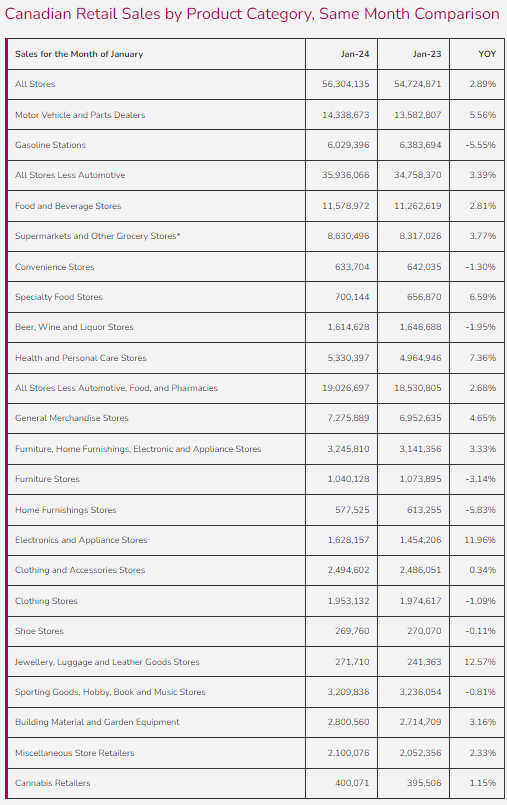

January kicked off with stronger growth than December for Canadian retail sales, growing 2.9% YOY for All Stores. Discretionary spending grew to a similar degree, increasing 2.7% YOY for All Stores Less Automotive, Food, and Pharmacies. The year-to-date sales grew in 2023 over 2022 to 2.1% and 0.4% respectively.

Food and Beverage Stores experienced growth around the rate of inflation (3.4%), with sales increasing only 2.8% YOY. There was, however, some noticeable polarity within the category, specifically:

- Convenience Stores fell -1.3% YOY in January. Notably, Couche Tard reported negative results for the first quarter of the 2024 calendar year in line with trend. There are numerous factors mentioned including convenience stores tied to slowing gas sales and lower-income consumers continuing to be strained. Couche notes that they are currently looking at expanding their private label and improving their loyalty program.

- Specialty Food Stores grew an impressive 6.6% YOY. This could be a result of the continued frustration of consumers with Canadian grocery giants. There has also been a trend in consumers increasing the number of shopping trips and lowering basket size, which bodes well for smaller, local grocers. In addition, RBC cardholder data indicated that consumers were cutting back on restaurant spending in January, which may be being redistributed towards Specialty Food Stores.

- Beer, Wine, and Liquor Stores continue to struggle in January, with sales decreasing -2.0% YOY. Many people cut back on drinking in the new year, but this is seemingly more widespread as 2023 experienced lower sales throughout the year.

Consumers increased their spending on Jewellery, Luggage, and Leather Goods Stores in January with sales growing 12.6% YOY. This can likely be attributed to two main factors: Valentine’s Day and impending travel.

- Valentine’s Day obviously has a large effect on the jewellery category, but travel may be affected now as well. As younger generations tend to prefer experiences over products, it is possible that they are deciding to take a small trip together rather than purchase jewellery.

- The RBC report indicated that there was a significant increase in online travel bookings, indicating that consumers are planning more travel in 2024. In Ontario, there has been limited snow, so people are opting to travel to other regions to take part in 2024’s ski season.

Looking forward to the rest of 2024, there are numerous trends to watch. According to recent RCC studies, consumers are expecting to maintain or increase their 2024 budgets which could be good or bad for business depending on its 2023 performance. For example, March will be interesting to watch as 84% of consumers expect to spend the same or more than 2023 during March Break, and 83% for Valentine’s Day. This is a promising statistic for travel, experiences, and jewellery, but can be a negative statistics for categories less associated with these time periods. There is not necessarily much more discretionary spending for Canadian consumers this year, but they may be planning to spend it much differently. In addition to this, as mentioned last month, Canadian Tire experienced poor performance in Q4 2023, and expressed that this is a foreshadowing of what’s to come. As we continue through 2024, JCWG is thinking about:

- Canada has been closely following the US retail sales trends recently. With that, will Canada experience a successful “leap year” February as the US did?

- Did consumers spend on experiences or products for 2024’s Valentine’s Day with their continued limited discretionary budget?

- With travel bookings increasing, where will we see the biggest increases in spend in Canada? Are consumers actually flocking to the mountains (BC, Alberta) or are they writing off the whole season and spending their money in the Caribbean?

- How have YOU changed your business’ budget for 2024 with all the changes that lay ahead?

For support with building an actionable retail strategy, reach out to the trusted experience at JCWG!

Thank you J.C. Williams Group for this report.

{kind=link}