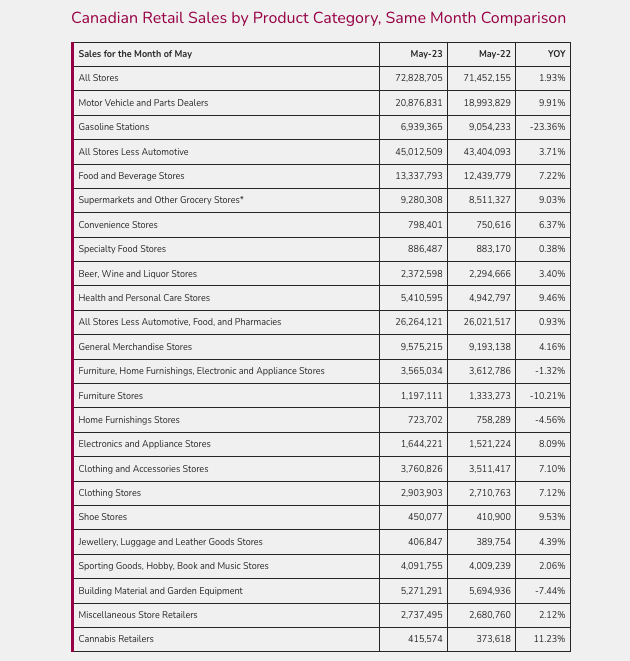

Canadian retail sales continue on a path of minimal growth in May 2023 with All Stores in January growing 1.9% YOY and All stores Less Automotive, Food, Pharmacies up only 0.9% YOY as discretionary spend remains low.

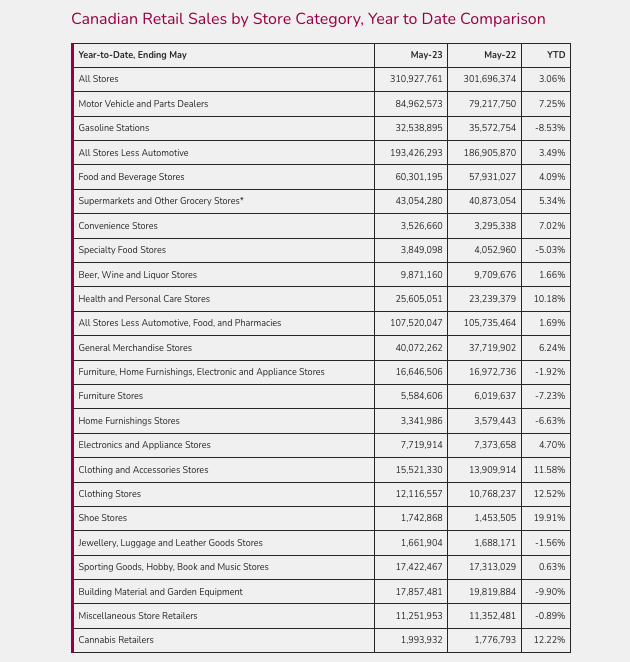

Categories that continue to perform above most others are Clothing Stores, up 7.1% YOY and Shoe Stores, up 9.5% YOY, with the overarching category of Clothing and Accessories Stores still up 11.6% YTD. This growth remains strong and got the JCWG thinking about how these categories are performing over 2019. To our delight, what we found is they are nearly reaching the levels of All Stores (up 23.2% YTD over 2019):

- Clothing Stores are up 19.4% YTD over 2019,

- Shoe Stores are up 16.2% YTD over 2019, and

- Jewellery, Luggage and Leather Goods Stores are up 19.1% YTD over 2019.

For a category that plummeted -80% YOY in April 2020 and did not reach positive growth again until July 2021, this category has shown impressive performance and lockdown recovery. Motor Vehicle and Parts Dealers experienced growth of 9.9% YOY in May, beating out their YTD sales of 7.3%. The JCWG team does not see this as sustainable over the rest of the year, as we are beginning to see reports of EVs piling up on dealer lots. Though brands like Tesla are still beating their supply predictions, it seems that demand has not quite met up, regardless of pay cuts. Consumers just aren’t able to buy cars when their costs of living keep increasing, and so do the financing/leasing rates of a new vehicle due to rate hikes. We predict that these sales will begin to dip soon, regardless of lower prices and increased competition that continue to flood the market.

Housing remains top of mind for Canadians, especially in larger cities like Toronto and Vancouver, as rental rates continue to rise along with mortgage rates. As such, categories associated with housing are all declining as a sign of the times:

- Furniture Stores are down -10.2% YOY,

- Home Furnishings Stores are down -4.6% YOY, and

- Building Material and Garden Equipment are down -7.4% YOY.

As the price to rent/own a home continues to increase over the rate of wages, these categories will likely continue to suffer. The more people are needing to spend on housing, the less they will have to be able to spend on furniture, gardening, etc. for the home.

It’s almost the end of July, meaning we are about to head into back-to-school! As we rapidly approach this season, we are thinking about:

- Will parents be able to purchase back-to-school related products as they did in previous years with the increased cost of housing and groceries?

- When will students start their purchasing this year? Will this follow the trend of Black Friday and Boxing Day sales moving further and further ahead?

- What channels are most appealing to parents and children as they prepare their lists?

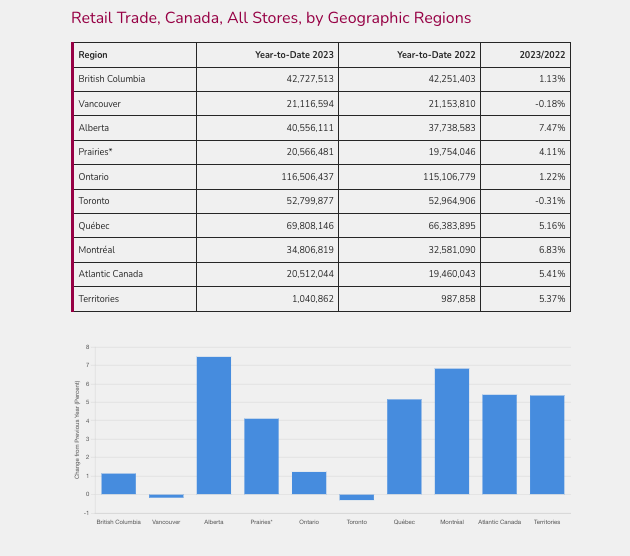

- Will Toronto and Vancouver (down -0.3% and -0.2% YTD) stop feeling the brunt of the retail sales decreases?

- How are YOU preparing for increases in back-to-school traffic?

For support in your seasonal retail strategy and adapting to market conditions, reach out to the trusted experience at JCWG!