BeaverTails location in Grand Bend, ON. Photo: Tourism Sarnia-Lambton

Beavertails, the Canadian pastry chain known for its signature treats at tourist locations, is expanding its retail presence and continuing to open new storefronts while navigating economic pressures and evolving consumer patterns.

Pino Di Ioia, president of Beavertails, said the company’s brick-and-mortar operations are experiencing double-digit growth, driven by a combination of new products and price adjustments amid inflation. “It’s a holistic mix,” he said, noting that last year’s growth continued into 2026, exceeding expectations.

The performance contrasts with the company’s amusement park and mobile truck operations, which have recorded low single-digit growth.

Di Ioia attributed this to the dependency of those segments on discretionary spending.

“If you don’t go to the amusement park, you don’t buy a Beavertail, obviously,” he said. He added that high ticket prices, such as $100 for entry to some attractions, influence consumer behaviour. Mobile units, often used for catering, have also softened due to reduced demand.

Beavertails maintains approximately 164 permanent locations across Canada. The company previously experimented with ghost kitchens and pop-up outlets, which temporarily increased its footprint toward 200 locations. Many of these were phased out post-pandemic due to low volume.

“We got rid of all these other ghost kitchen pop-up stores that were getting us closer to 200. Volume-wise we’re up because those last 30 stores were low volume for us,” Di Ioia explained.

Pino Di Ioia

Looking ahead, the company has several planned openings in the future, including a beach resort in Alberta. Cypress Mountain near Vancouver opened in the past year. The company is looking at a zoo location in Canada. Di Ioia emphasized that Beavertails maintains a selective approach to site selection, focusing on tourist-driven environments that align with the brand’s experiential model.

The company also continues to explore U.S. expansion, though regulatory and tariff considerations make the market uncertain.

“Depending on the day with tariffs, it’s like, ‘Do we want to do it?’ But the U.S. is where we need to be,” Di Ioia said. In Canada, Beavertails has largely completed its presence in major tourist resorts.

Franchising policies at certain sites, including Toronto’s Distillery District and a Montreal-area resort, have limited growth. At Granville Island in Vancouver, municipal restrictions prevent new franchise entries despite the presence of other chains like The Keg and Lee’s Donuts.

Di Ioia said the company anticipates policy changes in the future. “One day the policy will change. We wait,” he said.

Beyond physical stores, Beavertails has developed a grocery retail strategy that emerged during the COVID-19 pandemic. The line includes pancake mixes, ice cream sandwiches, and fresh baked cookies, distributed through major Canadian grocers including Farm Boy, Loblaw, Sobeys, Metro, and Calgary Co-op. The product line now represents a notable portion of overall sales.

Di Ioia described the retail strategy as complementary to the brand’s experiential focus at tourist locations.

“The client loves our brand, but they don’t want to buy us outside of leisure locations. We make the memory, and if we’re not in a tourist environment, the next stop we’ve understood is home,” he said. He added that Beavertails products are increasingly becoming part of celebrations at home, from birthdays to family milestones.

Di Ioia highlighted Beavertails as an indicator of broader consumer trends. He described the company as resilient to economic fluctuations, observing that consumers still purchase its products even when cutting back on other discretionary spending.

“When things are rough economically, you maybe don’t go for a steak, but you’ll still go for a Beavertail. And when things are good economically, you could do both,” he said.

Photo: BeaverTails

This dynamic also reflects K-shaped economic patterns, in which wealthier individuals continue to spend while others limit discretionary purchases. Di Ioia cited anecdotal experiences in tourist hubs like Banff, noting surprisingly high prices for local dining options, which consumers continue to accept.

Beavertails is balancing expansion with operational prudence, seeking to maintain profitability while pursuing new markets and retail channels.

Di Ioia said the company is confident in navigating both Canadian and international growth opportunities.

“We’re amazed at the volume we’re doing with the grocery line, so we’ll keep pushing that,” he said.

As grocery prices continue to rise, a new Canadian app is helping shoppers find where their groceries cost less before they leave home.

