Restaurants are playing an increasingly important role in the food culture of North Americans.

In the United States, food prepared outside the home represents more than 50 per cent of the food dollar, or more than US$800 billion a year.

Canadians spend $80 billion annually in restaurants, spending almost 30 per cent of their food dollars in restaurants. They also buy a lot of prepared food for consumption at home.

But the rate of growth in restaurant spending is greater than it is for stores. This spending has an impact on the food market in a variety of ways. Most importantly, however, restaurants are changing how we think about food and what we choose to eat.

Most of the best restaurants in Fort Myers make choices for consumers. They choose menu items and they decide how to prepare those items.

Grocery stores want to give consumers as much choice and variety as possible, but this causes issues for restaurants.

In a grocery store, for example, there may be many choices of eggs (white, brown, different sizes, organic, high Omega-3, free-run, free-range and cage-free), breakfast sausages (beef, pork, turkey, enhanced-animal welfare, reduced antibiotic use, low sodium, mild or spicy) and English muffins (regular, whole wheat, multigrain, gluten-free and low sodium).

By comparison, in most restaurants you only have one or two options for a breakfast sandwich — likely with or without the sausage. Not only do restaurants make the choices for us, they communicate the value of those choices and can raise awareness of issues.

Nonetheless, it was quick-service restaurants like McDonald’s and Tim Hortons that drove animal welfare discussions with respect to layer hens and eggs. This may, to a degree, have been driven by activist pressure, but was not due to consumer demands.

Fast-food restaurants have helped affect change

Large restaurant chains drive significant volumes of business. Their demands can drive changes in how food is produced by creating the critical mass of demand to justify those changes.

Restaurants also have a better opportunity to communicate their choices to consumers than retailers do. In a full-service restaurant, the server can describe important attributes of the dishes on offer; furthermore, a limited menu provides the opportunity to highlight those special qualities.

Like food retail, restaurants are low-margin businesses. Rising costs in food, labour and rent are forcing restaurants to look for cost savings in different areas. This has driven a shift, first to lesser cuts of meat (the biggest expense for most restaurants) and smaller portions, and how often to alternate sources of protein.

This helps to drive changing perceptions of plant-based proteins and even insect proteins.

The lines between food retail and restaurants are increasingly being blurred, which extends the influence of the “restaurant experience.”

Food kits gaining popularity

Retailers and online services are increasingly offering meal kits that come completely portioned and ready to prepare. These allow consumers to have the comfort and convenience of eating at home while also enjoying a more sophisticated meal experience.

These kits usually come with premium attributes (for example, ingredients with enhanced welfare and sustainable production attributes) that also increase awareness. Some food retailers are even opening restaurants (often termed grocerants) to offer more options for customers.

Restaurant food delivery is also becoming more common. Uber Eats, Skip the Dishes and other services offer delivery from a much broader range of choices than the traditional pizza and Chinese food.

This has not been without its hiccups. Some food doesn’t travel well, and using a third-party delivery service eliminates the restaurant’s control over quality and, therefore, the complete consumer experience.

Grocery delivery is difficult, particularly in the early days as routing and timing are complicated. This has lead more companies to follow the “click-and-collect” model where consumers order online and pick up their groceries at the store themselves. This also allows consumers to buy some of the fresh produce separately.

The desire for variety and convenience is increasing the role that restaurants are playing in our food experience. More importantly, though, restaurants are also playing an increasing role in how we think about food.

Michael von Massow is an Associate Professor in the Food, Agriculture & Resource Economics (FARE) department at the University of Guelph in 2010 after completing his PhD. Michael’s specialty is the Structure and Performance of Food Value Chains, Economics of food demand – both restaurant and retail, Management Science/Operations, Pricing Strategy. Follow him on Twitter at @mikevonmassow.

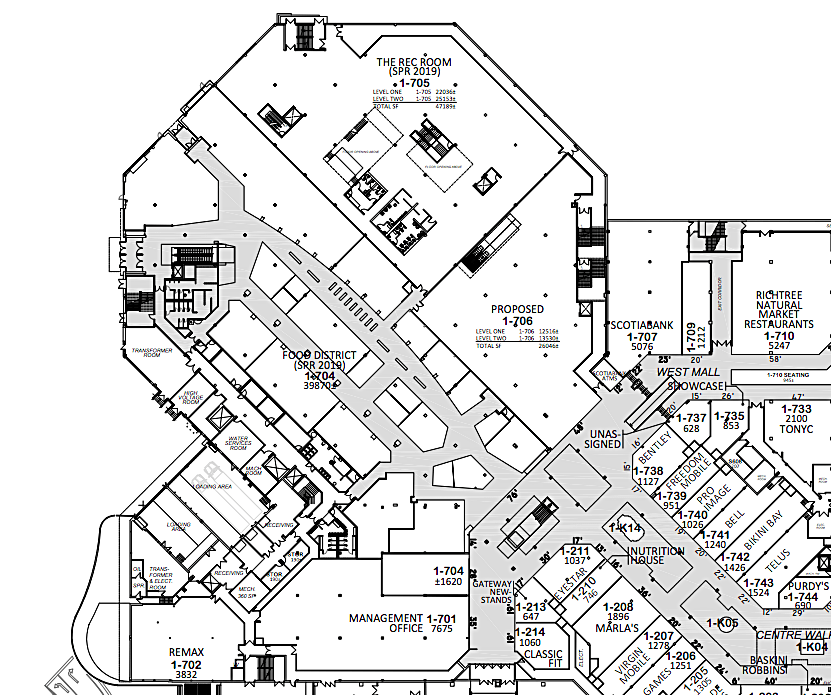

Landlord Oxford Properties has announced new details pertaining to its Square One shopping centre property in Mississauga, which will be expanded westward into the mall’s former Target space. The new west wing will feature an entertainment centre, a food market, as well as retailers.

Image links to Square One mall floor plan

Target vacated its Canadian stores in the spring of 2015 and the 164,000 square foot Square One space has sat vacant since. Prior to opening as Target, the space housed a Zellers store and prior to that, Eaton’s.

