The unique KARE furniture brand will look at expanding in Canada, and perhaps into the United States, after recently completing renovations to a flagship Toronto showroom which was the Munich-based retailer’s first location in North America.

Edilka Anderson, owner of KARE Toronto on Queen Street West, said the store has been newly-renovated with a stunning assortment of unique and beautifully-crafted accessories, lighting, furniture, and textiles to suit any home and style.

Anderson bought the 2,200-square-foot showroom at 553 Queen Street West in Toronto in May from the original owners who opened in the summer of 2017. The showroom was closed for about two weeks during the recent renovations.

“I created a concept in a way where we created small rooms. We can sort of showcase a living room, and then a dining room and so forth. In the way that it’s set up it’s almost the way you walk into an IKEA where you go into kind of like a maze,” explained Anderson. “I sort of made that concept so we could showcase the pieces. It’s not just a furniture store. It’s a design company.”

Edilka Anderson, owner of KARE Toronto

“My goal is to expand the showroom because we’re on Queen Street West and you don’t have the bigger stores here. But I do have a very large basement so I can double up my square footage by renovating my basement which is my goal. I plan on doing that hopefully by next Spring, next Summer. I would like to be able to double up the square footage of the showroom to be able to showcase more pieces.”

KARE was founded in 1981 in Munich by two designers, Jurgen Reiter and Peter Schonhofen. Over the years, it has become an international brand with a presence in more than 50 countries and more than 100 stores worldwide, mainly in Europe.

“The brand is really inspirational. They pride themselves in being inspirational instead of conventional. It’s everything but ordinary,” said Anderson. “And we have some really fun and unique designs. We have everything from accessories to furnishings to lighting. So we can basically do an entire home.”

“We have over 5,000 items on our website. We can’t carry everything (in the showroom). So we do sort of try to keep things fresh. And most of our orders from furnishings are through special orders.”

Customers receive a design and style magazine that showcases some of the new pieces the company gets in and twice a year KARE has a new collection.

“It’s always innovating and doing new things. We also have a couture book. It’s basically a coffee table book and it’s done every year. It’s a beautiful book and it has all of our items in it. It’s really well done. We use those a lot in working with our designers so they can have marketing material and things to offer their clients so that they can see,” said Anderson.

That includes a unique retail, in-store experience with augmented reality glasses.

“When we do a design project, we do a 3D design. So we do it on any type of software that you can use. We can use our furniture. Pieces are in that software. We have 3D glasses . . . You can view your room that we designed for you in 3D and you can literally walk in the room,” said Anderson. “They tested this in a market in Munich in some of the larger stores and the results that came from it was excellent in terms of selling more of the room because the person felt like they were walking in their own space and could see themselves in it. It’s very innovative.”

The Toronto KARE location is the only one currently in North America but Anderson said the company definitely wants to expand the brand in the future.

“With us being the only store in North America currently, everybody’s watching us. All eyes are on us. I think it’s a good opportunity for us to have something a little bit different. This brand and this store is not like any other store – furniture store – that you walk into. You definitely get variety and something completely unique,” said Anderson.

“I know that my plan is to expand here in Toronto and once we see the market respond really well I believe that there will be other stores opening in Canada and even in the U.S.”

Canada’s retail industry has seen a dramatic shift in recent years due to technological advancements. Fintech and retail solutions are now knocking on the doors of the big brands, desperate to help reshape the future of commerce and finance in this sector.

As retail faces new challenges, many are hopeful that these products and solutions will boost sales, improve operations and impact customers in the best way possible. Already, these solutions are in full swing working to harness real-time customer and point of sale (POS) insights, to reach customers across mobile channels, and to ensure visibility in all areas of production.

In 2016, over 1,500 fintech startups applied to MasterCard Start Path Global, in an effort to support startups to connect with some of the largest names in banking, retail and technology. As more fintech and startups begin cropping up in Canada’s retail space, it is becoming harder to be picked out by the top global brands. Therefore to impress the roster of retail A-players, Canadian startups need to build a solution that makes it hard for them to say ‘no’ to.

Identifying the issue, providing a suitable tech solution and proving this new approach actually works is essential to winning a business over in any industry. Here are a few steps we took at Jifiti to approach retailers and convince them to give us the green light in delivering reliable retail solutions to their stores.