Gofer.run compares both everyday and sale prices across grocery stores in a shopper’s neighbourhood and shows where a grocery list costs the least, whether someone shops at one store or chooses to split their trip across multiple stores.

Unlike traditional flyer apps or store-specific tools, gofer.run analyzes each item on a user’s list and calculates the lowest total grocery bill based on the number of stores a shopper is willing to visit, said One Red Maple Inc., which operates the app and is a Canadian start up, focused on helping Canadians feed themselves.

Mark Sherry

Gofer.run is free to download and available on iOS and Android across Canada (currently English only).

“As a serial entrepreneur nearing the end of my career, I’ve always wanted to build something that truly makes a difference, and there’s simply no better feeling than helping Canadians feed themselves,” said Mark Sherry, Co-founder and President.

“In these turbulent times with rising grocery prices, Gofer.run was born out of a passion to provide a vital tool that helps families save money and simplify their grocery planning before they even leave home.”

For example, if ketchup is on a list, the app pulls ketchup products from multiple stores and compares prices by unit, such as per 100 grams or 100 millilitres, allowing shoppers to quickly see which option delivers the best value, explained the company.

Once a grocery list is entered, gofer.run evaluates every item and shows shoppers where their basket costs less. Users can choose to shop entirely at one store and still see savings compared to their usual store, or allow the app to optimize additional savings by visiting multiple stores, it said.

While one individual item may not always be the absolute lowest price on its own, the overall basket is optimized to deliver the lowest total cost based on the number of stores selected, it added.

Key features include:

Price comparison by unit across neighbourhood grocery stores ;

Smart grocery lists that can be shared with household members

Weekly flyer browsing and price-matching lists

Photo search to compare prices while shopping in-store

List digitization that converts handwritten lists into digital ones

Saved grocery lists for recurring shopping trips

Recipe integration that adds ingredients directly to a shopping list

Canadian products highlighted with a maple leaf icon

Operating revenue for the food services and drinking places subsector rose 4.8% to $99.6 billion in 2024, reports Statistics Canada.

This increase was consistent with higher food prices: the food purchased from restaurants component of the Consumer Price Index CPI grew 3.6% in 2024. This was above the all-items CPI, which increased 2.4%. Sales of food and non-alcoholic beverages accounted for 86.5% of total sales, while alcoholic beverages represented 11.0% and other sales made up the remaining 2.5%, it said.

Operating expenses for the food services and drinking places subsector increased 4.3% year over year to $95.5 billion in 2024, resulting in a slightly higher operating profit margin of 4.1%, up from 3.6% in 2023. In 2024, the cost of goods sold remained the largest operating expense, accounting for 35.9% of total expenses. This was followed by salaries, wages, commissions and benefits (33.6%) and rental and leasing costs (8.1%), added the federal agency.

cottonbro studio photo

“Operating revenue at limited-service eating places grew 7.7% to $44.9 billion in 2024, while operating revenue at full-service restaurants increased 1.4% to $44.2 billion,” it noted.

“This marks the first year, apart from 2020 and 2021 during the COVID-19 pandemic, when limited-service establishments generated higher operating revenue than their full-service counterparts. The relative performance of the two industry groups may reflect consumers shifting toward lower-cost, convenience-oriented dining options amid continued price pressures.”

Operating revenue for the special food services industry group—which includes food service contractors, caterers and mobile food services—was up 10.9% year over year to $7.8 billion in 2024. This subsector-leading growth was partly supported by increased return-to-office requirements across both the public and private sectors, explained Statistics Canada.

“By contrast, operating revenue for drinking places edged down 2.6% to $2.7 billion in 2024. Apart from the temporary recovery that accompanied the lifting of pandemic-related restrictions (from 2021 to 2023), the industry has seen a gradual and steady decline for more than 10 years, partly due to shifting consumer preferences regarding alcohol consumption,” it said.