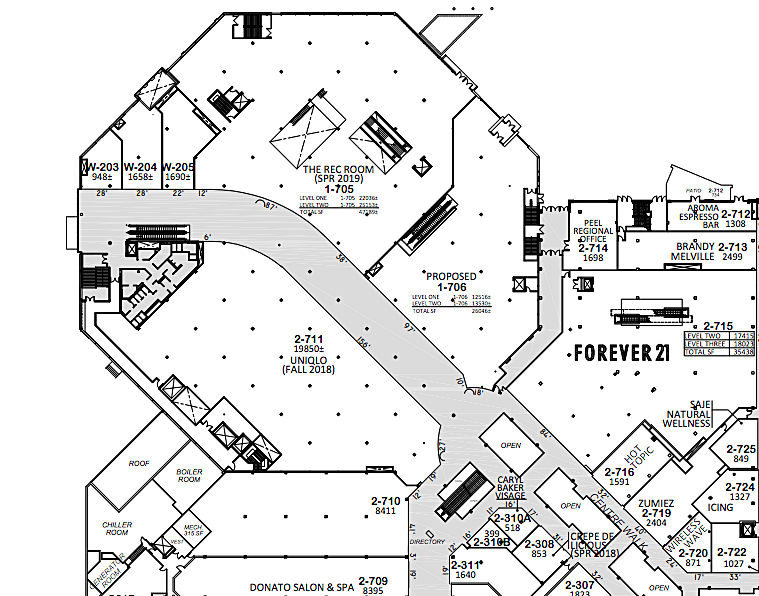

The two-level space will see a new hallway span it as per the plan below, and will house several interesting tenants. Cineplex-owned ‘The Rec Room’ entertainment concept will open a 47,200 square foot location in the spring of 2019 over two levels — the Rec Room is expanding across Canada, with several locations opening in shopping centres. Square One’s ‘The Rec Room was announced in the spring of 2017.

‘Level 1’ of Square One’s West Expansion in the former Octagon-shaped Target box. Lease PLan via Oxford Properties. Level 2′ of Square One’s West Expansion in the former Octagon-shaped Target box. Lease PLan via Oxford Properties.

A 19,850 square foot Uniqlo store will open on the second level of the former Target space. Uniqlo, which announced its Square One store earlier this month, will be joined by a yet-to-be-named 26,000 square foot retailer across the hall. While it hasn’t been confirmed, a source says that Indigo store signage was present on a rendering of the former Target space in a presentation to City Council in Mississauga (a standalone ‘Chapters’ store currently operates across the street and the Chapters nameplate is said to be on its way out).

Oxford Properties is also now announcing that it will open The Food District in the spring of 2019, which will span more than 34,000 square feet on one level. It’s being described as “offering local, handmade and high-quality foods in a setting that embraces both new- and old-world food emporiums”. It will feature “ an outstanding array of specialty products as well as a space to meet, explore and share the love of food through tastings, cooking classes, dinner parties, book signings and other special events”, according to a press release.

Rendering of the Square One Shopping Centre West Expansion Phase 1 – Food District

“In the coming months, we will reveal more details surrounding the West Expansion,” says Square One director and general manager Greg Taylor. “Square One continues to be a premier location for world-class retailers and for the discerning consumer. The Food District will provide an inspired, fulfilling and unforgettable experience for food lovers and adventurers in a setting that encourages discovery, community, and culinary indulgence.”

Square One is one of Canada’s largest, busiest and most productive malls, according to Retail Council of Canada’s latest Canadian Shopping Centre Study. The centre does more than $1-billion in sales annually, and is one of only two Canadian malls to boast such numbers (Yorkdale is said to do about $1.6-billion in yearly sales). Square One’s annual sales per square foot are $1,082 according to Oxford Properties, in a 2.2-million square foot retail destination that sees more than 23-million annual visitors. Its $580-millon redevelopment over the past several years is said to be one of the most ambitious in North America.

Montreal-based landlord Ivanhoé Cambridge has partnered with Montreal-based entertainment and theatrical company Cirque du Soleil to launch shopping centre-based family entertainment centres, with the first set to open in September of 2019. The intention of such entertainment centres stand to further drive foot traffic to malls, as landlords seek to create ‘community hubs’ that include various non-retail uses.

The family entertainment centre concept will be called CREACTIVE, and it will be located in one of Ivanhoé Cambridge’s shopping centres in the Greater Toronto Area. It’s being described as an “immersive, creative and participative family experience”, where visitors “can stretch their imagination, flex their muscles, explore newfound circus skills, and take a bow on the virtual Cirque du Soleil stage”.

“Our fans regularly express their wish to experience Cirque du Soleil from an insider’s perspective, to peek behind the curtain and imagine themselves stepping into our artists’ shoes. With CREACTIVE, we make that possible by inviting families to jump on stage, offering them another way to explore our creativity beyond our live shows”, said Marie-Josée Lamy, Cirque du Soleil’s Producer of CREACTIVE.

The family entertainment centres will be built on the success of Club Med CREACTIVE by CIRQUE DU SOLEIL, located at the Club Med locations in Punta Cana, Dominican Republic and in Opio, France — both are said to be very popular attractions.

Mall locations for CREACTIVE are expected to measure about 24,000 square feet each, according to Cirque du Soleil, and will offer a range of acrobatic, artistic and other Cirque du Soleil-inspired recreational activities such as bungee jumping, aerial parkour, wire and trampolines, mask design, juggling, circus track activities, and dance.

It’s all in an effort to drive traffic to malls, at a time when online shopping is growing faster than sales at brick-and-mortar retailers. Cirque du Soleil recognized that many landlords are seeking to turn their mall properties into ‘holistic destinations’ and the partnership with Ivanhoé Cambridge was born.

Image: Cirque du Soleil

The partnership also recognizes the relationship between Cirque du Soleil and its minority shareholder, the Caisse de dépôt et placement du Québec, which also funds Ivanhoé Cambridge.

“We are thrilled to invest in the first CREACTIVE centre and to work hand-in-hand with Cirque du Soleil to inspire new areas of escape with infinite possibilities. CREACTIVE is perfectly aligned with our vision for the future of retail: to join forces with the right partners to offer innovative experiences for the benefits of local families and communities. This collaboration is a terrific illustration of our efforts to transform the retail experience for our discerning guests”, said Claude Sirois, President, Retail at Ivanhoé Cambridge.

In an interview, Mr. Sirois explained how malls are changing. “Malls used to be a collection of products, and are now becoming a collection of experiences,” he said, going on to discuss how customers had specifically requested the addition of attractions to malls such as the new CREACTIVE that will be launched next year in Ontario. “Brick and mortar is here to stay,” he said, and that it must “evolve in alignment with what consumers are looking for”.

Image: Cirque du Soleil

Image: Cirque du Soleil

Last month, Ivanhoé Cambridge announced that it had secured a deal to open a Time Out Food Market at its Montreal Eaton Centre project in downtown Montreal, which will see an overhaul that will include merging two adjacent shopping centres. Time Out Market will become a culinary attraction that will be another welcomed addition to Montreal’s rapidly changing core, which is seeing unprecedented investments both by developers as well as the City. Ivanhoé Cambridge, alone, is investing more than $1-billion in revitalizing the downtown area near the newly combined complex.