Avoid the ‘I’ Word

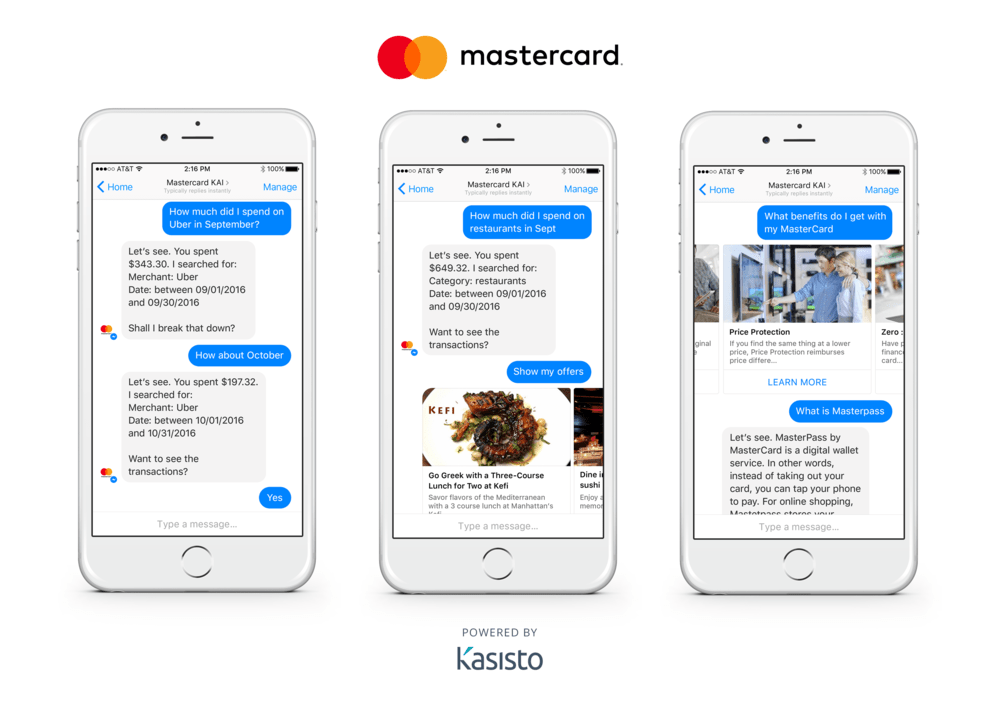

Image: Mastercard and Kasisto

Retailers will lose interest if any mention of integration is uttered. Retailers want a hassle free solution that requires little, or no adjustments, or resources from their part. To grab their attention, show that the solution can work seamlessly with the retailers existing systems, rather than having to integrate with it. Solutions that are creative should be able to supply a working solution that visibly solves a problem, or eases business, without needing full integration on the retailer’s end – at least in the initial stages.

This may mean that some processes are accomplished manually on the startup’s side, but there is nothing wrong with that. The goal is to offer the solution on a silver platter without the partner needing to invest time and resources in the early phases. What takes place behind the scenes with the product is completely up to the startup team. Don’t be afraid to dumb things down, or solve issues manually to avoid interruption and run a proof of concept. Having everything automated is surprisingly not a top priority for retailers. Instead, they appreciate startups who can creatively solve their issue without having to mention the dreaded need for integration.

Use a Middleman

Startups need to recognise that with the level of competition in their space, one way forward is to partner with a middleman to get solutions up and running. Partnering with a seperate player in the field can not only allow startups to utilize outside assets to improve their current solution and avoid needing integration with the client, but it can also put these startups on the map. Linking up with well-known corporations in and outside of Canada will grant startups the use of existing infrastructure, giving them a lift up the industry ladder.

Thanks to Prime Minister Trudeau’s recent efforts and initiatives in supporting Canadian businesses and commerce, it should be easier for Canadian retail startups to find these potential partners. His successful bid to host Collision, one of the largest tech conferences in North America, has already thrown the spotlight on Toronto and its bubbling tech ecosystem. Trudeau’s trip to Silicon Valley, including a visit to Amazon where he met CEO Jeff Bezos, has also encouraged big names to invest and look for partnerships in Canada. Specific interest in retail was sparked last year when AI-enabled intelligence company Rubikloud landed a $37 million investment. With more eyes watching Canada’s startup scene, finding the middle man to help kickstart your retail solution should be a top priority.

