By Elizabeth Shobert, Centric Software

The official start of Cyber Week is upon us, and itʼs time to read the signals about where the market stands and what we might expect over the coming month.

This season is shaping up around three contradictory truths all moving at full speed. On one side, value retailers are posting strong earnings and entering Cyber Week with the confidence of clear consumer demand: deep deals, bulk value, and convenience continue to win the day (think TJX, Costco, Walmart). On another, luxury (Hermès, Richemont, LVMH) is humming along on its own frequency, insulated for now by high-income shoppers who havenʼt pulled back, even as the broader market cools…though aspirational shoppers are noticeably more cautious. And running between them is everyone else: department stores, specialty players, mid-tier brands, all caught in a promotional arms race where margins are tight, loyalty is fickle, and algorithmic visibility means everything.

The result is a holiday landscape that feels both energized and, if weʼre honest, a bit uneasy. Shoppers are trading down and trading up simultaneously, hitting Walmart for essentials, Sephora for gifts, and Amazon for everything in between, each channel chosen with sharp intentionality. It isn’t just product retailers are competing on, theyʼre also competing on value perception, storytelling, convenience, and speed. And this Cyber Week, the winners wonʼt be determined by who discounts the most, but by who calibrates best: the smartest promotions, the clearest value proposition, and the most frictionless path from cart to doorstep.

With these themes in the back of our minds, let’s take a look at the latest market data.

Current Market Data

In the US market, weʼre seeing a clear trend: the share of merchandise on sale is running lower than last year, across both apparel and footwear. The clothing gap has narrowed in the past week, but footwear still sits roughly 3-4 points below last yearʼs discount levels, a meaningful signal that US retailers have kept inventories tighter (a necessity for many due to tariff volatility) and have avoided early-season promotional overreach.

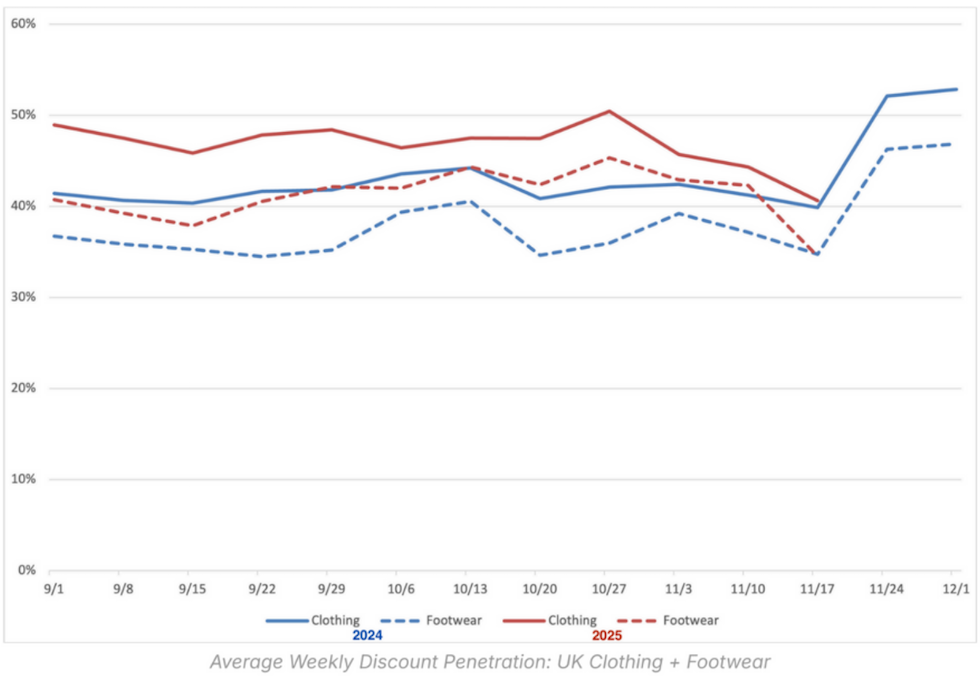

If we look at the UK market, the opposite trend is playing out. This year’s discounting has been tracking higher across both apparel and footwear, although levels have declined slightly over the past few weeks. The macro backdrop: persistent cost-of-living pressure is clearly pushing retailers toward deeper promotional moves earlier in the season.

Where Discounting Is Concentrated

Zooming in, the November markdown landscape reveals just how differently the US and UK entered the season.

In the US, the categories most likely to be on sale were grounded in basics, think cargo pants, chinos, camisoles, even skinny jeans, signaling retailers cleaning up slow-moving apparel without resorting to broad, margin-eroding discounts. Footwear, notably, was largely absent from the list, a sign that American retailers planned conservatively or saw healthier sell-through in shoes.