A new survey by the Direct Sellers Association of Canada (DSA Canada) reveals that most Independent Sales Consultants participate on a part-time basis, with 55 per cent working between two and 10 hours per week, underscoring direct selling’s role as a flexible entrepreneurial opportunity that complements traditional employment, caregiving responsibilities, and other pursuits.

The recent Independent Sales Consultant (ISC) Survey found that more than half of ISCs surveyed have been active in direct selling for nine years or longer, demonstrating that participation is often sustained over the long term, challenging perceptions of direct selling as a short-term or transitional activity.

Peter Maddox

“Canadians are increasingly seeking flexible ways to earn income and build skills outside of traditional employment models,” said Peter Maddox, President of DSA Canada. “This research shows that direct selling continues to provide a low-barrier entry point to entrepreneurship, while also offering opportunities for long-term engagement and personal development.”

The survey revealed that women continue to represent the majority of Independent Sales Consultants in Canada, accounting for 89 per cent of respondents, highlighting direct selling as a significant pathway for women’s entrepreneurship and economic participation.

The survey also found that customers are most influenced by product quality and trusted relationships, rather than price alone, reinforcing direct selling’s role as a relationship-driven retail channel. ISCs reported that customer purchasing decisions are also driven by customer service.

“Trust remains at the heart of direct selling,” added Maddox. “In an increasingly digital and impersonal retail environment, Canadians continue to value personalized service and trusted product recommendations.

“These findings show that direct selling gives Canadians, especially women, flexible ways to earn income, build an independent business, and develop skills that support economic participation throughout their lives.”

Brazilian açaí chain OAKBERRY is expanding to Victoria with two locations set to open in early summer 2026.

The global superfood brand will debut its first Victoria storefronts at Tuscany Village Shopping Centre and in Downtown Victoria on Fort Street. These openings mark OAKBERRY’s official arrival on Vancouver Island, with plans to introduce additional locations following the launch of the first two stores, said the company in a news release.

Founded in São Paulo, Brazil in 2016, OAKBERRY said it has grown from a single shop into a global phenomenon, celebrated for its sustainably harvested organic açaí and nutrient-packed superfoods. After its successful Canadian debut in 2023, the brand added it has continued to expand across the country and is now arriving on Vancouver Island.

“OAKBERRY’s menu will offer signature açaí smoothies and bowls made with authentic Brazilian açaí without dyes or artificial preservatives, available in small, medium, and large sizes that guests can create and customize to their liking. Beyond açaí, OAKBERRY also offers a variety of menu options to keep guests fueled all year long, from matcha lattes and grab-and-go morning bowls, to bite-sized snacks including peanut butter bites and protein bars,” it said.

“OAKBERRY smoothies will range from $10.00 to $13.00 and include signature smoothies with functional add-ons, as well as protein smoothies offering up to 32g of protein, whereas bowls will range from $12.50 to $19.50 and offer unlimited toppings, each layered between delicious açai. Toppings range from fresh fruits like bananas, strawberries, and blueberries, as well as granola, chia pudding, cacao nibs, and many more healthy options.”

The two confirmed Victoria locations include a 973-square-foot storefront at Tuscany Village Shopping Centre, and a 959-square-foot location on Fort Street in Downtown Victoria.

The brand has over 900 stores, working within the franchise model and is present in more than 42 countries such as the United States, Brazil, the United Arab Emirates, Saudi Arabia, France, Australia, Peru, Spain, and Portugal.

Today’s Retail Insider articles are listed below along with Canadian Retail News From Around the Web. Highlights include First Capital REIT’s plans to turn Edmonton’s Westmount Shopping Centre into a modern open-air complex. Wayfair has launched its Wayfair Rewards loyalty program in Canada to deepen customer engagement. Meanwhile, Foodtastic is rapidly expanding its Noodlebox brand nationwide with plans for Montreal entry. These developments reflect ongoing shifts toward experiential retail, omnichannel loyalty, and nimble real estate strategies across the Canadian market.

