In 2012, Vancouver’s Oakridge Centre announced a substantial renovation which would begin with the addition of three new-build anchor stores. In 2014, Vancouver City Council approved the expansion which would see the project double the size of the existing retail square-footage and be rolled out over the course of many years with development finality in 2024. Along the way, there have been advancements and setbacks including the discovery of an underground aquifer in 2016. It was reported in Retail-Insider that the retail expansion of the centre, which is now owned by QuadReal, would be slightly smaller than expected but still dramatic, nonetheless.

Opening day launch of JAC by Jacqueline Conoir in Oakridge Centre

Since 2016 there have been numerous modifications to the original scope of the development, and with any large-scale shake-up there will be hard decisions to make. One retail business that would not be continuing as part of the development was Vancouver-based JAC by Jacqueline Conoir. Over 30 years, founder and lead designer RozeMerie Cuevas built Jacqueline Conoir into an iconic Canadian brand with numerous awards and recognitions in Fashion and Business and had doggedly pursued the development of a brand with a strong identity and continual growth.

In 2012, Cuevas launched JAC by Jacqueline Conoir (“JAC by JC”) to capture the mid-to-upper youth market, away from the ‘business woman’ identity that collections up to that point had cultivated. JAC by JC incorporated relaxed silhouettes, incorporated higher quality fabric, and edginess. Launching a pop-up in July 2016 at Oakridge Centre, Cuevas created a foundation for the new JAC by JC label and brought in higher price-point items including double face coats, down coats, knits, and silk blouses. Two years later, JAC by JC’s pop-up lease was terminated due to the Oakridge expansion plan which saw long-term tenants offered first options on temporary retail spaces.

Bruce Li, RozeMerie Cuevas, Helen Siwak, Vladimiros Xanthopoulos, and President of E-Fashion Town Mr. Leon

To visitors to Oakridge and the public in general, JAC by JC had shuttered and closed permanently, possibly caught up in the wave of closures affecting mid-range retailers due to the rise in fast fashion retailers and the resurgence of upscale luxury brands’ popularity with millennials. In reality, in 2018 Cuevas had already opened 100 retail stores in China with the support of an investor Bruce Li, whom she had met in Vancouver and developed a joint venture partnership within China.

“The Oakridge JAC store was difficult to close as it was performing very well and had attracted many loyal customers who were very sad to hear about the closure. The JAC brand was stronger than it had ever been. We had strong design and a production facility, making it ready for large-scale retail expansion across Canada,” says RozeMerie Cuevas from her office in E-Fashion Town, Hangzhou, China.

Retail-Insider’s west coast correspondent, Helen Siwak, traveled to China to interview Cuevas about JAC by JC’s retail presence in China and the developments that the company is making outside of fashion retail.

The JAC by JC headquarters in Hangzhou’s E-Fashion Town is modern and less than three years old. Measuring 20,000-square-feet over two floors, the lower level houses the design department, administration offices, and a large JAC by JC outlet. The second level includes the sales, customer service, and marketing department, online e-commerce platform, and the sample production room.

E-Fashion Town is a new district dedicated to the business of fashion in China and is traversable by foot or electric carts only. The area is a mix of new builds populated by top Chinese designers, Diction (the Chinese equivalent of WGSN trend forecasting analytics), JAC by Jacqueline Conoir, and an impressive exhibition centre, which Siwak and the JAC by JC team toured with Leon, President of E-Fashion Town. When completed the area will include a massive art and culture centre, additional business buildings, and will hold indoor/outdoor cultural events in the springtime.

Cuevas’ office is on the main floor framed by glass windows. From her position, she can oversee the design and pattern-making division, access the outlet, and hold meetings.

Siwak interviewed Cuevas while shadowing her during the busiest time of the retail cycle, the Spring/Summer 2019 Collection buying event, which saw owners and representatives from 101 stores converge on headquarters for two days of activities.

Presence in China

As of December 1, 2018, there are 101 JAC by JC retail stores in China – the corporation owns 30%, and 70% are franchises. Of these, 50% are owned by businesswomen, 35% by businessmen, and the remaining 15% owned by husband/wife couples.