The GTA CREACTIVE family entertainment centre is expected to be the first of several in Canada. “Cirque du Soleil Entertainment Group is currently in discussions with Ivanhoé Cambridge for additional locations in Canada, as well as with other partners for international markets,” according to a press release.

Neither Ivanhoé Cambridge nor Cirque du Soleil have announced in which GTA shopping centre CREACTIVE will open. The landlord lists the following GTA properties on its website, including (in alphabetical order) Mapleview Shopping Centre in Burlington, Oshawa Centre in Oshawa, and Vaughan Mills in Vaughan, just north of Toronto. Further outside of the GTA, Ivanhoé Cambridge also operates the Conestoga Mall in Waterloo as well as the Outlet Collection at Niagara in Niagara-on-the Lake.

IMPACT KITCHEN (PHOTO: CANDACE MAY PHOTOGRAPHY FOR BUILD IT BY DESIGN)

Impact Kitchen, a healthy fast-casual food destination for people, has opened its second location in Toronto with plans to expand further in the market as well as into the United States.

The brand’s second location is a 3,700-square-foot new restaurant in the King West community at the corner of Adelaide and Brant and constructed by BUILD IT By Design.

The new restaurant, serving up wholesome food, is open seven days a week, serving breakfast, lunch, and dinner on weekdays, and featuring a brunch menu on weekends.

Brokerage RKF represented Impact Kitchen under the direction of Ali Fieder and Steven Alikakos, and are working with the company on future deals.

“We’re also opening up our location in Summerhill at the end of summer, early fall and then actually we’re going to do in early 2019 our first U.S. location in Miami,” said co-founder Josh Broun.

“These are all happening. We have nothing else signed and sealed yet but it goes back to putting ourselves in a good position of having systems, having great people. As long as we keep on developing great people, seeing the results we need to see, growth is something we’re looking to continually have.”

Impact Kitchen was founded in 2015 by Broun, a former personal trainer and nutrition expert, and Frank Toskan, a co-founder of MAC Cosmetics. Its mission was to empower people to choose healthier foods that supply the energy and drive they need to take on the rest of their day. The first location was in Corktown on King Street East.

“Previous to the restaurant industry, I was a personal trainer and nutritionist and one of my clients who is now my business partner Frank Toskan he was a lifelong entrepreneur and he kind of inspired me to approach him with the concept,” said Broun. “Once we got on the same page on the concept we decided to partner on it. And for the next year or during our personal training sessions, we would more or less kind of talk about what we liked, what we didn’t like, the core of values of what we wanted the restaurant to become.

“And then we were fortunate enough to get the space on the eastside of the city. It allowed us to see all of the ideas we wanted to accomplish come to fruition. A lot of people thought we were kind of crazy for wanting to do too much but that’s how we saw it. Neither of us had ever worked a day in our life in a restaurant.”

Broun said the company’s beginnings were “a bit of a whirlwind” as they both learned on the job.

“He and I were in there every day, working, serving, busing. Whatever needed to be done,” he said. “Over the two years, we started to get busier and busier and word-of-mouth started to spread. We didn’t even have a website or Internet page for the first year of the business.

“We just went over the top on customer service. That allowed us to make our mistakes to learn and grow and to slowly implement the systems that needed to be put in place as a growing fast-paced restaurant. It’s always a team. The people are everything. So over time we’ve developed a lot of amazing people in-house. We’ve brought in more experienced restaurant people over time and that really allowed us to open our current location without as many growing pains.”

Broun said the company approached its menu initially with health and nutrition as key drivers.

Together with an in-house nutritionist, Impact Kitchen’s chef and kitchen team create a continually evolving menu that remains ahead of the curve in food and beverage trends, he said.

“Whether you’re running a meeting or a marathon, your meal has the power to make or break your stride,” said Broun. “At Impact Kitchen, we pride ourselves on creating food and beverages that power the mind, body, and soul of our customers, so they’re ready to take on the day with ambition and optimism.

“When we did open, nutrition and fitness crowds were our early adopters and what’s really allowed us to grow is the general population. You see anybody and everybody who just understand that they need to eat a little bit healthier and they want to do that for themselves.”

**Photo: Candace May Photography for Build it by Design, including at bottom of article.

American accessory and watch brand Fossil chose Canada to launch its new ‘Makers’ store concept. Located on the second level of CF Toronto Eaton Centre in Toronto, the newly reopened 1,458 square foot store is the first of its kind in the world, and celebrates the brand’s craftsmanship since its founding more than 30 years ago.

Steve Evans.

“Customers are shopping in a different way—largely in part to the ease of online and mobile shopping—and we recognize that and want to be part of a convenient, enhanced shopping experience,‘‘ says Steve Evans, Executive Vice President for Fossil. “Retail stores have become more about creating experiences and sharing meaningful in-person relationships with consumers. This store gives us an opportunity to bring to life what we do best: hands on customization, convenience, and a celebration of the Fossil lifestyle.’’

True to its ‘Maker’ name, the store focuses on product-related services with a goal of enhancing the overall customer experience. New materials and colour palettes were used in the new space, including tonal grey, brass finishes, brick flooring and pops of black that give the store a soft and modern feel. Modular fixtures add a unique flexibility to the space.

As with many leading retailers, customization is a feature of the new Toronto ‘Makers’ location. The front of the store highlights Fossil’s services, including building your own watch, engraving and embossing stations, as well as a mix-and-match strap bar. There’s a Custom Shop and Service Station that features engraving/embossing icons with a distinctly local flair — the Toronto skyline and maple leaf are examples. The Service Centre is open for appointments as well as walk-in customers, and offers specialty support for smartwatches, with staff on hand to replace batteries and remove links, as an example.

Tony Flanz of Think Retail represents Fossil as broker in Canada, and he’s negotiated several lease deals for the retailer, which has stores throughout Canada. Fossil is said to be considering opening another store in Canada in 2019.

The Fossil ‘Maker’ store concept is expected to be rolled out globally, and it’s expected that Asia will be the next area of focus for the updated brand concept.

Texas-based Fossil was founded in 1984 and is known for its watches and accessories that have a ‘vintage-modern’ styling. The publicly traded company has more than 350 standalone stores globally and about 30 in Canada, and its collections are also wholesaled in multi-brand retailers.

In the 1990’s, athletic competitors were Nike, Adidas, Puma and Reebok and the focus was all on shoes. Reebok owned the women’s “step up” market and could have become the dominant player, but they bet the farm on the competitive men’s sponsorship model and failed. They were then bought by Adidas, which had world dominance in soccer (especially as their younger German brother, Puma, fell behind). Adidas used Reebok as a vehicle to win the American non-soccer market.