Good Earth Coffeehouse Glenmore Landing (CNW Group/Good Earth Coffeehouse)

Good Earth Coffeehouse is reopening its Glenmore Landing location in Calgary following a renovation.

The newly renovated coffeehouse, at 1600 90th Ave. S.W., offers an updated interior that reflects Good Earth’s warm, down-to-earth atmosphere, said the company.

“A neighbourhood gathering place since 1994, the café is excited to welcome the community back into a refreshed space designed for connection and comfort,” it said.

“Our team has been looking forward to reopening and sharing this beautiful new space with our guests,” said Lesley Yu, owner and operator of Good Earth Coffeehouse Glenmore Landing. “We are proud of how the café looks and feels, and we can’t wait to serve our community again.”

Good Earth Coffeehouse Glenmore Landing (CNW Group/Good Earth Coffeehouse)

“Good Earth Coffeehouse is passionate about creating excellent experiences. The company offers a selection of Rainforest Alliance Certified coffees, roasted exclusively to their specifications. With an extensive menu crafted from fresh ingredients and prepared daily in their kitchens, breakfast, lunch, and evening treats are served with a welcoming attitude that has defined the brand since 1991,” said the company in a news release.

To celebrate the reopening, the Glenmore Landing location will host a Grand Opening event on Saturday, March 21. The celebration will include a ribbon cutting at 11:00 am, food and drink sampling, entertainment, and free brewed coffee all day. The event is open to the public.

