Despite recession predictions, retail continues its strong post-pandemic growth into 2023, says a new report by commercial real estate firm Colliers.

The consumer appears resilient, with higher savings rates than pre-pandemic, and a huge demand for travel, hospitality, and entertainment. Favourable demographics, particularly strong population growth compared to other developed countries, continues to act as a tailwind for retail sales. Overall sales rose in every province but one, despite shortages in areas such as automotive, said the 2023 Retail Outlook.

“Retail rents reached all-time highs as renewed leasing demand and a lack of new developments funnelled demand to existing centres. Vacancy rates dropped nationwide, as the nadir of retail leasing in 2021 has turned around. Despite high-profile closures of US retailers such as Bed Bath and Beyond and Nordstrom, the vacant space has been rapidly absorbed in most markets,” said Colliers.

“Retail investment continues to be dominated by private investors, as larger institutions and REITs continue to be net sellers. Larger players have also focused on the redevelopment aspect of retail, turning suburban assets into mixed-use developments or land assembly plays.

“Throughout the pandemic, grocery, pharmacy, discount stores, and quick-service restaurants – performed very well. These sectors have continued to attract both customers and investors into 2023, even as restrictions have disappeared . . . The retail industry of Canada has seen a focus on sustainability, partly manifested in the growth of second-hand and vintage apparel, providing an unexpected growth area going forward.”

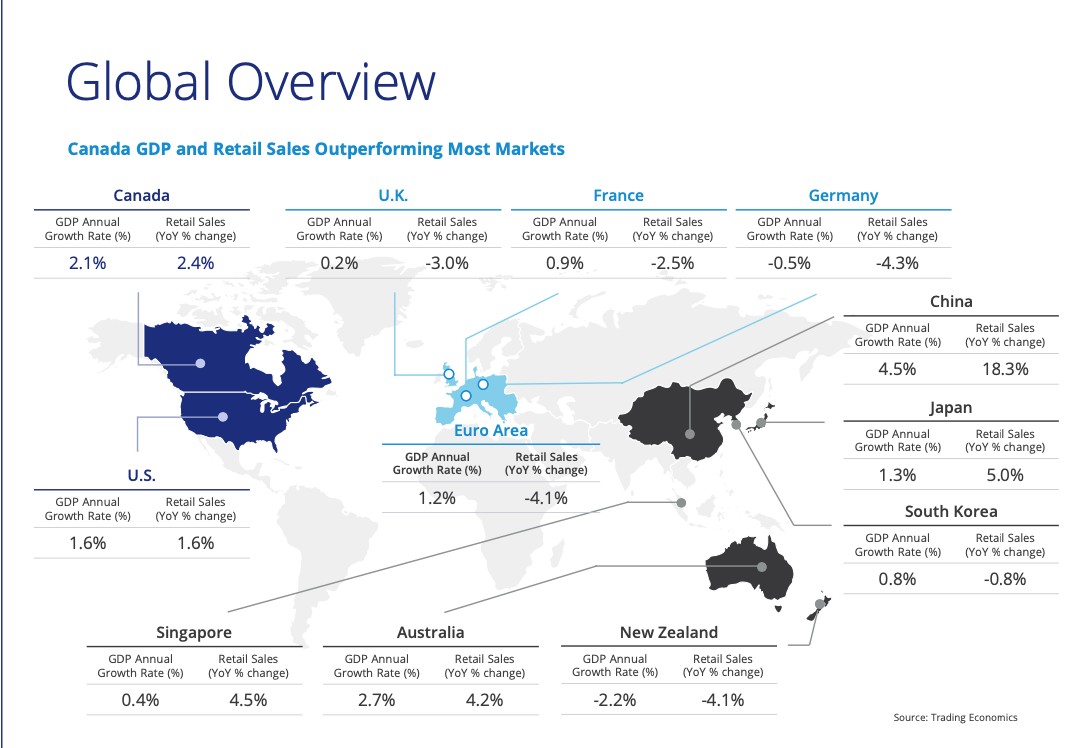

Madeleine Nicholls, Senior Managing Director Brokerage | Vancouver, for Colliers, said the key message from the report is that Canada overall compared to other countries is outperforming many nations in both economic growth and retail sales.

Even with the various interest rate hikes, Canadians have remained resilient when it comes to retail spending, added Nicholls.

