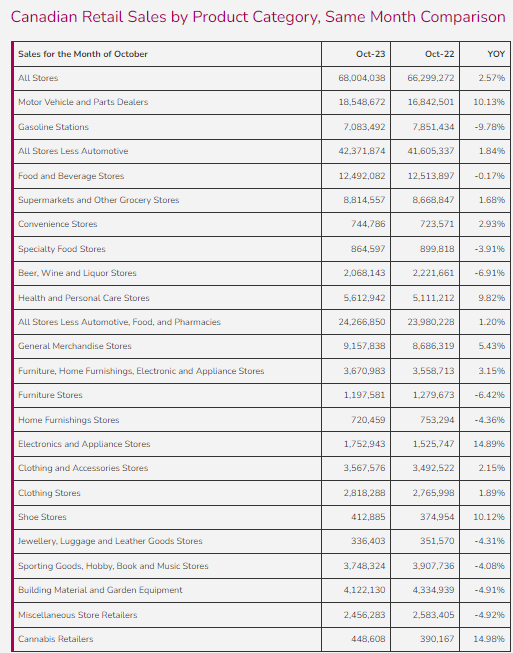

Canadian retail sales grew 2.6% YOY for All Sales in October, below the rate of inflation as well as the CPI rose 3.1% compared to 2022. Discretionary spend also remains low as All Stores Less Automotive, Food, and Pharmacies were up a mere 1.2% YOY.

Gas prices have been decreasing in Ontario, as reflected in Gasoline Stations with a decrease of -10.4% YTD. Contrary to this decrease, is the increase in Motor Vehicle and Parts Dealers are up 10.1% YOY and 7.1% YTD, likely a result of:

- 2022 realizing the worst sales in new vehicles in over a decade,

- The average price of a new car was up 22% in 2022 in Ontario, and is now up 20% in 2023 in Canada (the average new car in Canada will now cost you $67,817), and

- The increase in EVs has resulted in an increase of the average price of new cars as the prices for batteries are still high.

Continuing on a downward trajectory in October is Beer, Wine, and Liquor Stores with sales down -6.9% YOY. The trend of people moving away from alcohol continues to gain traction, and the appeal of cannabis alongside it. As such, Cannabis Stores are up 15.0% YOY. This category will likely continue to grow through 2024 as Mississauga begins to role out cannabis stores, and as regulations changed to allow cannabis retailers to operate up to 150 stores (up from 75).

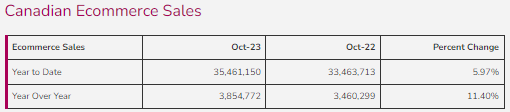

Ecommerce Sales grew 11.4% in October as Amazon’s final Prime Day of 2023 performed better than previous years. Customers began their holiday shopping even earlier this year with these sales spreading out their holiday budget, though it is likely to have a minimal impact on Black Friday/Cyber Monday performance. Though early predictions from StatCan are that November sales remain largely unchanged, Shopify reported a growth of 22% over Black Friday in 2023 compared to 2022.

Some predictions JCWG has going into 2024 are:

- In 2023, the Canadian market lost Nordstrom. Though StatCan does not report directly on Department Store sales, the category is down in the US. The Canadian department store industry, even without Nordstrom, is still over saturated. JCWG expects this category to have a reduction in the number of stores.

- Physical retail will continue to perform well, and vacancy rates will continue to decrease. This will be reliant upon relevant/exciting activations in the spaces.

- With the increase in physical retail, JCWG expects there to be more shopping centre operators announcing redevelopments to orient their centres further towards mixed use, especially in secondary markets.

- Travel will continue to increase, though travel related products will not grow to the same extent. However, categories popular amongst wealthy tourists (luxury, etc.) will likely benefit from this increase tourism.

- As the population ages, we expect the results of “downsizing” will continue to grow the secondary retail market (consignment, thrift stores, etc.). JCWG also expects more brands to control their own resale markets as brands such as Patagonia, Arc’teryx, etc. have already done.

For more insights into the retail industry and to help your brand prepare for these changes, reach out to the trusted experience at JCWG!

Thank you J.C. Williams Group for this report.