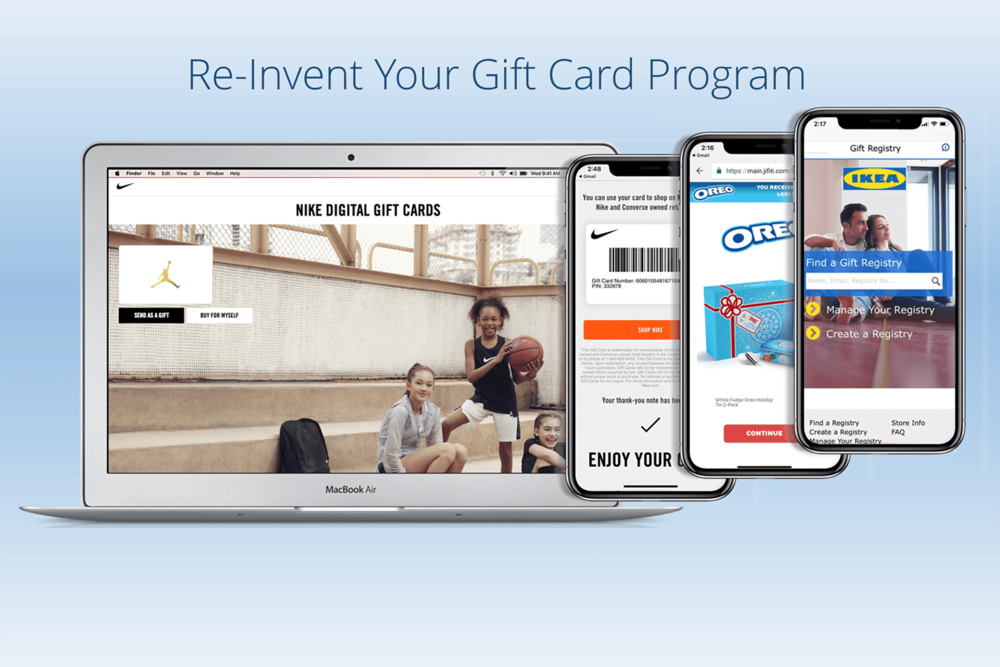

At Jifiti, we collaborated with Mastercard to offer retailers a zero-integration option for our platforms. Thanks to the international credit cards technological infrastructure we are able to offer a seamless transfer of funds between our gift registry and consumer financing platforms without requirements from the retailers own management system. This collaboration has let us work with large retailers such as Ikea and others to implement our retail solutions on their sites. Therefore, building a solution that does not require resources on the retailers end is one step towards partnering with some of the big brands.

Show Results

Image: Nike Gift Cards

Assuming a startup can provide a solution without needing full integration immediately within the retailers own internal system, then proving that the solution works across the board is the next step. Once positive results appear, retailers will not require any other convincing and will be inclined to prioritize their time and resources to work with the startup.

Reiterating the previous point, results do not necessarily need to stem from automated solutions. Proving the solution can be processed manually first to run tests and show results is a great first step. The solution can always then be upgraded once the retailer has seen results and is onboard. This is what we achieved at Jifiti when partnering with Nike. We first launched a gift card promotions platform with them using a middle man, however, once Nike saw the success from our platform and how it increased sales and lowered fraud, they agreed on direct integration with their gift card processor.

Presenting results to the retailer involves communication and time. It’s important to set out KPIs with the partnered retailer to ensure both startup and retailer are on the same page on what exactly is being tested and what results they are looking for. This could be sales, brand awareness, user acquisition etc. Laying these expectations out up front will allow startups to prove their point to the retailer and then move on to discuss investing resources and further development.

Retailers in Canada and the rest of the world are in no way turning their backs on technological solutions and the startups offering them. They are looking to innovate and to do so they need the combined benefits of a streamlined shopping experience and new tech to stay ahead of the competition. However, retailers, particularly the big brands, will be more inclined to test new solutions from smaller startups if it does not interfere with their ongoing pipeline and budget and if it can be worked seamlessly into the brand’s existing software. Therefore, to increase their chances, Canadian startups should keep these three pointers in mind when developing and pitching their solution to retailers. It could significantly lower the entrance barrier to testing and launching with some of the larger brands in the retail industry.

Iconic athlete and former Toronto Blue Jays star Jose Bautista joins Endy, Canada's leading online mattress brand, as investor. (CNW Group/Endy (Overwater Ltd.))

Toronto-based mattress-in-a-box brand Endy announced that it has partnered with professional baseball player José Bautista, who was with the Toronto Blue Jays from 2008 to 2017. Mr. Bautista is an investor in the company, as well as a spokesperson. Endy is one of several mattress-in-a-box brands that are fighting for market share in Canada and thus far, the company is maintaining its number one position in terms of sales.

Mr. Bautista announced his association with Endy this week as part of an ongoing promotion for the brand as it continues to seek brand awareness across the country.

“Endy is an incredible Canadian success story. This is a company that continues to make a name for itself, not only for flipping an industry on its head, but for donating thousands of mattresses to those in need,” said Mr. Bautista. “As an investor, I’m proud to team up with Endy, a company whose values I share: innovation, well-being, and paying it forward.” Being a fan of the mattress as an end-user as well, he said, “Over the past two years, I’ve become close with the Company’s founders, Rajen and Mike, and their desire to give back to the city of Toronto and the country of Canada that I had made my home for the past 10 years – I knew I had to get involved.”

PHOTO: ENDY FACEBOOK PROFILE

Despite increasing competition, the company is seeing rapid year-over-year growth of 300%, resulting both from expansive marketing efforts as well as consistently high ratings among purchasers. Growth has been so rapid that the company also recently announced that it is opening a distribution centre for Western Canada in suburban Vancouver to keep up with the demand.

Endy was founded in 2015 as an online ‘sleep brand’ and the company is in line to do in excess of $50-million in sales this year. Canada is Endy’s target market and remarkably, the company’s revenue is now about 10% of that of Sleep Country Canada, which is the largest bedding retailer in the country with more than 250 brick-and-mortar stores as well as expansive e-commerce.

Since its launch about three years ago, Endy has partnered with local charities from coast-to-coast to donate new and gently used mattresses to families and individuals in need. Endy has distributed more than 2000 mattresses through its charity partners in every Canadian province, including Furniture Bank (Toronto), Matthew House (Ottawa), Women in Need Society(Calgary), Aboriginal Mother Centre Society (Vancouver), as well as several others. The company has also supported global charitable organizations including Nothing But Nets and Mr. Bautista’s own foundation, the Bautista Family Education Fund, which provides assistance to student athletes, both on and off the field.

ENDY FACTORY IN MONTREAL. PHOTO: ENDY FACEBOOK PROFILE

Advertising had been initially focused on urban areas with the young urban professional being an important target market. Expansive campaigns with entities such at Toronto’s TTC has seen Endy advertising occupy entire subway cars in an effort gain brand awareness to the hundreds of thousands who ride the system daily. Endy is now expanding its advertising to suburban and other parts of Canada, not to mention the newly announced Bautista partnership.