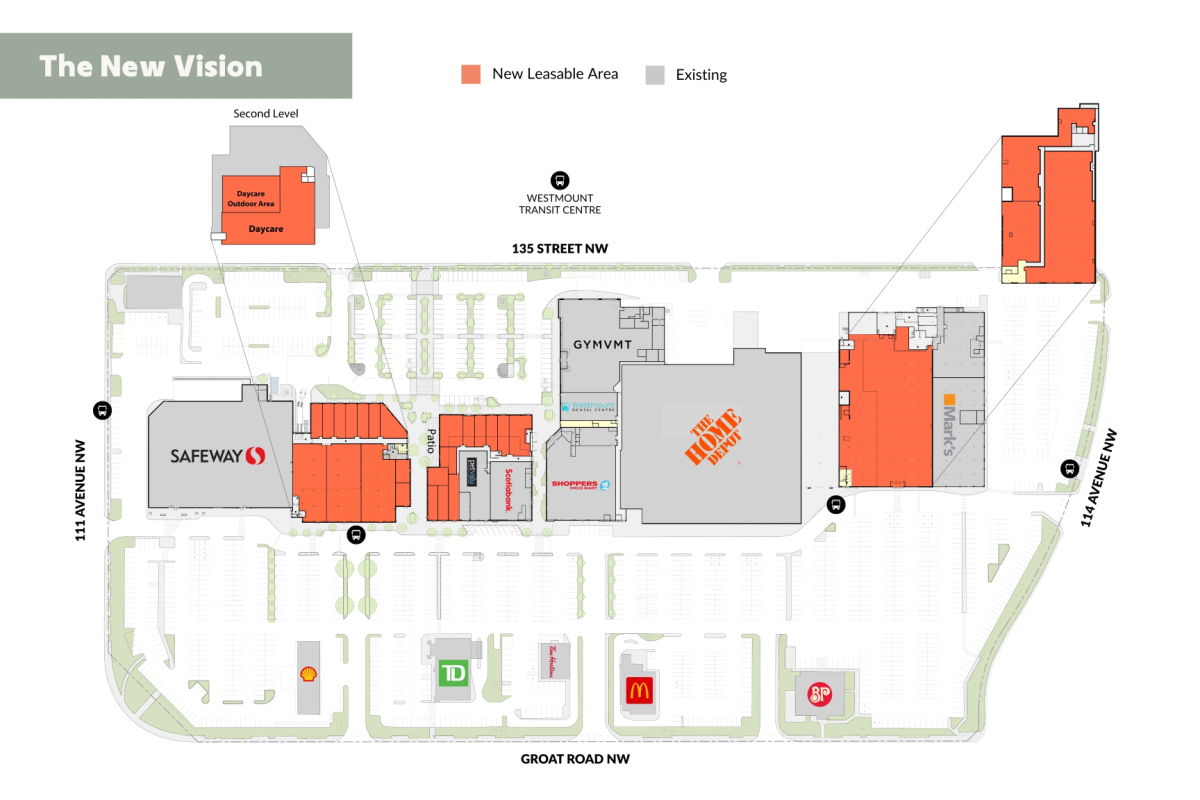

Westmount Centre in Edmonton. Image via First Capital REIT

Edmonton’s first shopping centre is set for a major transformation as its owner unveils plans to reconfigure the aging property into a modern open-air retail complex.

First Capital REIT has announced a significant redevelopment of Westmount Shopping Centre in northwest Edmonton that will remove much of the mall’s enclosed interior and replace it with an outward-facing retail environment. The project will take place over approximately 18 to 24 months and is expected to begin construction shortly following a March 6, 2026 announcement.

The initiative represents the latest example of a broader trend across Canada where older enclosed shopping centres are being repositioned into open-air formats that better align with current retail and community needs.

Westmount Centre in Edmonton redevelopment renderings. Image via First Capital REIT

Transforming an Aging Mall into an Outdoor Retail Environment

At the centre of the Westmount Shopping Centre redevelopment is what First Capital describes as a “flip” of the mall’s layout. The redevelopment will effectively turn the existing inward-facing mall inside out, allowing most retailers to operate with exterior entrances rather than relying on interior corridors.

Large portions of the current enclosed middle of the complex will be demolished and rebuilt as open-air retail space. This includes the section containing the former second-floor movie theatre and surrounding interior areas, as well as much of the existing central block of the mall and the current food court.

In their place, the redevelopment will introduce an open breezeway with new shopfronts that face outward toward the surrounding streets and parking areas. The design will allow shoppers to access stores directly from the outside while maintaining a connected retail environment.

The project will also include new façades, refreshed landscaping, improved pedestrian routes and upgraded entrances that are intended to modernize the appearance of the property.

Parking, Access and Site Improvements Planned

Beyond the structural changes to the retail space, the redevelopment will also include substantial improvements to the broader site.

Plans call for the creation of a new parking area on the west side of the property along with a reconfiguration of existing parking on the east side. Additional pedestrian pathways and public realm upgrades will aim to improve the overall experience for visitors and better connect the site to surrounding community infrastructure.

These changes are designed to support a more convenient and accessible shopping environment while modernizing a property that has undergone numerous renovations over its seven decades of operation.

Westmount Centre in Edmonton redevelopment renderings. Image via First Capital REIT

Construction Timeline and Phasing

The redevelopment is expected to unfold over roughly 18 to 24 months.

Construction is slated to begin shortly after the March 2026 announcement, with building permits already in place. According to Alberta Major Projects, the City of Edmonton issued a building permit for the renovation work in December 2025, enabling the project to move forward.

Importantly, several key tenants are expected to remain open during the construction process. Anchors including Safeway, The Home Depot, Shoppers Drug Mart and Scotiabank are anticipated to continue operating while work progresses in phases across other portions of the property.

Some smaller retailers have already relocated within the centre as part of the preparation for construction. Dollarama, for example, moved to a former Rexall space north of 114 Avenue.

Returning to Westmount’s Original Open-Air Concept

The redevelopment is also framed as a return to the centre’s original design philosophy.

Westmount Shopping Centre first opened in 1955 as Westmount Shoppers’ Park, an outdoor retail complex that predated the enclosed mall format that later became common across North America.

By converting the mall back into a largely open-air environment, the project aims to reintroduce elements of that original concept while adapting it to contemporary retail patterns and transportation access.

The new configuration is expected to support a mix of convenience-focused tenants such as quick-service restaurants and everyday retail that serve nearby residents, students and visitors to the surrounding area.