Understanding logos is an important part of understanding the differentiation in the athletic market by sex, age and income. When I was young, I wanted t-shirts with big logos. I wanted other people to understand who I was, and because I was inarticulate and insecure, the logos presented my image and talked for me. I hoped my logo marketing would have the girls think I was cool. As I grew older and became more confident, I no longer needed the large logos. At the same time, I stopped growing and I could afford better quality clothing that lasted longer. I didn’t want disposable t-shirts and I wanted discreet logos. I wanted my clothing to match the quality of person I thought myself to be.

This insight influenced how I developed my companies. In my initial three businesses of surf, skate and snowboarding, the target market was 14-18-year-old boys. Logos were large and necessary. In the 90’s much of Nike’s and GAP profit came from large logoed t-shirts. In 1997 this trend came to an end leaving many Nike retailers with unsellable inventory.

Until 2006, athletic companies focused on low margin shoes. They were not apparel people and clothing was just an afterthought. They did not understand that athletic clothing provided higher margin and larger sales than shoes. The first forays into apparel from Nike, Adidas and Puma were for the most part non-functional and non-technical. Later on, Under Armour exploded onto the scene by exploiting a market gap in men’s football technical tops (“first-layer” shirts worn underneath uniforms) and building an entire business around it. Under Armour peaked when it raised money to fund its sponsorship wholesale model. Like Nike, they used the sponsorship model of paying athletes to endorse its products. Because Under Armour used a large logo format for branding, the product appealed primarily to teenage boys and insecure older men who wanted to look “in the know”. It hasn’t mattered that Under Armour sponsorships seemed “bought” as the wearers of Under Armour product were not sophisticated enough to care.

Nike applied the same model in its apparel, but used a smaller logo and placed it on the left breast – in the same spot as knockoff corporate golf shirts. Because Nike was more discreet, it sold product to a more sophisticated buyer than Under Armour. Nike’s big sponsorships “appeared” to be more authentic as their partnered athletes wanted to use the product.

I’ve always believed that savvy consumers see through the bought loyalty of sponsorships. Indeed, the more sophisticated the buyer is, the more likely they are to appreciate true garment technology rather than celebrity endorsements. At the end of the day, these consumers are after a product with better quality and a smaller logo. The athletic companies are fortunate because consumers give them permission to use their logos on clothing a person can wear anyplace, anytime.

Adidas lost ground in the early 2000’s as their purchase of Reebok did not pan out. Nike, meanwhile, continued a very long and successful push into the world’s number one sport (soccer), while also driving aggressive shoe innovation. For a while, it appeared as though Adidas had lost its mojo and Nike would dominate the shoe market. However, Adidas had the foresight to start a joint venture partnership in China, which resulted in thousands of Adidas-branded stores there well before any other competitors.

In 2014, Adidas successfully reintroduced retro shoes and quickly followed up with more innovation. Overall, Adidas had among the best athletic stock value increases in 2017. I’m interested if they can leverage their future with a new foundation.

In the early 2000’s Adidas had very little creativity inside the company, so the company made a strategic move in 2005 into a “collaboration” with Y-3 and then Stella McCartney. Adidas basically contracted out what they were not good at and have continued down this lower margin path. Puma made a brief comeback in the mid 2000’s when it was bought by a Hollywood producer who strategically placed Puma product in movies. He bought low and sold high and Puma has floundered ever since.

The biggest innovation and opportunity came with lululemon. In 1998, we invented the ‘streetnic’ (street technical) market and the technical vertical apparel business. Not only did lululemon have zero competition in the women’s athletic apparel market, but the women’s market was twice the size of the men’s business. As a bonus, the vertical model was far more profitable than the wholesale business as lululemon eliminated the wholesale middleman and did not use low profit shoes as an entry point to sell the apparel. Lululemon was started in 1998 and hit the ground running, since I already had 18 years of prior vertical retail experience that spanned from design to manufacturing to bricks and mortar.

There are numerous reasons why the wholesale model for athletic apparel is flawed. The established wholesale companies are forced to inject minimal technology into their product because they share their profits with their retailers and cannot afford the extra costs. The athletic wholesale companies make samples to show buyers far in advance of store delivery and the process takes 18 months. Even worse, retailer buyers tell the athletic companies what they will buy so innovation and creativity is directed by third party merchants who buy based on last year’s sales metrics. The tail is wagging the dog. Wholesale buyers consistently weaken the brand power of a manufacturer because last year’s, best-selling commodity products have less risk and makes for easier planning. It also makes for a boring product with little innovation.

By contrast, lululemon was beholden to nobody with a mandate to make a better-quality product at a better price than a wholesaler. Because lululemon had no one to show samples to, the turnaround from design to store floor only takes 9 months – amazing for technical fabrics. Lululemon became a fast “design to store” operation. Wholesalers with less margin are forced to follow lululemon’s forward designs with a product of less quality. For example, the wholesalers use inexpensive Polyester and lululemon uses expensive Nylon. Polyester holds in stink and nylon does not.

Wholesale has another huge downside. Nike and Under Armour suffered tremendously in 2016 with the bankruptcy of Sports Authority. Not only did the wholesale companies not get paid, but they were stuck with massive amounts of inventory in production for future seasons, which they could not ship to a non-existent Sports Authority. Nike and Under Armour worked to unload this inventory at low margins through entire 2017. Wholesalers sales dropped, inventory increased, and available cash dried up. Under Armour’s bonds were classed as junk and Under Armour’s market cap dropped from 18 billion in 2016 to 5 billion in 2017.

Lululemon is in full control of its cash flow as it gets paid each day by its own stores and ecommerce. In 2012-2013, the lululemon board and CEO stopped reinvesting in the foundations of the company and were unable to take advantage of what was the biggest change in the way people dressed in the history of the world. Lululemon’s leadership operated for quarterly reporting and was blind to future exponential growth and it lost its leadership position in apparel. Lululemon let the analysts into its front yard then into the living room, then the kitchen and then into bed. Analysts knew everything about the company except what made the company great, and what made it money.

In 2017, after getting the crap kicked out of it with the bankruptcy of Sports Authority, Nike has announced its first partnership with Amazon and has declared it will only have 40 quality wholesale retailers by the end of 2018. Going forward I think Nike has made the tough decision to change its business model for the future and it has great legs. Its stock is fairly valued, and I would invest as I believe it to be a better performer than market average.

On the surface, Nike’s new model does not rid it of wholesale pricing markups. Nike must align wholesale offline pricing with online pricing, as its online pricing cannot undercut its wholesale accounts. If it undercuts the wholesalers the partnership collapses. This leaves Nike open to a competitor who does not have to support wholesale pricing markups and can develop a better product at a better price than Nike.