The mattress-in-a-box concept is still relatively new and yet its business is exploding in Canada. Competitor Casper, which recently opened its first Canadian store at CF Sherway Gardens and will soon announce a second store in downtown Toronto, also has celebrity backers including Leonardo DiCaprio, Tobey Maguire, Adam Levine and Ashton Kutcher.

Various other brands continue to enter the market, such as Leesa and Tuft & Needle, with more brands seemingly coming online every week. There’s even now a plant-based mattress called Haven Mattress Company, based in Kelowna. Sleep Country Canada also recently introduced UK-based brand Simba — the premium ‘Hybrid®’ mattress-in-a-box brand has sold more than 150,000 mattresses across Europe. Sleep Country also unveiled its in-house mattress-in-a-box brand Bloom which is also carried across the chain.

ARTIST’S RENDERING OF UNIQLO SQUARE ONE SHOPPING CENTRE (CNW GROUP/UNIQLO CANADA)

Popular Japanese fashion retailer UNIQLO has revealed the opening dates of its next four Canadian stores. When all are open by the beginning of November of this year, the company will have almost doubled its Canadian store count over an eight-week time span.

UNIQLO currently operates five stores in Canada — two in Toronto and three in the Vancouver area. More store announcements are expected soon as lease deals are finalized, according to landlords, not including the four confirmed locations that have been revealed to the public.

Of the four confirmed UNIQLO stores, three are in the Greater Toronto area and one is in the Vancouver area.

“Encouraged by the warm welcome we have had to date, we are thrilled to be opening three new stores in the Greater Toronto Area and a fourth new store in Greater Vancouver,” said Yasuhiro Hayashi, Chief Operating Officer of UNIQLO Canada. “We’re excited these four new stores will allow more people to discover LifeWear, thoughtfully created to make everyday life better and more comfortable.”

RENDERING OF METROTOWN (BURNABY, BC) EXPANSION. PHOTO: UNIQLO

The British Columbia store opening comes first, taking place on Friday, September 14. The 15,970 square foot store, which will include about 12,000 square feet of retail space, will open in the former Old Navy at Coquitlam Centre. The store will be located on the mall’s second level, according to floorpans by landlord Morguard. Coquitlam Centre’s UNIQLO will be the fourth location in the Vancouver area and for a two-week timespan, Vancouver will have double the number of UNIQLO stores compared to Toronto.

That will change on Friday, September 28, when UNIQLO opens a 28,150 square foot location at Vaughan Mills, just north of Toronto. The store will have about 20,000 square feet of retail space and will be located where Holt Renfrew’s off-price concept HR2 was located before it shuttered in December of 2017.

On Friday October 12, UNIQLO’s next Canadian store will open at the CF Markville shopping centre in Markham, also north of Toronto. The 18,560 square foot store will include about 15,000 square feet of retail space in the mall’s former Forever 21 location.

And on November 2, 2018, UNIQLO will unveil a 19,850 square foot store at Square One in Mississauga, which will include about 15,000 square feet of retail space. UNIQLO’s location at Square One is remarkable as it has been carved out of the mall’s former Target space — Target exited Canada in 2015 and prior to Target, Zellers occupied the premises. Entertainment concept The Rec Room will open nearby in the spring of 2019 as well as a new ‘food district’ market that is also expected to open in the fall of 2019.

All four stores above open at 10:00am and according to UNIQLO, one HEATTECH item will be given away to the first 500 customers who make a purchase on opening day of each new store. As well, people will be encouraged to ‘Spin The Wheel’ for the chance to win free items or discounts between 2:00pm-5:00pm.

[CF RICHMOND CENTRE GRAND OPENING ON FRIDAY, APRIL 6. PHOTO: RITCHIE PO]

YORKDALE MALL LOCATION. PHOTO: RETAIL INSIDER

When all four stores are open, the Greater Toronto Area will be home to five UNIQLO stores, while Vancouver will be home to four locations.

The first two Toronto stores, both of which opened in the fall of 2016, are considerably larger than all of the stores that have opened in British Columbia to date. The CF Toronto Eaton Centre store, which opened in September of 2016, spans about 33,400 square feet over two levels in part of the mall’s Sears space which has since been repurposed to house Nordstrom, Samsung and several smaller retailers on the mall’s second level.

The Yorkdale UNIQLO store opened in October of 2016 and spans more than 30,000 square feet over two floors. For a period of about a year, Toronto was the only market in Canada to boast any UNIQLO locations.

That changed in October of 2017 when UNIQLO unveiled its 20,630 square foot two-level store at Metropolis at Metrotown in Burnaby. Several months later, in March of 2018, UNIQLO opened a 12,800 square foot store at Guildford Town Centre in Surrey. In April, UNIQLO opened its third Vancouver-area store in Richmond when it unveiled an 8,010 square foot one-level unit at CF Richmond Centre.

