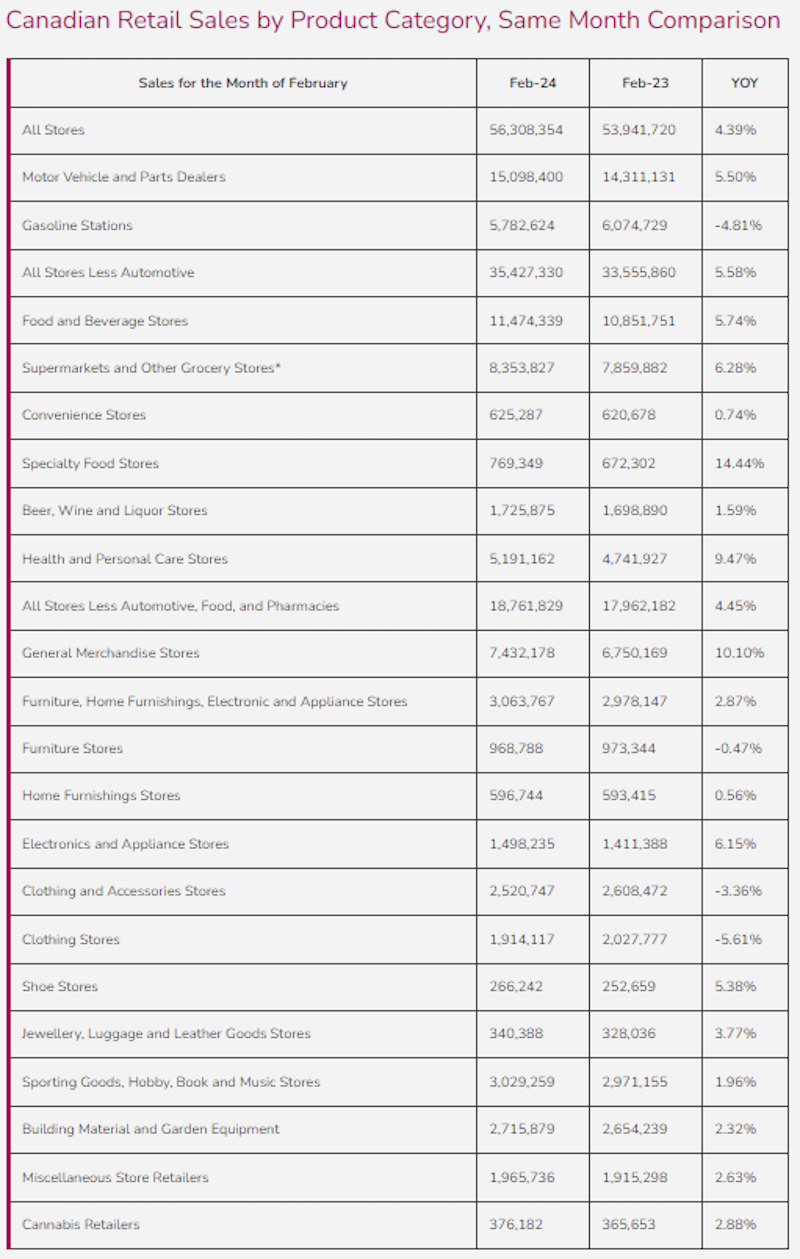

February retail sales continued on a path of growth in Canada with All Stores growing 4.4% YOY. Discretionary spend grew to a similar extent with All Stores Less Automotive, Food, and Pharmacies up 4.5% YOY in February.

2024’s Valentine’s Day, as with previous years, has an impact on February’s retail sales. However, with continuous inflation in 2024, it was likely that sales would be impacted. RCC performed a study for 2024 Valentine’s Day, with some notable results for those taking part in the occasion:

- 49.1% planned to spend $50 or less, with the rest expecting to spend more than $51.

- 25% expected to go to a restaurant and 22% expected to purchase/receive gifts.

- 58% expected to purchase products related to food/beverages/alcohol.

- 27% found inspiration in-store for Valentine’s Day, the highest compared to other channels.

- 78% plan to purchase products in-store rather than online/other for the occasion.

These predictions from the report were reflected in various categories in February’s retail sales, namely:

- Specialty Food Stores continued to grow in February 2024, up 14.4% YOY, as with in January (6.6% YOY). As mentioned last month, this is likely due in part to the frustration with larger grocery chains. However, this impressive growth in February can also be attributed to consumers looking to spend on food/beverage (58%). Rather than looking at restaurants, consumers may have opted to spend on higher-end food and cook rather than pay increasing restaurant prices.

- Beer, Wine, and Liquor Stores were up 1.6% YOY in February. This category has been on a slow, but steady, decline recently. While still down -0.2% YTD, this increase in sales is likely thanks to Valentine’s Day. Wine, cocktails, etc. are popular beverages for the occasion, and it seems consumers were not ready to part with this tradition. In contrast, Cannabis Stores sales were up a mere 2.9% YOY in February, much lower than is normal.

- Jewellery, Luggage, and Leather Goods Stores grew 3.8% YOY in February. This category is very popular for Valentine’s Day, but it seems to not be as strong as consumers’ budgets get tighter and tighter. Growth is growth, so consumers clearly were still spending on this category, and more than in 2023, but it may be that Valentine’s Day is slowly becoming more experience than product-focused.

For the first time lately, Home Furnishings Stores grew by 0.6% YOY. A category that has been struggling due to its inherently higher ticket items, as well as difficulties in the housing market, this is a welcome change. The Bank of Canada continues to hold interest rates, while there are no immediate signs of housing prices decreasing in the short term. Therefore, consumers may now be opting to simply buy a home if they have been waiting, or stay put/furnish/upgrade if they have purchased and expect the value to be in flux. Regardless, the Furniture Stores category is still down for February, -0.5% YOY, but this category may start to grow again for the same reasons.

As April is coming to an end (at the time of writing), the JCWG team is looking forward to summer retail trends.

- With consumers getting more and more used to increasing costs, will they budget larger ticket items throughout the summer or will they continue to save for the uncertain future?

- Where will the majority of tourists to Canada be coming from this year? Will Americans start to return more with favourable exchange rates?

- What products will be the most popular in summer 2024? Will summer wardrobe changes lead to increases in clothing sales (down -5.6% YOY in February 2024)?

- How are YOU preparing for tourists in summer 2024?

For support with building a seasonable and actionable retail strategy, reach out to the trusted experience at JCWG

{kind=link}