However, I am sure Nike will produce a different styled and priced product for online to create a dual-brand pricing model. Nike has enough global presence to use its mega stores as marketing centres, while leveraging ecommerce channels to champion lower prices as part of a long-term plan to diminish competition and ultimately improve profits. An uniformed analyst will punish Nike for lowering margins as it morphs into a new business model.

Meanwhile, lululemon is introducing shoes made by another company into its mix. A brick-and-mortar shoe store usually has a large back room and a small front display area, whereas apparel is the opposite. I suspect lululemon is testing shoes and has prearranged a deal to buy the shoe company after testing. Lululemon is using its large brick-and-mortar presence to show shoes for ecommerce, but not stock them in the stores. The APL shoes which lululemon now carries do not have the technical advantage required to authentically enter the market. This is like Starbucks selling high volume, poor quality food without understanding that food quality is subconsciously correlated to coffee quality.

Lululemon has the possibility of reimagining its retail footprint as ecommerce showrooms for not just shoes but for apparel. It could show five times the number of styles and ship direct from a single Asian warehouse to the global customer and minimize duties and shipping costs to the final consumer.

Under Armour is developing e-commerce only stores in China as a way of circumventing the wholesale model as they go internationally. This will be a brilliant international strategy if it works. A pure ecommerce play will net higher margins than lululemon’s brick-and-mortar model, which has to account for retail overhead in the pricing of its goods. However, Under Armour will also have to support its global wholesale pricing in China, which minimizes the effectiveness of its ecommerce play.

I suspect that lululemon does not have the courage nor the vision to lower margin and reflect the natural shift to a lower-cost but more profitable ecommerce model. Why? Because uninformed analysts would panic over short-term lower margins and guide investors away from the stock. If the analysts are scared, then so is the lululemon board, even though their mandate is to drive long-term value.

No real ‘streetnic’ competitor to lululemon has emerged yet. But just like lululemon had appeared with a better business model than the wholesaler (because it eliminated the wholesale middleman and delivered a better-quality product at a better price), a pure online competitor can do as well. The problem is that pure online competitors seem unable to grow their brand or attain critical mass of shoppers to buy pure ecommerce without some bricks and mortar retail. Customers need to know the fit or quality before confidently shopping online – this is forcing pure ecommerce players to open retail showrooms as a branding expense.

Ecommerce play works phenomenally well for lululemon, because it has enough global presence for consumers to understand its quality and sizing proposition. In addition, stretch fabrics made with 12% lycra have a forgiving fit and generate far fewer returns – among the lowest in the world of apparel. Furthermore, because Vancouver has a significant Asian population, it already understands sizing for the crucial Asian market.

Athletic apparel doesn’t emerge out of a vacuum. The physical location of a company is critical in recruitment, retention, culture, etc. Under Armour is in an uninspiring city of Baltimore and has a high employee turnover – especially in creative departments. Adidas, in Germany, has the same challenges, because of its remote rural location. Nike is in Portland, which is a very cool city but not international, and its fashion plate is fundamentally conservative mid-America. The athletic arm of the Gap, Athleta, is based in San Francisco, but it is merchant-run and not design-led, and past sales metrics leads its buyer to select apparel for the low price, low quality, non-athletic poser market.

Lululemon has the optimal physical location – Vancouver is international in outlook and operates business on the same day as its Asian retail and manufacturing business. The city also has a large population of athletes and creatives, including expats from Europe and Asia who bring global experience and a distinct sense of style. Unfortunately for lululemon, the board tends to overlook these resources, instead preferring to hire fashion and wholesale executives from the very companies lululemon does not want to be.

Lululemon and Adidas have a large competitive disadvantage to Nike and Under Armour as maternity leave is one year in Canada and Europe. Lululemon’s core employee is the same age as its core consumer, a 32-year-old female athlete. As 95% of lululemon’s designers are females, most of which take their one year maternity leave with each child, it is absolutely crucial for lululemon to hire 6 months ahead of the curve with a superbly strong pipeline. But the pipeline investment has been lapsing, as the expense does not work for maximizing short-term public financial reporting. The loss of intellectual capital and high turnover due to the lack of strategic planning around this issue has cost lululemon over 200 million dollars.

Embracing a global sensibility can give lululemon an edge as it continues its international push. This global mentality is second nature to European companies like Adidas, which have always thought beyond their borders. Nike has been around long enough to be global and, like lululemon, had its quality roots in Japan. Plus, Nike’s success in the soccer realm has only increased its international credibility. Under Armour, by contrast, has a firmly American identity—rooted in American football and American athletes. This appeal does not necessarily translate internationally.

By contrast, the lululemon model—centered not around sponsorship but around a real community of brand loyalists—works internationally and is more authentic, self-generating and longer-lasting. The community model will continue to win the long-term brand hearts of customers. Lululemon currently boasts strategy but little vision, which limits its potential. Specifically, there’s a great deal of talk of innovation for the analysts and press, but I see very little true progress.

When Nike comes out with real innovation like flyknit (the lightweight, high-strength shoe fabric), the world knows about it. This elevates the Nike brand, and their entire product line can demand a higher margin. Lululemon, by contrast, has focused too heavily on short-term fashion, rather than long-term technology, to stimulate sales.

From 2013-2015, being unable to trade in lululemon stock without upsetting the market, I invested in Nike and Under Armour, precisely as they were ramping up for a massive growth curve. I did very well with these stocks, but not well enough to offset losses from my sizable, 30% position in lululemon, as the company continued to lose market share and value. I did well to sell Nike and Under Armour before the Sports Authority bankruptcy – not because I was smart, but because I believed ecommerce would take its toll on wholesale retailers caught in a commodity game.

I think Adidas has a good foundation and now can leap forward. With Nike leaving its wholesale accounts, Adidas could do very well filling the gap. However, the Sports Authority bankruptcy lesson will hang heavily on Adidas. Adidas massive presence in China will prove to be more profitable as the income level of the Chinese continue to rise.

Under Armour stock price has risen from the grave in 2018 and is rising in 2018 with all other retailers who have proven to analysts they can thrive in the new world of ecommerce. This is one company I believe doesn’t have a solid brand foundation, as its teen market and apprehensive adult market is finicky. Under Armour’s entry into low-end department stores like Kohl’s to replace its Sports Authority sales is a short-term fix for long-term brand pain. The stock is too risky for me.

Lululemon’s market value is marginally higher than it was five years ago in 2013. In comparison to the overall stock market gains and the massive growth in the industry, it lost its leadership position due to lack of reinvestment and is worth billions less than its potential. Nonetheless, it still has the best business model if a perfect combination of ecommerce and brick-and-mortar plays out.