The departures of American-based retailers recently have garnered much media attention and headline news but the Canadian retail market has also seen, at the same time, expansion of existing brands and new brands entering the market.

“That’s an indicator of the low vacancy rate that we’re seeing across the country in all segments. When great locations become available, they’re very desirable,” said Nicholls.

She said a few things have fuelled retail spending in Canada including strong employment, population growth and the wealth effect that even during this environment of higher prices from homes to vehicles, people have higher savings than they did pre-pandemic.

Nicholls added that certain retail categories showing year-over-year sales growth is promising, including shoes, clothes, and food and beverage which have been solid and healthy.

“All the provinces are performing really well but what really jumps out is the spending in Alberta and Newfoundland which is extremely high. That’s perhaps driven by the fact that there has been movement to those provinces,” said Nicholls. “And in Alberta’s case, different than the oil boom, people are moving to Alberta now because of the demographic shift of young people moving there in search of affordability for the same reason that people have moved to Newfoundland as well.”

The Colliers report said retail spending dipped in the first quarter of 2023, as the unprecedented interest rate hikes of the prior year took effect. While experts forecast a mild pullback in consumer spending, it is expected to be similar to prior declines, returning to trend within two years. Rate increases of +4.25 per cent in 2022 were intended to address runaway inflation in Canada, a problem shared with much of the rest of the world.

“While inflation nominally helps retail sales numbers, it hurts it overall when we look at spending in real dollars. Clearly there has been some pullback since 2022, where spending peaked in Q2 just as interest rate increases were taking effect. Higher costs of housing, gas, cars and food have squeezed spending elsewhere,” said the report.

“Interest rate hikes have a number of benefits for retail long-term, as the goal of reducing inflation and increased housing costs will hopefully return more spending power to the household. Additionally, higher rates incentivize saving over borrowing, which can create a “wealth effect” where households spend more as they see their assets grow.”

Colliers said the extreme drop during COVID lockdowns led to years of “pent up” demand for everything from international flights to cars to live sports to music events, and the economy is only just now adjusting to these new levels of demand for “experiential” retail.

“Overall retail spending is maintaining a consistent trend, reflecting Canada’s strong population growth and robust labour market. Favourable “fundamentals” are the driver for consistent growth in the retail sector until at least 2025,” added the report.

“Prior to the pandemic, the Canadian consumer was strained, with household savings rates reaching zero or even negative levels. Despite lower inflation, rising costs in several areas combined with weak wage growth was clearly straining households.

“However, one unintended side effect of lockdowns was a drastic improvement for some in household finances. Between mortgage deferrals, income supports, business loans and the reduced costs of working from home, households suddenly experienced savings rates in excess of 20 per cent. There was nothing to spend on (no travel, shortages of many products due to shipping issues caused by lockdown) and households socked away unprecedented savings. This led to a boomerang with the “pent up demand” spending upon reopening, and the subsequent inflation that is only just now subsiding.”

While the closure of a few large occupiers such as Nordstrom garners wide coverage, there has also been a surge of new retail occupiers across Canada, explained Colliers.

“Quick-service restaurants have been thriving for years, with a highly scalable business model that was ideally suited for small urban spaces. Large expansions are planned for a number of occupiers like US stalwarts Taco Bell and Burger King, homegrown brands such as Harvey’s and Mary Brown’s Chicken, and new chains like Egg Club (Ontario) and Columbus Café (Quebec),” said the company.

“In Q1 2023, Goodwill announced a large expansion, planning to open 40 new stores in more affordable markets. Across Canada and the world, second-hand shopping has surged in popularity, to economize in an inflationary environment, support local stores, and for the “thrill of the find” as opposed to the standardized and searchable environment of ecommerce.

“Second-hand shopping also has obvious environmental benefits, which increasingly appeals to customers looking for sustainable retail options. Thrifting intersects with a number of other retail trends, such as a desire for less standardized/”off the rack” fashion, and the rise of influencer marketing – exemplified by the story of a TikTok personality who found a $10,000 vintage Versace dress at a local secondhand shop.”

The report said vacancy declined across several categories from their COVID-era peak, with regional vacancy down five per cent from 2021 and the popular community mall reaching record lows of four per cent. “Destination” shopping centres (super-regional) have performed well and now have vacancy commensurate with neighbourhood retail. The loss of some notable occupiers hasn’t obviously impacted vacancy rates in any class yet, though it’s possible we’ll see the effects later in the year.