The locations themselves range in size from 60-square-metres to 300-square-metres, are located in AAA shopping centres, with the company projecting an additional 40 locations by the end of 2019.

At the end of 2018, JAC by JC employed over 550 persons – 100 in headquarters, 150 in corporately owned stores, and 300 in the production facility.

Production in China

With the continuous growth in the number of stores opening and the expansion of the line to 150 styles released four times a year, the company decided that in 2017, JAC by JC would invest in a four-storey production facility. Cuevas asserts that “owning one’s own factory is mandatory to ensure quality production, efficiency, and timely deliveries.”

The completed production facility is unique in that it includes not only garment production space, inventory, and fabric storage, but also includes a large modern restaurant-style eating area, and a communal meeting room where team-building events take place and where the staff and management celebrate birthdays and other special occasions.

To further ensure the well-being of workers, the company built a four-storey residence where individuals can choose to share a studio living space with a friend or occupy a single room. Each room is furnished with ceramic tiling and laminate flooring throughout. When asked if this was the norm for the area, Cuevas responded that it was not, but these were elements that were important to her and her partner to provide for workers, of which many were from outside of the city, to feel comfortable.

In the five years that JAC by JC has been operational in China, the company and RozeMerie Cuevas, in particular, have received multiple acknowledgments, awards, and designations, and is operating and competing with the top Chinese designers. Her status in a foreign country as an icon and a women’s wear visionary continues with an invitation to be on the fashion panel division of the Zhiejing Merchants Associations formed by Jack Ma founder of Alibaba.

Next week Retail-Insider will publish Part II of Retail-Insider on Assignment in Hangzhou, China where we report on JAC by Jacqueline Conoir’s expansion plans for North America and future IPO.

Italian luxury brand Fendi has unveiled its first comprehensive ‘world of Fendi’ leased concession in Canada at Holt Renfrew’s 50 Bloor Street West flagship in Toronto, as Fendi expands its Canadian operations in partnership with Holts.

The boutique, which features nearly 3,000 square feet of selling space, carries the brand’s full line of products for both men and women. That includes a range of ready-to-wear for both genders, as well as an expansive assortment of footwear, leather goods, accessories and women’s furs.

ACCESSORIES AT THE FRONT OF THE STORE. PHOTO: CRAIG PATTERSONPHOTO: CRAIG PATTERSON

The retail space includes luxurious features throughout. Light-coloured textured walls are punctuated by decorative panels of champagne, gold and grey, as well as several fur ‘tablets’ hanging from the walls. Handmade skill carpets in aqua and powder pink contrast with furniture such as modular velvet seating, not to mention whimsical features such as brass and marble occasion tables shaped like large earrings. Furniture and other fixtures were imported from Rome, according to the company.

The store is separated into four ‘rooms’, each carrying different product lines. A separated men’s area, the largest of its kind in Canada for Fendi, includes an assortment of clothing, bags and accessories as well as Fendi men’s footwear (which is the top-selling men’s category for the brand in Canada). A women’s ready-to-wear section includes apparel and furs as well as a seating area and a large dressing room. A women’s shoe salon features a range of styles, and the front of the store includes an expansive assortment of leather goods and small accessories.

PHOTO: CRAIG PATTERSON

On display are some pricier pieces such as a crocodile handbag priced well into the five figures — that particular item is under protective glass. Other bags are open to be touched by shoppers.

The boutique is located in the northwest corner on the ground floor of Holt Renfrew’s Mink Mile flagship. The space previously housed a beauty area and before that, menswear (prior to relocating to a standalone men’s store at 100 Bloor Street West).

Fendi is the second ‘world of’ boutique at Holt Renfrew’s Bloor Street store. In March of 2018, Saint Laurent revealed an equally large concession with its own street-facing entrance at Holts. The store is undergoing an overhaul and more boutiques will be announced shortly. Holt Renfrew is adding ‘world of’ concessions to its Canadian stores, and we’ll discuss this at length in a feature article this month.