WASHINGTON DC LOCATION. PHOTO: UNIQLOTOKYO FLAGSHIP LOCATION. PHOTO: RETAIL DESIGN BLOG

UNIQLO is expected to expand its base of stores into secondary markets in Canada such as Edmonton, Calgary and Ottawa at some point, though the company hasn’t provided a timeline. Toronto and Vancouver might be considered to be strategic moves as UNIQLO looks to expand brand awareness in the country, similar to what it has done in the United States. There, UNIQLO started opening stores in New York and California before expanding further into markets such as Chicago and Boston.

Those in Canada living outside of Ontario and BC can now buy UNIQLO items online with its recently launched mobile e-commerce platform that also has core items available in an extended range of sizes from XXS to 2XL.

ABOVE: LAVAL, QUEBEC LOCATION (OPENING SOON). PHOTO: LEE VALLEY

Ottawa-based Lee Valley Tools, known for its tools and gifts for woodworking, crafting and gardening, is expanding its store operations into to province of Quebec. This fall, the company will unveil one of its efficiently laid out ‘new format’ stores in suburban Montreal, and more stores for Quebec are anticipated.

CEO Robin Lee said that the Laval Store will be different than many of Lee Valley’s existing stores, as the retailer adopts a new and more efficient store format which includes more retail space at the front of its stores and less back-of-house/storage than its previous locations. In the company’s older locations, about 1/3 of the store’s square footage is for consumers to view products, while the back 2/3 of the store was dedicated to storage and other back-of-house activities. New stores have inverted the ratio with the majority of selling space being dedicated to shoppers, and less at the back.

ABOVE: GOOGLE MAP OF NEW LAVAL LOCATION. BELOW: PHOTOS OF WINDSOR STORE WITH NEW FORMAT

1 of 4

Lee Valley’s first store in Quebec will be at Centre Laval; located at 1600 Boulevard Le Corbusier, Unit 31 B in Laval, spanning nearly 25,000 square feet. Laval is an upscale suburb of Montreal which is also known to have the region’s leading shopping mall, CF Carrefour Laval.

Other ‘new format’ Lee Valley stores include units in Kingston, Kelowna, Windsor and Niagara Falls — these are also the company’s most recent locations to open, as the company perfects its store design. The newer stores feature a ‘pathway’ configuration which encourages discovery and activity, according to Mr. Lee. Merchandising is also done in ‘pods’ so as to be more interactive, in order to create an experience which is also educational.

The company’s new format stores are usually a bit smaller than the company’s typical stores overall, and will measure generally in the 15-16,000 square foot sales floor range. The Laval store will offer an expanded sales floor for the Quebec market with space exceeding 11,000 square feet. All of the new Lee Valley stores feel larger than traditional Lee Valley stores because of larger front-of-house space for shoppers.

WINDSOR LOCATION. PHOTO: LEE VALLEY WEBSITE

Lee Valley Showroom Construction

1 of 12

Lee Valley Warehouse Construction

1 of 3

[Above: Construction Photos of the new Laval store. Photos: Lee Valley Website]

The idea is to make Lee Valley stores interactive, and it’s working. The retailer has a fiercely loyal client base that is growing, and Lee Valley is also targeting a younger demographic that is also seeking to be ‘makers’ — society spends a lot of time in front of screens, and some are finding value in making things with their own hands.

“Physical retail needs to be less transactional and more educational,” said Mr. Lee, going on to explain that good retail can be considered to be akin to “theatre”. Ultimately, it comes down to the in-store experience, especially at a time when consumers can shop online.

While no locations have been confirmed, Mr. Lee said that Lee Valley could open two more stores in the Montreal area as well as one in Quebec City — expansion will depend on space and the Laval store is being used as something of a test site.

Robin Lee is the son of Leonard and Lorraine Lee, who founded Lee Valley in 1977. The company now employs more than 1,000 people coast-to-coast, with 19 stores as well as an engaging e-commerce website. Staff are empowered to provide the best advice to the customer regardless of whether or not an interaction results in a sale, and the company shares profits with its employees. Physical retail and mail-order/e-commerce are both significant components to its business model.

Lee Valley also has a manufacturing arm called Veritas Tools, which makes woodworking hand-tools, including hand planes, marking gauges and other measuring tools, router tables, sharpening systems, saws tools, and numerous other gadgets. Veritas does research and development activities for the factory line and has developed and patented many innovative designs.

Robin Lee, CEO of Ottawa-based Lee Valley Tools, was recently presented the 2018 Retail Council of Canada Excellence in Retailing Awards Lifetime Achievement Award as part of the Retail Council of Canada Store 2018 Conference. He was also recently featured in Retail Council of Canada’s Canadian Retailer magazine.

Iconic Canadian footwear chain Town Shoes will cease to exist after 66 years in business. The company has 38 stores across Canada, and the announcement will be of concern to some landlords that are already grappling with vacancies in their malls.

American parent company DSW Designer Shoe Warehouse paid $62-million when it bought a 44% stake in Town Shoes in the spring of 2014. That deal helped DSW open its large format concept stores in Canada — Town Shoes’ expertise and distribution network were utilized as part of the expansion which saw 27 DSW stores open in regions across Canada.

SUNNYBROOK PLAZA IN TORONTO. PHOTO: GOOGLE MAPS

LAWRENCE PLAZA IN TORONTO. PHOTO: GOOGLE MAPS

DSW acquired a 100% stake in Town Shoes in May of 2018 and at the time, we were told by suppliers that they had been informed that the Town Shoes nameplate would be shuttered. That information was denied by the company and thus was not reported in Retail Insider. Now DSW confirms that all Town Shoes stores in Canada will be closing by the end of its fiscal year.