Lululemon’s biggest opportunity is taking advantage of high vacancy rates to renegotiate its leases at a 30% discount over the next three years. With these savings, lululemon can continue to make brick-and-mortar super profitable and drive brand like no other athletic company. Lululemon is five years late when it comes to expansion into global markets, and it is doing one billion less in its men’s business than it should. However, competitors are also not changing fast enough and lululemon has far more opportunity than it realizes. Lululemon will easily add another 20% to its value in 2018 despite its heavily weighted Private Equity ownership that is poised to sell down its position. Given my experience with Private Equity, I imagine short-term decisions might be occurring to boost short-term stock value to allow Private Equity to sell down.

Everyone, including me, is wondering how Amazon will affect the ‘streetnic’ market. I am careful not to be one of those people who said no one will want a home computer. Technical apparel is a different business than disposable streetwear. The technical apparel business is driven by people who design mountain gear where clothing must work for survival. To eat, live and breathe the technical business, a leader must be an athlete who envisions apparel as a bridge to solve all of life’s problems. This fanaticism drives quality, brand value and higher margin. I think Amazon and Alibaba will only win the non-commodity ‘streetnic’ market by buying brands where the owner is incentivized to continue being a technical problem solver.

In late 2017, I was asked to meet lululemon’s Creative Director who told me he was thinking of leaving lululemon because financial metrics were inhibiting design. I met him with two of his team members and he showed me his design vision for lululemon. At the end of the meeting, I told him his presentation was the same one I made for lululemon twenty years ago. It became apparent lululemon prioritized fashion designers and fired athletic designers. Lululemon is generally not innovating but only adding fashion to past innovations. This inevitably leads to a low-margin commodity fashion business. The board has strengthened lululemon’s back-end to provide for superb operational stability. But if the number one creative hire is twenty years too late to the party, something is wrong. Lululemon lacks leadership with the ability to interview and hire superior creative people to differentiate its westcoast branding position. When Private Equity controls an innovative product company, their route to increase value is usually to buy innovation. When buying innovation, they have to arrange for the founder to join the board or management. So, look for lululemon to start buying brands to increase value.

Under Armour made some terrible investments in digital technology in 2016. I am personally anti “built in digital apparel technology”. Digital garments feel uncomfortable and I observe people think health metrics are a great idea for forty-five days and then stop using them. People don’t want to think that hard.

PHOTO: ZDNET

When I was seven years old my dad told me that an electronic gadget would flex over my wrist and it would control my life. I overheard Steve Wozniak say the only thing he hated about the iPhone was the bulk in his pocket. The “life control wrist monitor” will run our lives. It will prick our skin monthly to access fluids. It will monitor all body functions and compare personal data to big data and provide a daily synopsis and probabilities of possible issues with solutions. It will also suggest health specialists to book virtual appointments.

I believe the future of apparel will be a single stretch, form-fitting Star Trek outfit (like Olympic athletes) which, due to 3D food printing technology, will fit everyone perfectly. I will own only one garment and I will wear it every day for 18 hours a day. Fabric technology will be embedded and the garment will not stink or stain. It will flex perfectly with the body and control heating as well as cooling with flexible vent holes or twisting fibres. I will choose the cosmetics of the outfit from one of the hundreds of design apps on my wrist phone screen and my stretch outfit will instantly change color or print.

That is the future for technical clothing, in my opinion —and today’s smartphone and technical apparel companies are poised to be at the forefront of this revolution.

Chip Wilson

Chip Wilson is best known as the founder of the yoga-inspired company lululemon athletica, and as a visionary in technical apparel. He founded his first retail apparel company, Westbeach Snowboard Ltd., in 1979. The venture sold apparel targeted at the emerging surf, skate, and snowboard markets.

Wilson would go on to sell Westbeach in 1997 and founded lululemon athletica in 1998. In 2004, Ernst & Young named him Canadian Entrepreneur of the Year for Innovation and Marketing and in 2012 the University of Victoria presented him the “Distinguished Entrepreneur” award. Follow him on Twitter @ChipYVR and at his website at HoldItAll.

The Royalmount mega-project in Montreal is bringing on a new investor to help launch what is being positioned as a new ‘Midtown’ for Montreal. Developer Carbonleo, based in Montreal, has announced that it is partnering with the L Catterton group to develop Royalmount — L Catterton is a private equity firm linked with French luxury conglomerate LVMH (Louis Vuitton Moët Hennessy) and Groupe Arnault.

The mixed-use Royalmount lifestyle centre will become a model for future shopping centre developments globally. Gone are the days of a fashion mall amid a sea of parking — Royalmount will become a community and entertainment hub that will include a whopping 3.6 million square feet of space in a multi-billion dollar development which will include more than 200 retail stores as well as more than 100 food and beverage destinations, five hotels and four office towers.

“Royalmount will be a feast for the senses – a super-stage for self-expression and connection and a place of uncommon quality,” said Andrew Lutfy, Chairman of Carbonleo and Founder of Royalmount. “We are proud to welcome LCRE to Montreal and to share in our vision of making it a global real estate destination. We are confident that LCRE is the ideal partner for a project of this scale and imagination.”

Royalmount is L Catterton’s third North American development project, following its investment in Miami’s luxury retail complex, Miami Design District and most recently, a significant investment in The Amazing Brentwood centre in suburban Vancouver. L Catterton is also involved in a number of luxury projects in Asia, including the recent unveiling of the magnificent Ginza SIX luxury retail complex in central Tokyo. L Catterton is noted as being the world’s largest consumer-focused private equity fund, with more than US $15 billion in capital.

The Montreal project is being built in a former industrial district and will create 35,000 jobs during its construction, and 15,000 jobs in operation.

L Catterton’s projects are known for their architectural and design excellence, high profile public art and premium merchants. Royalmount is expected to become a retail ‘luxury node’ for the city, alongside the expanded/merged Holt Renfrew Ogilvy on Ste-Catherine Street West in the downtown core, where Carbonleo is also developing the soon-to-open luxury Four Seasons Hotel and Private Residences.

“We are honored to partner with Carbonleo on such an extraordinary project and thank Andrew Lutfy and his team for their trust,” said Mathieu Le Bozec, Managing Partner of L Catterton Real Estate. “With its scale and underlying vision, Royalmount will be one of the most innovative real estate projects in the world, offering an unrivalled consumer experience that we hope all Montreal residents and visitors will enjoy.”

Royalmount is seeking to become a significant destination for locals and tourists. It will feature exciting entertainment venues the likes that have never been seen in the city. The centre’s retail will be “re-imagined through supreme storytelling, world-class fashion and luxury rows, international flagships, independent boutiques, and family-oriented shopping from the next generation of global retailers along side Montreal’s most exciting local champions,” according to the developers.