PHOTO: CRAIG PATTERSON

PHOTO: CRAIG PATTERSON

Tables shaped like earrings. Photo: Craig Patterson

Looking towards the accessory area from the women’s section. Photo: Craig Patterson

Entrance to the men’s shop. Photo : Craig Patterson

Canadian grocers can no longer afford to wait for their money to show up at their stores. That’s a given. They need to go after it as well. E-commerce in the grocery business was barely a thought 5 years ago. Most grocers did not want to cannibalize sales and decrease foot traffic. The primary idea has always been to have more people in grocery stores, not less. With Amazon, Walmart and Costco looking at cyberspace as a potent place to sell food now, grocers are looking at strategies to keep their customers. At first, it was the “click and collect” era — not the greatest idea in the world, but nonetheless a strategy. Most grocers are now looking at full delivery service whether through a partnership or by developing everything in-house.

That is the case for Loblaw, which recently launched “PC Insiders” which offers free delivery to its customers for a fixed fee. This program “À la Prime” is clearly in response to Amazon’s incursion into the grocery business. The brilliance of the Prime model is based on how it can build loyalty and allow the retailers to cover delivery costs. Paying for delivery is not something consumers are keen to do, and costs could be exorbitant for grocers. With its Prime program, Amazon has perfected the art of covering last-kilometre costs in delivery service, which is known for the most expensive when selling products online to consumers. Venturing into smaller streets, looking for addresses and transporting the product to consumers’ doors takes time and energy. Loblaw with its $99 PC Insiders program is merely copying Amazon by doing the same, and why not? Loblaw has a database of 16 million non-paying PC Optimum members, so a loyalty loop can be executed by Canada’s number one food retailer. Converting 100,000 PC Optimum members can generate enough capital to cover significant costs. It’s the first of its kind in Canada and we expect to see more in Canada in the future.

PHOTO: LOBLAWS WEBSITE

PC Express (Store Pickup) Drive into a reserved PC Express parking spot at your preferred store, and we’ll load your order into your car for you. Photo: Loblaws

PC Express (Self-Serve Kiosks in-store)

Perfect for lighter loads and quick shops. Walk up to our PC Express self-serve kiosks located in-store, find your bags, and go. Photo: Loblaws

PC Express (Neighbourhood Pickup)

Enjoy the same quality service, closer to home. Look for PC Express trucks, containers and other pickup locations in your neighbourhood. Photo: Loblaws

PC Express (GO station [Toronto GTA])

Avoid extra stops on your commute with Station Pickup. Look for PC Express lockers, containers or trucks found conveniently near the parking lot at select Ontario GO stations. Photo: Loblaws

On the other hand, some partnerships look promising as well. Sobeys opted for a partnership with UK-based Ocado. This partnership has done wonders for European grocers willing to increase their business with e-commerce. Many countries in Europe are now seeing online food sales exceed 5%, and in some cases up to 8%. In Canada, we are not even at 2%, but the market potential is real. More than a third of Canadians are thinking of going online regularly to purchase food. Almost everyone under the age of 39 in Canada right now considers the internet as an integral part of their lives. Their economic influence will only increase over time, and grocers know it. Buying online has its perks, especially when the weather is less than convenient, or you want to avoid the flu bug, or that you simply want to grocery shop for someone else who requires care and lives on the other side of town.

The “click and collect” model, the first iteration of the e-commerce play for grocers never made sense from a consumer’s perspective. Ordering online only to pick up your order on your way home is not very convenient. The dreaded step of waiting to pay for your food is avoided when using e-commerce, but “click and collect” only served the industry’s interest in playing defence against Amazon. The e-commerce model is economically more palatable for retailers compared to home delivery as it moves inventory efficiently without the last-kilometer cost. To add insult to injury, some retailers charged consumers for home delivery. More well-thought out online delivery programs will ultimately make “click and collect” obsolete. Mental cyber-benchmarks are different today from those only a few years ago. And, let’s face it, consumers expect more convenience and are willing to pay for it.