Town Shoes has an extensive history in Canada. It was founded by entrepreneur Leonard Simpson in 1952 when he took over a failing store at the Sunnybrook Plaza in Toronto (the shopping mall was a new concept at the time). A second location opened soon after at the ‘Lawrence Plaza’ which is located south of the Yorkdale Shopping Centre.

Town Shoes founder Leonard Simpson

Town Shoes founder Leonard Simpson

In the 1960’s, Town Shoes opened a shop-in-store on Toronto’s ‘Mink Mile’ inside of upscale multi-brand retailer Harridge’s at 131 Bloor Street West in The Colonnade, and the company maintained a Bloor Street West presence thereafter until last summer when it closed its standalone store at 95 Bloor Street West. That retail space is currently occupied by menswear retailer Strellson.

Town Shoes was also a sponsor of Toronto Fashion Week for many seasons, supplying shoes for the runway shows. The company was also known to have collaborated with Canadian designers on exclusive lines. Town Shoes has a close tie to the fashion world in Canada and the news of its closure will be shocking for many.

Michael J. Armstrong is an Associate professor of operations research, Goodman School of Business, Brock University. He teaches courses on quality improvement, game theory, and operations management. He holds a PhD in management science from the University of British Columbia, an MBA from the University of Ottawa, and a BSc from the Royal Military College of Canada. Before his academic career, Armstrong was an aircraft maintenance manager. He holds several certifications from the American Society for Quality, including a six sigma black belt in quality improvement.

While cannabis shortages do exist, federal officials disagree. Bill Blair, the minister leading Cannabis Act implementation, has repeatedly said supplies are “adequate” and even “exceed existing demand.”

How the Ford government decides to regulate retailers will have a major impact on how many retailers will get into the business — potentially thousands of distribution points are possible in the province, in contrast to just 51 in Saskatchewan and 30 in Newfoundland.

Ontario’s change to private sector cannabis stores will give consumers more convenience. That will mean stronger competition against the black market, but potentially higher consumption too.

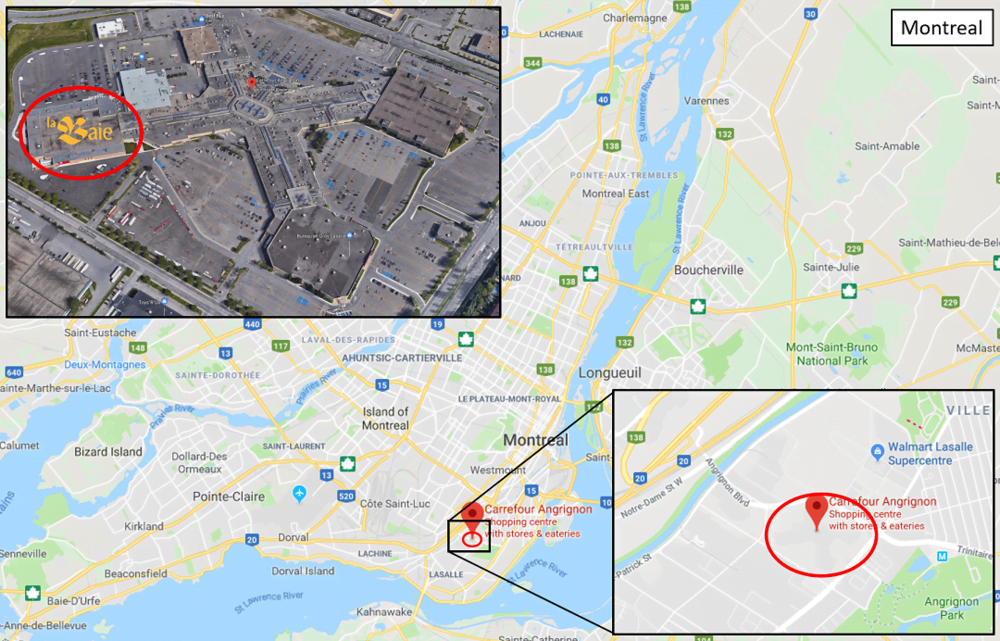

Toronto-based department store chain Hudson’s Bay has opened its first newly-built store in almost 15 years in a suburban Montreal shopping centre. The opening represents something that we’ll be seeing a lot less of in Canada moving forward — a traditional department store opening a new location, at a time when mall landlords are looking to other concepts to anchor and draw-in consumers.

The 129,000 square foot Hudson’s Bay store is located at the Carrefour Angrignon Shopping Centre in LaSalle, located about six kilometres south of Montreal’s downtown core. The new store features the typical departments found at Hudson’s Bay including fashions for women, men and children as well as footwear, leather goods and accessories, major home fashions and Hudson’s Bay’s new toy department. The store also features an expanded assortment of beauty and cosmetics. Its design reflects Hudson’s Bay’s updated interior aesthetic which features bright lighting and attractive interiors — some existing stores have seen such renovations, though many suburban stores leave something to be desired.