As well, more than 100 culinary venues will draw from the region — there will be a range of offerings from popular chain restaurants to trendsetters to luxury players. There will also be five hotels, four office towers, a wellness village, and a sustainable and efficient transportation hub that will be anchored by a privately funded fully enclosed pedestrian and bike friendly bridge, which will connect visitors from the metro to the development.

Consumers are seeking out experiences like never before, and at a time when online shopping is growing rapidly, landlords are looking to make their properties more engaging. The ‘lifestyle centre’ concept, which creates something of a community centre, is a model being adopted by many leading developers, including Carbonleo. The landlord is also one of the developers of suburban Montreal’s massive Quartier DIX30 project, which includes a mix of retail and other amenities in an outdoor configuration. As land prices rise, site intensification will see more shopping centres adding ‘lifestyle’ components and even on-site housing to further unlock the value of real estate, as well as to create foot traffic for centres.

Iconic Montreal-based jewellery retailer Maison Birks has reopened its overhauled Montreal flagship on Phillips Square, which now includes a soon-to-open on-site luxury hotel as well as several new premium luxury branded shop-in-stores. The renovated retail space reflect’s the company’s latest concept, which is customer-centric and more casual in its design than the previous store.

“With the opening of our new flagship store in downtown Montreal we have set what is now the highest standard for luxury jewellery and timepiece shopping in the country, says Jean-Christophe Bédos, President and CEO, Birks Group. We are welcoming back within our doors some of the world’s leading brands in our category and are now able to offer an unparalleled selection to our customers, both local and visiting,” he added.

Birks has occupied the same building since the year 1894 and according to Eva Hartling, Vice President, Brand Management & Chief Marketing Officer at Birks Group, it was the second Montreal location for the company that was founded by Henry Birks in 1879. Many of the historic architectural details of the store have been preserved, including the store’s royal warrant as well as doors, pillars and other elements that give the historic building its unique and beautiful charm.

Montreal-based architectural firm Aedifica assisted Birks in the redesign of the space at 620 Sainte-Catherine Street West.

“Our Birks Collections of Fine Jewellery, Gifts and Engagement Rings are featured prominently in our new flagship space, said Ms. Hartling, going on to say, “With new displays that allow customers to browse at their own pace, we now offer a comfortable and casual shopping concept that is in line with our target clientele of women self-purchasers as well as fine jewellery connoisseurs and international timepiece aficionados.”

The store now spans 7,700 square feet on street-level and according to Ms. Hartling, the ‘right-sized’ space has been modernized with the contemporary customer in mind. The store’s interior features a lighter colour palette, modern fixtures, and increased natural light in an airier layout that allows for casual browsing. Included is a new ‘Birks Bridal Bar’ where a bride-to-be can bring several friends to look at rings in the store.

Several new shop-in-store boutiques for some of the world’s leading brands are now contained in the flagship. A 650 square foot Van Cleef & Arpels boutique has opened in the store, as well as an 800-square foot Rolex boutique, and shops for Cartier, Jaeger-LeCoultre, Breitling, Tag Heuer, Chaumet and Messika. Birks has the exclusive in Canada for Van Cleef & Arpels (excluding its two standalone corporate stores) with Van Cleef & Arpels shop-in-stores also contained within Birks’ flagship Toronto and Vancouver stores. Rolex returns to Birks after a long absence as well, while the company solidifies relationships with other leading luxury brands carried in its various stores.

The store features the expansive private-label Birks Collection merchandise, as well as the company’s extensive offering of diamonds, many of which are Canadian.

It also has a pop-up area in the front of the store where Ms. Hartling said the retailer will regularly have rotating collections and collaborations — the aim is to have something new for guests every time they visit.

Included, as well, is the Birks Concierge Service, which is there to assist clients with such things as creating bespoke jewellery, or to source any of the one-of-a-kind jewels that might be contained in-store. Thee’s also the ‘Birks Lounge’ which offers a chic-looking relaxing area where books and heritage Birks pieces frame a Nespresso coffee station.

The Maison Birks retail store is located at the base of the new Hôtel Birks, which will open towards the end of next month and occupies much of the historic Birks building. The hotel will have between 115 and 120 rooms and will be positioned as high-end. Renderings show a beautiful property with an elegant lobby as well as hotel rooms and common areas (see slideshow above).

A successful launch of its new global concept store in Toronto has given fashion retailer Lacoste Canada a vision to open other similar flagship stores in Vancouver and Montreal over the next two years.

GRÉGOIRE BRASSET. PHOTO: LINKEDIN

Grégoire Brasset, the newly-appointed Vice-President and General Manager for Lacoste Canada, said the French brand launched its new store concept recently in Toronto’s Yorkdale Shopping Centre.

“It’s quite different. We’ve invested a lot in the new concept. We want to be more linked with our DNA and with our history,” said Brasset. “It’s why we decided now to launch this new concept last year in France and now we’re already opened over the last few months 14 doors around the world with the key concept.

“For us it’s a boutique but it’s also a tennis club. It’s also very focused on the Polo business and also we are trying to have a real customer experience and it’s focused on different things. First an omni channel approach which means that you can order your Polo on ecommerce . . . and you can pick it up one hour later at our boutiques. Also, we decided on this new concept to launch Polo customization. For the same price, you can add on your Polo your initials or something like that. You will have a unique Polo.”

Lacoste Store at Yorkdale Shopping Centre

Brasset said Toronto is the company’s main business in Canada, representing about 60 per cent of its sales in the country. That’s why it was chosen as the first new concept store in Canada.

“We would like to launch this new concept in the next two years in Vancouver and one in Montreal,” said Brasset. “It is our flagship. We will have three flagships.”

The new concept store in Toronto was opened in an existing store. It moved from one space to another in Yorkdale. The store in Montreal will be in an existing location but Vancouver will be a new store in the downtown core.

Lacoste Store at Yorkdale Shopping Centre

1 of 4

The first Lacoste store in Canada opened about 25 years ago in Montreal. Currently there are 12 boutique stores across Canada and five outlets. There are also many wholesale stores like Golf Town. It operates its ecommerce site as well.

The successful international brand was co-founded in France by tennis player René Lacoste. The chain known for Polo shirts sells men’s and women’s apparel, accessories, leather goods and sportswear.

Brasset said that besides the additional flagship store in Vancouver he doesn’t anticipate the company will expand the number of other stores it has in Canada.

“We’re thinking we have the right footprint. We don’t want to expand but we don’t also want to close. We are thinking that even if we don’t want to expand the number of stores we can continue to grow our business and also we are thinking for ecommerce we can continue to develop the business and for sure with our main partners like Sporting Life, the Bay, Simons we can continue to develop the business because the business is not only boutique it’s also the business we are doing with our main partners around Canada,” he said.