PHOTOS AND VIDEO: FRESH STREET MARKET (VANCOUVER)

The emergence of more e-commerce in food retailing signals the end of the big box stores. More retailers are looking at smaller stores which require less inventory and maintenance. A big store with nobody in it is bad for business; therefore, it makes little sense to build more of them. Sobey’s acquisition of Ottawa-based grocer Farm Boy last year in Ontario is consistent with such a strategy. Farm Boy offers a great in-store experience while providing Sobeys with high-quality products to be delivered at consumers’ homes.

E-commerce in food also offers more opportunities beyond retailing. This is happening in service as well. An increasing number of consumers want to “go out by staying home”. No overpriced wine, no extra tips, no standing around waiting to be seated, instead more consumers want to enjoy a meal in the comfort of their homes. Although home delivery by restaurants has been around for decades, there are now new options available to them. New are apps, such as UberEats and Skip The Dishes, allow consumers to have access to more choices. Some restaurants can’t afford a driver or to operate a fleet of cars. These apps act as brokers between restaurants and the curious consumer. As a result, some restaurants are now virtual, operating without a dining room while exclusively selling online. Brokering online relationships between consumers and the food industry could get interesting in years to come. With drones, some are predicting to see more farmers selling directly to consumers. The sky is the limit, literately.

SKIP THE DISHES

UBER EATS

During this Holiday season, malls were packed, but don’t let that fool you for a second. Throughout the year an increasing number of consumers will spend time in front of a screen purchasing presents instead of parking kilometers from the mall’s entrance and working their way though the cashiers. So uncivilized. That rule increasingly applies to food. Now if only we can figure out a way to have someone clean-up the dishes for us, that would be such bliss. That would clearly be e-commerce’s next frontier in food.

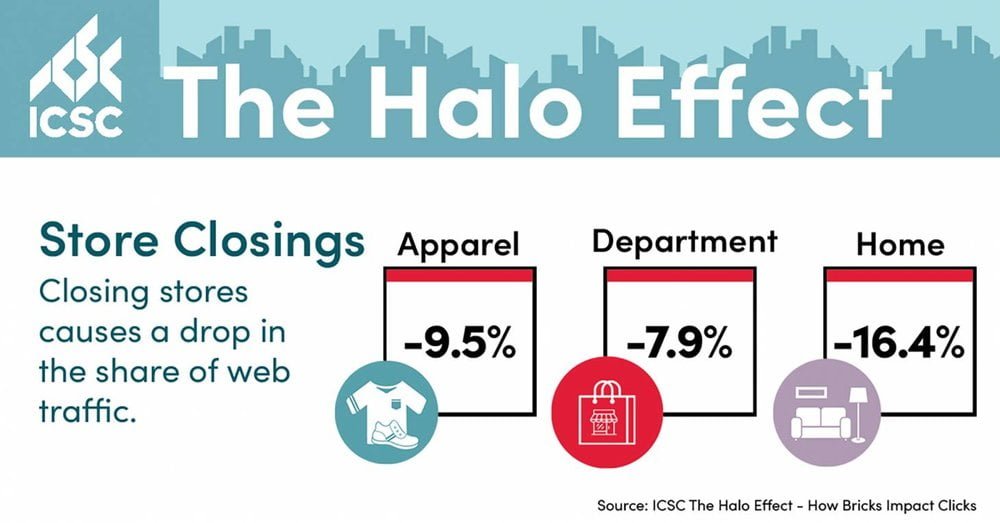

The council’s report, The Halo Effect: How Bricks Impact Clicks, found that opening a new physical store in a market leads to a 37 per cent average increase in overall web traffic. It also found that emerging brands, less than 10 years old, see on average a 32 per cent climb in their share of web traffic when a new store opens. For established brands, it’s a 27 per cent hike.

“A lot has been said over the past few years about the pace at which online shopping is changing buyer behaviours and about the long-term impact on physical retail. There is a direct and positive correlation between having both a physical and a digital presence,” said Michael Kehoe, an Alberta-based retail specialist and broker of Fairfield Commercial Real Estate in Calgary.