Across the Atlantic, the story is completely different. UK retailers leaned heavily on promotions, with dresses, skirts and occasionwear posting discount penetration levels north of 55%. Itʼs a much more aggressive stance, suggesting softer consumer demand and greater inventory pressure. Altogether it looks like there will be a far more promotional holiday experience for UK shoppers compared with their US counterparts.

Whatʼs Selling Through at Full Price

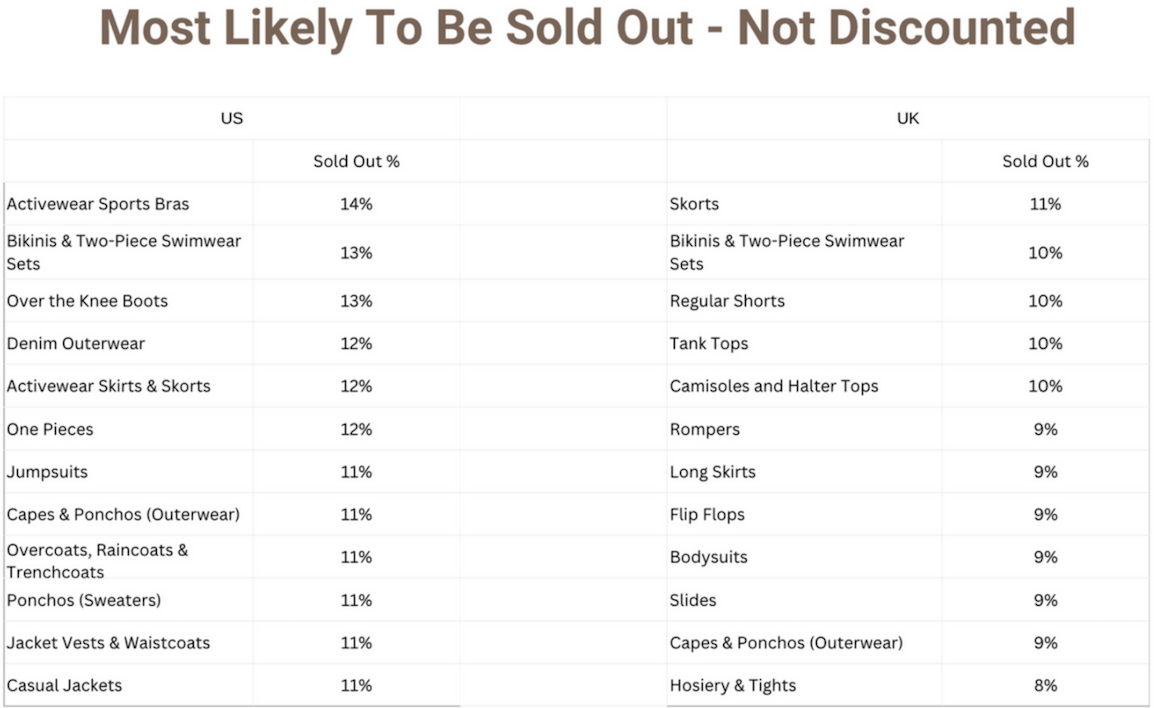

The sold-out data adds another layer, an insight into true demand strength.

In the US, shoppers are snapping up activewear, outerwear, and boots at full price. These are categories with momentum and tight inventory discipline, indicating retailers have anticipated demand accurately and have not needed to discount to move product.

In the UK, the fastest-selling items are lighter, transitional pieces, including skorts, camisoles, swim, and shorts. Itʼs a clear indicator that UK consumers are still reluctant to commit to full-price winter apparel and are favoring seasonless staples and perhaps even planning warm-weather travel.

So What Does This Mean?

All signs point to a holiday season that will unfold unevenly and, in many cases, later than usual. With US shoppers buying selectively and UK consumers waiting for deeper deals, much of the real conversion may not materialize until mid-December, when urgency finally overrides hesitation. That means retailers need to stay agile: inventory thatʼs well-positioned and promotions that can be adjusted in real time will determine who captures this late-season surge.

The divide between markets, and between value, luxury, and the pressured middle, makes a one- size-fits-all strategy impossible. Success this year will hinge on precision: targeted promotions, clear value communication, and operational speed that supports last-minute purchasing. Retailers that stay disciplined now will protect margins and enter 2026 in a stronger position, while those who over- promote early may find themselves out of room when demand actually hits. In a season defined by delay and unpredictability, the winners will be the ones prepared to perform when the clock runs out.

This content was developed in partnership with Retail Insider and Centric Software. To work with Retail Insider, email Craig Patterson at craig@retail-insider.com