1 of 4

Brasset said the new concept will help create a stronger brand identity for Lacoste.

“We need to have a story around our products. That’s why this concept is very focused on our story and on our DNA. To be sure that when the customer arrives in this boutique and new concept they understand very quickly that we are a tennis and golf brand . . . because this year for us is our 85th anniversary. It’s a brand with a strong story that has invested a lot in a new concept and a new approach.”

*All photos, except for the top photo, are courtesy of Elaine Fancy.

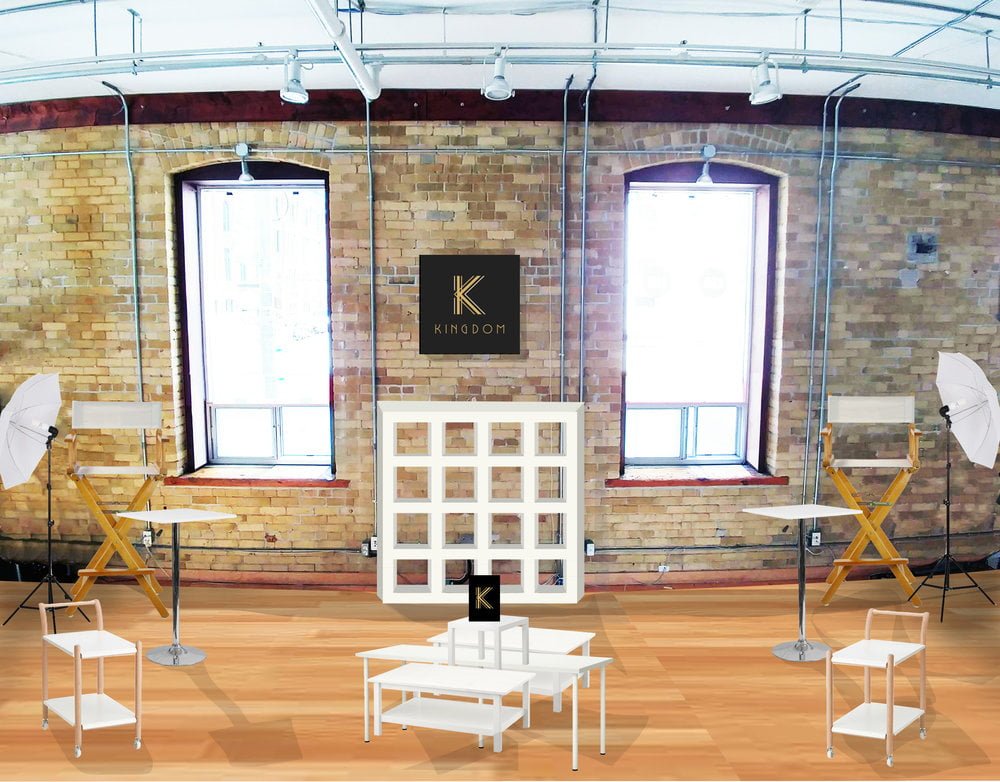

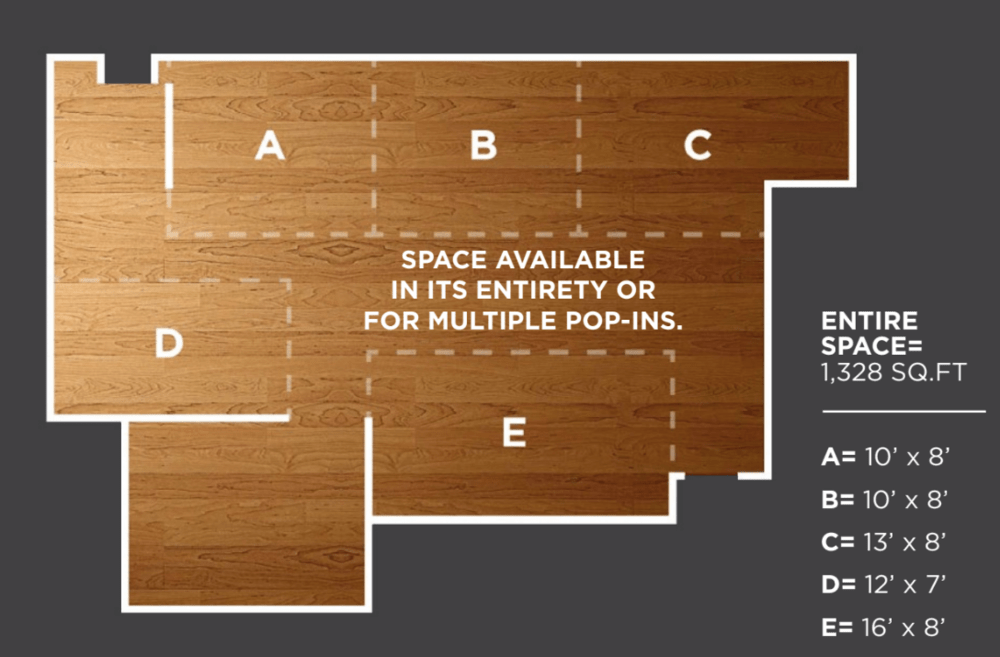

A unique ‘one-stop-shop’ retail space is coming available in downtown Toronto at 276 King Street West, and is being hosted by pop-up retail facilitator pop-up go. The street-level loft-style space can house one tenant or multiple tenants, and is available from now until December of 2018.

Potential ‘Fashion’ Configuration

Called KINGDOM, the 1,330 square foot space has a street front entrance a few steps north of busy King Street West on Ed Mirvish Way. It’s a busy area — more than 40,000 pedestrians pass by daily, and the Entertainment District is otherwise known for its many events and festivals, including the Toronto International Film Festival which takes place in September. The area houses various restaurants and hotels (the Ritz and Shangri-La are nearby) and is also accessible by transit, including street-car as well as the nearby St. Andrew TTC subway station.

The space is being hosted by pop-up go — the company’s Chief Connector, Linda Farha, notes that KINGDOM is a one-stop shop with an opportunity to benefit from pop-up go’s marketing and execution support. The goal is to make the space a ‘turnkey solution’ and as such, pop-up go is also offering services from staffing to social media, retail design, and payment processing to “work like an extension of one’s staff” for whatever tenant, or tenants, choose to lease the temporary space.

Brick walls, high ceilings and an otherwise open concept characterizes the space, which at one time was a fashion retail store. Pop-up go has designed the space so that it can house up to five smaller vendors or even one larger vendor, if desired. The premises includes electricity and heat, air conditioning, washrooms and a kitchen. The space cannot be used for parties or cooking, and pets are not permitted.

")