“Physical stores are thriving and proving to be vital to the success of both established retailers and emerging brands. In this era of experiential retail, bricks and mortar stores are more relevant than ever. According to the International Council of Shopping Centres, physical retail – bricks and mortar stores – drove 95 per cent of Canadian retail sales – $615 billion in 2017 . . . This study confirms that the blue-chip workhorse of any retail strategy is brick and mortar stores.”

The ICSC survey was conducted by strategy and research firm Alexander Babbage. It tracked retail web traffic and consumer brand awareness among emerging and established brands.

The web traffic analysis included retailers that opened or closed a total of 804 stores, with an estimated 18.6 million square feet of gross leasable area, in 145 markets covering a population of approximately 222 million residents.

“The halo effect is the tendency for an impression created in one area to influence another. In retail, the halo effect is measured through the impact of physical stores on consumers and brand awareness — in ways that can boost or diminish web traffic and online sales,” said the report. “The proof exists at both established retailers and emerging brands that are radically transforming the way they conduct business to compete in this new reality. On one side are traditional retailers that are bolstering their online presence and acquiring e-commerce companies to expand their digital reach. On the other are digitally native brands building a brick-and-mortar presence to sustain growth and customer loyalty. Together, these complementary interests are charting new territory — where physical and digital retail converge to create a seamless experience for shoppers.

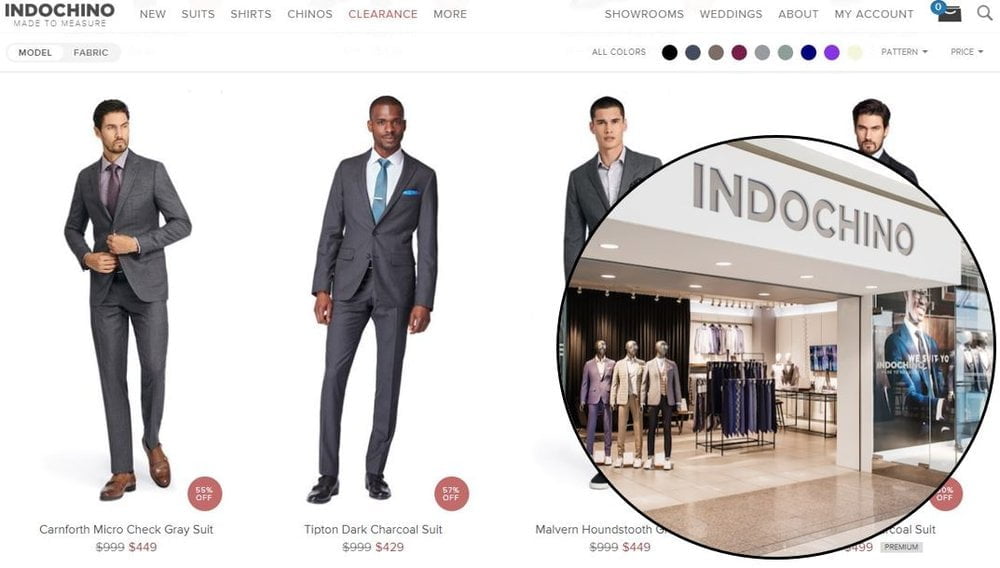

INDOCHINO WEBSITE (CLICK) AND METROTOWN LOCATION (BRICK) IN BURNABY, BC.

“The core of that experience continues to be the retail store and its halo effect on digital engagement and brand awareness.”

The report also said that an increase of just five per cent in the number of physical stores in a single market has a significant benefit on digital engagement and retail web traffic.

And the opposite is also true: Web traffic drops off when retailers close stores. In one retailer’s case, the share of web traffic across the markets where they closed declined up to 77 per cent.

“That new store serves as a constant billboard in the customers’ daily travels, helping reinforce the strength of that brand and the presence of that brand,” said Michael Brown, partner in A.T. Kearney’s consumer products and retail practice, in the report. “It gives the consumer a place to engage with the product and try the product, and it puts a face on the brand.