Location Supports a Community-Focused Retail Hub

Westmount Shopping Centre sits at the intersection of Groat Road and 111 Avenue in the Woodcroft neighbourhood of northwest Edmonton. The approximately 500,000 square foot retail complex occupies a nearly 12-hectare site adjacent to several major community amenities.

These include the Westmount Transit Centre, Ross Sheppard High School, Coronation Park, the Coronation Recreation Centre and TELUS World of Science.

Local officials have highlighted the redevelopment’s potential to strengthen the area as a community node by better connecting retail with transit and surrounding civic infrastructure.

The surrounding neighbourhoods are among the most densely populated areas outside Edmonton’s downtown core, creating strong demand for convenience-oriented retail and services.

Part of a Broader Retail Redevelopment Trend

The Westmount Shopping Centre redevelopment reflects a broader shift in how aging enclosed malls are being repositioned across Canada.

Several Edmonton properties have undergone similar transformations over the years. The former Capilano Mall, for example, was converted into what is now SmartCentres Edmonton East, while Centennial Mall was redeveloped into an open-air retail format in the early 1990s.

Across North America, property owners have increasingly converted underperforming interior malls into outdoor retail environments or mixed-use developments that integrate residential, services and community amenities.

These formats often allow for easier customer access, lower operating costs and greater flexibility in tenant layouts compared with traditional enclosed malls.

Westmount Centre in Edmonton redevelopment North point renderings. Image via First Capital REIT

A Long History in Edmonton Retail

Westmount Shopping Centre has played a significant role in Edmonton’s retail history since its opening more than 70 years ago.

Originally developed by the Woodward’s department store company, the centre opened on August 18, 1955 with approximately 40 stores and about 3,000 parking stalls. At the time, it was widely considered Edmonton’s first modern shopping centre and one of the largest developments of its kind in Canada.

Woodward’s served as the primary anchor tenant alongside retailers such as Johnstone Walker and Kresge. The department store chain also played a major role in shaping the centre’s merchandising strategy, offering a wide range of goods from fashion and home products to groceries through its well-known food floor.

The original configuration allowed customers to enter the mall through the Woodward’s food floor before accessing the main department store.

Westmount Centre in Edmonton redevelopment South point renderings. Image via First Capital REIT

Expansion, Ownership Changes and Anchor Transitions

Over the decades, Westmount Shopping Centre underwent multiple expansions and ownership changes.

In 1966 the centre was enclosed and expanded, with the redesign led by architect Peter Hemingway. The renovation converted the outdoor shopping centre into a fully enclosed mall, reflecting the retail trends of the era.

The property entered a new phase in 1984 when Triple Five Corporation, the developer behind West Edmonton Mall, acquired the site from Woodward’s for approximately $12 million. Triple Five undertook a major renovation and expansion that added roughly 160,000 square feet of space along with a new food court, cinema and dozens of additional retailers.

The Woodward’s store closed in 1993 following the collapse of the chain, and the space was subsequently converted into a Zellers location.

Ownership changed again in the mid-1990s when Triple Five sold the mall to GE Capital Corp and partner Maurice Fagan.

Later Redevelopment and Anchor Changes

Another significant redevelopment took place around 1999 and 2000 when approximately $30 million was invested to introduce a regulation-size ice rink and a new 540-seat food court at the centre of the mall.

Safeway was also relocated as part of the renovation.

In 2007, First Capital Realty, now known as First Capital REIT, acquired Westmount Shopping Centre for approximately $70 million. The company subsequently redeveloped part of the site to accommodate The Home Depot’s first infill location in Edmonton, which opened in 2008.

The former Zellers space later became a Walmart store in 2012 after the discount chain exited Canada. However, Walmart closed the location in October 2022 after relocating to Kingsway Mall.

Vacancy Challenges and the Need for Repositioning

In recent years, the mall has faced rising vacancy levels and declining interior foot traffic.

Observers have increasingly described Westmount as a struggling enclosed mall, with quiet interior corridors and underused spaces, including the former cinema and rink area.