“We’re excited to extend the Hudson’s Bay footprint in Quebec with our opening in LaSalle,” said Alison Coville, President of Hudson’s Bay. “Hudson’s Bay prides itself on providing new and exciting experiences for our customers and we look forward to joining the LaSalle community.”

The last time Hudson’s Bay opened a new full-line store was in the year 2003 when it unveiled its 212,000 square foot location at CF Polo Park in Winnipeg. That store replaced a former Eaton’s location in the mall.

The store’s grand opening over the weekend featured Vanessa Grimaldi of ABC’s “The Bachelor,” who hosted the store’s official ribbon-cutting ceremony. There were also appearances throughout the weekend by Canadian Olympic Athletes Max Parrot, Philippe Gagné and Joseph Polossifakis, as well as Celebrity Chef Chuck Hughes.

The new Carrefour Angrignon Hudson’s Bay replaces a Target store which operated in the mall for a couple of years — Target exited the Canadian market in early 2015 after a disastrous expansion which saw it lose billions of dollars in the process.

Carrefour Angrignon spans about 850,000 square feet, making it one of the largest fashion shopping malls in the Greater Montreal area — it services the trade areas of LaSalle, Nuns’ Island, Montréal, Lachine, Montréal West, N.D.G., Côte Saint-Luc, Dorval and Châteauguay (representing a population of about 612,000 people). Annual sales are in excess of $430/square foot according to landlord Westcliff’s leasing site, with the centre seeing about 6.5-million visitors.

Hudson’s Bay operates 12 stores in the Montreal area, including a 650,000 square foot multi-level flagship in the city’s downtown core, as well as smaller units in suburban malls. That store count will be reduced to 11 this fall with the closure of its location at the Le Boulevard shopping centre — we recently profiled potential redevelopment opportunities for that mall space, with options including smaller anchors as well as larger-format food-and-beverage offerings.

We’re unaware of any plans for future Hudson’s Bay stores anywhere else in Canada at this time — department stores are something of a remnant from the past in North America, and some landlords are even saying that they’re not interested in including such traditional large anchors in their malls. There are numerous examples of this and one notable example in Montreal is the massive Royalmount project which will open in several years time. Instead of department stores, the centre’s anchors will include an expansive mix of food and beverage offerings as well as entertainment and other attractions that are expected to draw shoppers from the region.

Smaller specialty anchor stores are still expanding their operations in Canada, however. TJX Companies’ brands Winners, HomeSense and Marshalls are all expanding their base of stores in Canada, in some cases taking part of the retail space once occupied by larger retailers such as Sears Canada and Target. ‘Cultural department store’ chain Indigo is also utilizing the opportunity to replace many of its older-format Indigo and Chapters stores by building new concept Indigo-branded locations in part of the real estate once occupied by department store retailers.

Other anchors such as ‘food halls’ and similar market places are currently in vogue with mall landlords. Next month, for example, Market & Co. will debut at the Upper Canada Mall in Newmarket, north of Toronto, and others are planned as Oxford Properties and other landlords re-think their mall real estate while seeking to drive traffic to their centres with food and beverage offerings which also includes an expanded assortment of full-sized restaurants.

At one time, much of Canada’s retail sales were done in major department stores. Toronto-based Eaton’s was an important national retailer, as was Simpson’s and Sears (which at one time operated under the same ownership). Regional nameplates such as Woodward’s in Western Canada, Morgan’s in Quebec and others were household names until they either went under or were acquired. Hudson’s Bay ended up buying struggling Woodward’s and Simpson’s and rebranded many of those stores to its Hudson’s Bay nameplate (if locations were kept open at all).

Until late last year, Sears Canada was Canada’s other traditional department store chain. After declaring bankruptcy last year, its last Canadian stores closed in early 2018.

The end of the era of department stores isn’t unique to Canada. The United States was once home to a mighty roster of regional department stores with names such as Marshall Field’s, Dayton’s, The Bon Marché, Burdine’s, Wanamaker, Bullock’s and many others — most of which were eventually converted to Macy’s stores, resulting in considerably fewer locations due to duplicity.

Founded in 1670, the Hudson’s Bay department store chain includes 89 standalone full-line department stores across Canada, as well as an e-commerce site at thebay.com. The company recently opened 10 new Hudson’s Bay-branded stores in the Netherlands, marking the first international expansion for the nameplate. HBC in its totality includes more than 480 stores and about 65,000 employees globally, and also operates banners across North America and Europe including Hudson’s Bay, Lord & Taylor, Saks Fifth Avenue, Saks OFF 5TH, Galeria Kaufhof (the largest department store group in Germany) and Belgium’s only department store group Galeria INNO. HBC has significant investments in real estate joint ventures.

The Hudson’s Bay brand has seen a remarkable transformation over the past several years, which was spearheaded by visionary and retail veteran Bonnie Brooks. She and a team helped take Hudson’s Bay more upscale by dropping hundreds of brands while adding other more popular brands, while renovating stores that were badly in need of updating. As a result, Hudson’s Bay now carries many of the brands that Holt Renfrew once carried (Holt’s itself is undergoing a very high-end transformation) and Hudson’s Bay’s repositioning makes it a competitor of Nordstrom (now with six full-line stores in Canada) and to a lesser degree large-format retailers such as La Maison Simons, which is also expanding.