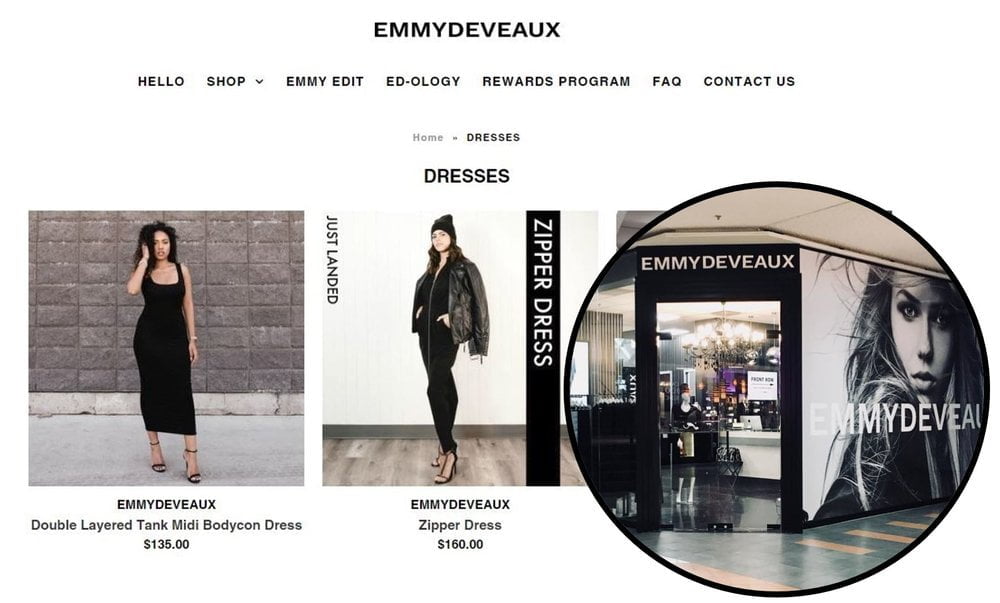

EMMYDEVEAUX WEBSITE (CLICK) AND EDMONTON CITY CENTRE EAST LOCATION (BRICK) IN EDMONTON, AB. THE STORE HAS SINCE MOVED INTO ‘THE BUILDING’ AT 6924 104 STREET AND SOME ARE SAYING IT COULD BE THE ‘NEXT LULULEMON’.

“Do I serve a market area with five stores and my web capabilities, or do I look at having three stores and a fulfillment centre supporting the omni-channel experience in that area? On the flip side, do I want a store that delivers marginal profitability at that location but contributes to the overall profitability of a market because we understand the positive impact of the halo effect? We have to look at the integrated contributions and also understand the negative effects of what happens to the digital business if a retailer closes its only store in a market.”

The ICSC report concluded that a bright future lies ahead for physical retail stores.

“When retailers invest in brick-and-mortar locations, their online presence thrives. What’s more, retailers with physical stores perform better on measures of brand awareness and consumer perceptions than in markets where those brands lack physical locations. As the findings, examples, and insights in this report reveal, physical stores matter, but retailers must continue to innovate in order to flourish in today’s environment,” it said.

I was in New York over the holidays and visited the Amazon 4-Star store in SoHo. Overall, the store was functional but not incredibly exciting from my perspective. The visit also led me to contemplate the limitations of such a concept and to challenge the very meaning of it in society. A little deep for December. Either way, I think the store meets it’s perceived objective: to add value for Amazon customers. The store was packed for at least three reasons in my opinion. Firstly, because it was late December and virtually all popular New York stores were packed. Secondly, because it is relatively new (September 2018 opening) so folks are curious and the Amazon brand is very hip. Thirdly, the store adds value to customers as an extension to Amazon’s tried and true website.

For those of you who are unfamiliar with the concept, let me explain it a little. Amazon has taken select products from it’s US website that have four star and above (five star maximum) aggregate ratings along with new and trending items and top sellers and merchandised them all in one 4,000 square foot physical location.

The store is cashless (a new trend within select retail) and is NOT set up the same as Amazon Go locations that eliminate payment lines. Customers can pay with credit card, debit or the Amazon app.