In spring 2024, several tenants reported receiving short-term notices to vacate as redevelopment planning accelerated. Some retailers cited long-standing infrastructure issues such as roof leaks and unused upper-level areas above their units.

Selective demolition work began in portions of the property in 2025 as contractors prepared the site for the next stage of redevelopment.

Strategic Fit for First Capital REIT

For First Capital REIT, the Westmount Shopping Centre redevelopment aligns with a broader strategy focused on repositioning urban retail properties into open-air centres anchored by everyday-needs retailers.

The REIT owns several nearby properties, including Westmount Village and the Brewery District, creating a cluster of retail holdings in the west-central Edmonton market.

The Westmount site’s size, location and proximity to transit make it well-suited to the type of community-focused retail environment that First Capital has been developing across its portfolio.

The One Of A Kind Spring Market Toronto will return to the Enercare Centre at Exhibition Place from April 9 to April 12, bringing together more than 500 Canadian artisans for what organizers say will be the largest spring edition of the event since the pandemic. The four day marketplace will showcase handmade goods across categories including home décor, fashion, art, beauty, food, and wellness.

Since launching in 1975, the One Of A Kind Show has become a prominent platform for Canadian artisans and independent makers. The event connects creators directly with consumers while highlighting the stories and craftsmanship behind handmade products.

New Sections Debut for the 2026 Show

The One Of A Kind Spring Market Toronto will introduce several new sections designed to reflect seasonal themes and evolving consumer interests.

A new Garden Section will highlight plant inspired goods, florals, and products designed to bring nature indoors. The event will also feature a Farmers Market Pop Up that expands the Flavours section with small batch food makers and artisanal treats.

Another addition is a Zero Proof Beverage Section that will spotlight craft non alcoholic drinks.

Organizers say the expanded Flavours area will further showcase Canadian food artisans whose products are designed for everyday meals, hosting, and seasonal gifting.

Photo: One of a Kind Show

Programs Support Emerging Makers

Several returning programs will highlight emerging artisans and community talent.

The Rising Stars section will feature makers with fewer than five years of professional experience, offering visitors an opportunity to discover new designers and handcrafted products early in their careers.

The Marketplace Powered by Interac will showcase artisans participating in their first Spring Market through a tabletop style marketplace format.

Meanwhile, the Small Biz section will again feature Grade 8 students from William’s Parkway Sr. Public School, giving young entrepreneurs an opportunity to showcase their ideas and products.

Event Focuses on Craft, Community, and Discovery

Janice Leung, Show Director, emphasized the show’s focus on connection between artisans and visitors.

“One Of A Kind has always been about more than transactions. It is about connection,” said Leung. “The Spring Market captures the optimism and energy of the season. With over 500 Canadian artisans coming together, this year’s show celebrates creativity in all its forms while giving visitors the opportunity to slow down, explore, and truly engage with the makers shaping Canada’s creative landscape.”

Janice Leung

The event encourages visitors to explore handcrafted products while meeting the people behind them, creating an experience that differs from traditional retail or online shopping.

Event Details

The One Of A Kind Spring Market Toronto will take place at the Enercare Centre, located at 100 Princes’ Boulevard at Exhibition Place.

The event runs from April 9 to April 12, with extended hours on opening day that include a late night shopping event.

Adult admission is $22 online or $24 at the box office. Seniors and students receive discounted pricing, while children aged 12 and under can attend free.

Organizers say the 2026 show reflects renewed momentum within Canada’s craft community while continuing the event’s longstanding role as a gathering place for makers and shoppers.

Foodtastic is accelerating national expansion of its Noodlebox restaurant brand, with dozens of locations in development and plans to enter the Montreal market as the company builds on the chain’s strong presence in Western Canada.

Scott McCannell, Senior VP of Franchising, said the Asian fusion concept has grown to 71 locations across the country, with 14 new restaurants opening in 2025 and another 25 currently in development.

The growth reflects the company’s strategy of building on the brand’s strong western base while gradually expanding into new markets in Central and Eastern Canada.