PHOTO: HBC

1 of 4

Given that the increasingly upscale Hudson’s Bay chain operates 89 stores in Canada, it’s questionable if we’ll see more store closures in the years to come. The Le Boulevard location in Montreal will be closing as mentioned above, and the company is known to have numerous locations which are under-performing.

One Hudson’s Bay store in Western Canada, for example (prior to a mall renovation), saw sales of about $11-million annually — about the same numbers as the Shoppers Drug Mart store in the mall, and about a million dollars less than the much smaller Winners store in the same centre. Moving forward, the company may look to operate fewer and more profitable locations in Canada’s larger centres — some Canadian cities have several Hudson’s Bay stores scattered throughout and there are even Hudson’s Bay locations in smaller centres such as Kamloops in British Columbia, Red Deer in Alberta, and Barrie, Ontario as examples.

There’s still life in the department store concept, however, if done right — Selfridges in London, Galeries Lafayette in Paris and Takashimaya in Tokyo are examples of highly profitable and innovative department stores operating internationally, and elements of their success might be utilized to revive North America’s department stores. That is, if department store owners decide against subleasing space to non-retail uses such as WeWork, which warrants a separate discussion altogether.

We seem to be living in an era in which the pleasure of eating is quite simply overpowered by values-based narratives in food consumption. And this is happening at an astonishing pace. Vegetarianism and veganism are both coming into their own, allowing more people to “come out of the cupboard” to speak openly about and affirm their commitment to a self-imposed diet. They’re doing it for animal welfare, the environment, health — whatever factor is deemed personally important. But make no mistake: this trend is an indication that the current economy is strong.

Human psychology has shown us that consumers traditionally indulge, ironically perhaps, in times of uncertainty. The fear of food insecurity is a very powerful force. Consumers who may lose their professional situation will often treat themselves with sweets and other often unhealthy offerings, just to forget about their own reality for a while.

It appears, though, that healthy eating habits are winning over indulgence these days. Once food security is achieved for a foreseeable future, or even if it is based on pure optics, many things can change. Science serves as a reminder that the food security concept must recognize the importance of food quality in a general sense, which includes considerations of food safety, nutrition and health as well as the experiential aspects of food shopping and consumption. This is likely where we are at in our present economic cycle.

Many years ago, conversations about food were about flavours, tastes and traditions. Today, we talk more about morals and values linked to how we consume food, simply because we can afford to do so. Stock markets are on a tear, and the unemployment rate is almost at an all-time low. Food is not just about survival, but rather more about making a socio-economic statement as much as a moral one. At social gatherings, some are now made to feel as though eating meat is a crime.

In the past, consumers recognised the limitations on their ability to influence the choices made available to them, and they often seemed doubtful about the potential for collective action to work. They made little connection between threats to global food supply and their own daily consumption practices. That has all changed, due to the abundance of time we now have.

Most of our time is spent looking at a screen, a computer, phone, television, or other portable device we have at hand. Technological advances coupled with our pursuit of convenience, have given us a lot more time to think about food in a different way. Grocery shopping and cooking at home takes less time than the pre-industrial practices of hunting or harvesting. With ready-to-eat food, or even ready to cook solutions we save even more time — time now spent on developing a philosophical attitude toward food consumption. Technology makes our lives simple, and with simplicity also comes greater coherent thought and enhanced self-awareness as a consumer and particularly, as a food consumer.

In the meantime, the industry is coping, and adapting quickly. A few stunning examples: McDonald’s is offering Big Macs without the meat, and according to some sources, the Beyond Burger campaign at A&W is having great success. We also have seen changes in packaging and labels to appeal to the increasing number of consumers who are rejecting the status quo, or anything that appears disconnected with a holistic view of the world.

But it all really comes down to how the economy is doing. The current unemployment rate is incredibly low, and according to Morneau Shepell, salaries should be going up by 2.6% on average over the next 12 months. More money in the consumer’s pocket will allow them to believe they can trade up, or perhaps sideways, when making food choices. It also gives families much needed financial help. What is also enticing consumers is a weaker than expected food inflation rate across the country. Food inflation remains more than 1% lower than the general inflation rate. So, prices have been less of an issue this year, although this is about to change.

Grocers are indicating that prices will increase due to tariffs. While the rationale of raising prices due to tariffs is highly disputable, when grocers use financial updates to let consumers know prices may go up, it is a sign. Loblaw and Metro have done it, and it would not be surprising if Sobeys follows suit. Food inflation should reach anywhere from 2% to 2.5% by year’s end.

Yet, even with higher food prices, the buoyant economy allows more of us to think about the ethical, environmental and moral implications of our food choices. And we can afford to — for now.

Dr. Sylvain Charlebois is Dean of the Faculty of Management at Dalhousie University in Halifax. Also at Dalhousie, he is Professor in food distribution and policy in the Faculty of Agriculture. His current research interest lies in the broad area of food distribution, security and safety, and has published four books and many peer-reviewed journal articles in several publications. His research has been featured in a number of newspapers, including The Economist, the New York Times, the Boston Globe, the Wall Street Journal, Foreign Affairs, the Globe & Mail, the National Post and the Toronto Star. Follow him on twitter @scharleb.