Each item is electronically signed and shows individual aggregate customer rating details along with the Amazon Prime member price and the non-member price. Electronic signage shows daily featured items.

Overall, I liked the store for it’s simplicity and use of analytics to offer assortments based on what the masses prefer. I wouldn’t say that the store was exciting or offered a unique experience to customers. In fact, I found it a little boring. Having said that, I am not Amazon’s target market for this store. I don’t buy much online, except to learn from a retail perspective. I am also a bit of a minimalist (ironic, I know) and a non conformist (look at my hair).

I also liked how the store uses physical cross merchandising, highlighting products that are traditionally bought together as in the case with the smart home section that showcases all products that work with Alexa in one section. It’s much easier to tell a category story in store than online.

I also like how Amazon highlights specific New York favorites which hints at localization. I think there is an opportunity to do more of this to better address regional variances in customer preference where they arise.

The store succeeds as it reinforces Amazon’s (and society’s) use of collective ratings and reviews to assist one in making a purchase decision. That is, many of us feel more comfortable buying something that other customers have told us is great. Great may refer to quality, functionality or performance among other things. It is important to note that rating systems and specifically Amazon’s rating system has come under scrutiny of late for it’s potential inaccuracy and lack of authenticity. See the link to the article from the Wall Street Journal that talks to this. The store succeeds by adding a physical dimension to eliminate one of the remaining barriers to online shopping: not being able to touch and feel the product. Amazon’s rating system has been used as a proxy for this part of the traditional customer purchase decision making process. When customers shop online they can not touch and feel the product so they rely on others to do so for them and verify their experience with ratings and reviews. These ratings are of course aggregated and averaged.

One can contrast the role of Amazon’s 4-Star store with the trend in retail toward customized, unique and individually marketed products. If customers demand that more products are designed uniquely for them or by them, how does Amazon’s 4-Star’s aggregation and averaging of a given countries’ consumer needs fit in? If I buy a product from this store, I can feel comfortable that millions of other Americans have bought the same item and that it met their needs exceptionally well on average. There is strength in numbers. However, if I wish to express myself and stand out from the crowd with a new shirt or if my tastes vary from the average than perhaps products from this store miss the mark to some degree. Does this mean that Amazon or at least Amazon 4-Star stores are relegated to utilitarian, functional products? More discussion is needed here in my opinion.

Being in an Amazon store, I was not surprised to see customer feedback gathered at the exit with a simple four option kiosk. Simple and effective. More retailers should use this system at least as a starting point. Funny how it included only four options as opposed to five options (stars).

If you would like to see additional pictures and details, CNBC’s analysis is a worthy read.

Several prominent retailers will be closing stores this month in Canada, as the retail landscape shifts and new brands enter the market. The retail industry is complicated — real estate can be costly, and sometimes leases expire without renewal. In January, typically, some companies file for bankruptcy while others reconsider their operations following the busy holiday season, so there may be more to come this month as we expand our reporting.

Hugo Boss ‘Mink Mile’ Canadian Flagship to Close

Staff confirm that on January 20 Canada’s Hugo Boss flagship at 83 Bloor Street West in Toronto will close permanently. The impressive three-level store opened in late 2009 to much fanfare, replacing a women’s store on Cumberland Street in Yorkville.

With 35-foot frontage on the Mink Mile, the retail space spans four floors consisting of a ground floor spanning 3,586 square feet, a second level with 3,541 square feet, a third floor with 3,169 square feet, and a basement level spanning 3,605 square feet (building total: 13,900 square feet). CBRE Toronto’s Urban Retail Team is listing the space for lease.

Hugo Boss will relocate its Canadian flagship to Toronto’s Yorkdale shopping centre this year, where it will open a new 6,600 square foot store in space previously occupied by AllSaints (which recently relocated in the mall). The current Hugo Boss store at Yorkdale, which is located next to a gorgeous new Bottega Veneta flagship and is across from an expanding Holt Renfrew store, has been secured by a luxury brand to be announced at a later date.