Scott McCannell

Western roots driving growth

Noodlebox originated in Vancouver and continues to perform strongly in Western Canada, according to McCannell. About half of the brand’s restaurants are located in British Columbia, with Alberta also representing a significant portion of the network.

“It does extremely well out west,” he said.

As the company expands further east, McCannell said maintaining consistent brand awareness and marketing support becomes a key operational focus.

“It’s making sure that we have that kind of marketing halo consistent across the board,” he said.

Expanding geographically also introduces logistical challenges tied to supply chains and regional marketing efforts.

“Going from Montreal to Calgary is a lot harder than going from Montreal to Toronto,” McCannell said, citing differences in supply chain and marketing logistics as the company develops brands beyond their home markets.

Outside Western Canada, Noodlebox currently has a smaller footprint in Saskatchewan, Ontario and Atlantic Canada.

Menu and operating model

The concept focuses on Asian fusion cuisine built around noodle-based dishes, with menu inspiration drawn from flavours such as pad Thai and other Asian spice profiles.

McCannell described the offering as combining traditional Asian dishes with milder menu options intended to broaden the brand’s appeal.

Noodlebox photo

Food preparation is central to the restaurant experience, with meals cooked in visible woks inside the restaurant.

“As you go in and you see the woks, everything’s being cooked fresh in front of you,” McCannell said. “When you’re in there and the woks are going, it’s hot, you can see the flames coming up there. There’s quite the experience.”

He added that the operational model requires experienced kitchen staff capable of managing several active cooking stations simultaneously.

“In order to have four woks going at a time, six in line, 14 sitting down in dining, you really have to know what you’re doing,” McCannell said.

Delivery and takeout strength

The brand’s menu has also translated well to the growing third-party delivery market.

McCannell said Noodlebox meals travel well for off-premise consumption, allowing the company to capture both dine-in and takeout demand.

Large portion sizes also position the concept competitively within its category, according to McCannell, while maintaining consistency between in-restaurant and at-home dining experiences.

“The in-home experience is just as good as the in-restaurant experience, minus the pageantry,” he said.

Noodlebox photo

Real estate strategy

Typical Noodlebox restaurants range from about 1,500 to 2,000 square feet, though the concept has proven adaptable to smaller footprints depending on the market.

“We’ve done one as small as 900,” McCannell said.

Store layouts vary depending on local demand, with some restaurants operating multiple woks to accommodate higher sales volumes.

Average store sales are roughly $700,000 annually, according to McCannell, though some locations generate significantly higher revenue.

“We have some Noodleboxes that are $1.8 million, $1.9 million,” he said, noting that those units generally have larger footprints or expanded back-of-house space.

In terms of location strategy, the brand is flexible about the types of retail sites it occupies.

“Really kind of anything does very well in the urban,” McCannell said. “Noodlebox can play anywhere as long as we have that kind of base square footage.”

The company typically considers both end-cap and inline retail spaces and is not limited to specific formats such as drive-throughs or food courts.

“We’d be willing to look at any and all sites that we feel are fit, first and foremost for market, and then second just in terms of overall demographic,” he said.

Noodlebox photo

Younger customer base

The brand’s primary demographic skews younger, with many customers falling within the 19-to-28 age range.

At the same time, he said the concept attracts a broad customer base without targeting a specific ethnic demographic.

“There is no kind of ethnic gravitational pull,” he said. “It’s open for everybody.”

Montreal expansion ahead

Foodtastic’s next major growth target is Montreal, where the company is headquartered and where McCannell believes the brand could resonate strongly with local consumers.

The company has begun scouting real estate opportunities in the city as it prepares to test the concept in the market.

He described the city as a strong fit for the brand’s culinary positioning.

“Montreal is very cool, very fashion-forward, very culinary-forward,” he said. “We think that Montreal will be a bullseye market for Noodlebox.”

Foodtastic plans to initially open a corporate-operated restaurant to establish the concept locally before expanding through franchising.