PHOTO: WWW.TROVER.COM

J. Crew CF Toronto Eaton Centre to Close

The J. Crew store at CF Toronto Eaton Centre in Toronto will be closing permanently on Sunday, January 6. The 8,315 square foot store boasts a men’s shop with a separate entrance in a prominent location on the third level of the busy shopping centre, which is considered to be CF Toronto Eaton Centre’s ‘most desirable’ level that features soaring ceiling heights under a glass atrium and street front access at its north end (which is anchored by Nordstrom) as well as pedway access south over Queen Street to Hudson’s Bay/Saks Fifth Avenue.

The CF Toronto Eaton Centre J. Crew store opened in the fall of 2012 and was the second in Toronto for the brand, following the opening of a women’s only store at Toronto’s Yorkdale (which was J. Crew’s first Canadian store and the first international location for the US-based retailer).

J. Crew has closed several stores in Canada over the past couple of years. In the fall of 2018 the brand closed two stores — one at CF Rideau Centre in Ottawa and at CF Chinook Centre in Calgary and prior to that, two stores in the GTA (CF Fairview and CF Markville) as well as a unit at West Edmonton Mall. The Edmonton store was J.Crew’s only full-priced store in the city and when the brand opened an outlet store at South Edmonton Common (carrying much of the same product as in the mall), sales at West Edmonton Mall tanked.

J. Crew continues to operate a network of full-priced and outlet stores in the country, though some question if the brand will eventually pull out of Canada entirely. Canadian operations have struggled, though sources confirmed that the CF Toronto Eaton Centre store was profitable. When J. Crew entered the Canadian market in August of 2011 (via Yorkdale), some complained that its pricing was too high compared to its US stores.

PHOTO: ENDA B

Enda B in VancouverShuts Operations

The storied Enda B. retail group, based in Vancouver, shut its operations at the end of December. That included a 4,000 square foot store at 4346 W. 10th Avenue in Vancouver’s prestigious Point Grey area, as well as a 1,560 square foot DKNY-branded store at Vancouver’s soon-to-be overhauled Oakridge Centre.

Enda B. was an upscale multi-brand women’s retailer that was founded in 1983 with a small store in Point Grey Village, which grew to include a larger space on W. 10th Avenue. In 1998 Enda B. opened a DKNY-branded store at 2625 Granville Street, which eventually relocated to the upscale Oakridge Centre on Vancouver’s West Side. Enda B. also operated a DKNY store at West Edmonton Mall which closed a couple of years ago.

The second-generation family-owned business got started back when Vancouver was something of a fashion backwater. A handful of other prestige retailers operated in the city at the time — Alberto’s Boutiques and Shoes operated several stores (in 1987 they were amalgamated to create the multi-brand Leone concept at the Sinclair Centre on West Hastings Street) and Holt Renfrew operated a 50,000 square foot store at CF Pacific Centre. In 1985, luxury multi-brand retailer Boboli opened on the prestigious South Granville strip with luxury multi-brand Bacci’s opening next to it, also housing one of two Canadian locations for Italian brand Byblos.

Fast-forward to today, Vancouver is a luxury retail powerhouse with a 190,000 square foot Holt Renfrew which is said to sell about $400-million annually as well as Nordstrom’s top-selling store, not to mention an ever-expanding assortment of standalone luxury boutiques in the city’s downtown ‘Luxury Zone’. Some mono-brand boutiques are among the top performers globally in Vancouver, buoyed by designer-spending Asian locals and tourists.

DECEMBER DECORATIONS AT BOBOLI. PHOTO: BOBOLI VIA FACEBOOK

Boboli Vancouver to Close Men’s Business

The prestigious multi-brand fashion retailer Boboli at 2776 Granville Street in Vancouver won’t be closing, but it will be losing its connected men’s store that features an iconic arched stone doorway. The men’s store closes mid-January and a new wall will be created to separate the two spaces.

PHOTO: SUQUET INTERIORS

The building with address 2762 Granville Street is being offered for lease by brokerage CBRE Vancouver (Mario Negris and Martin Moriarty have the listing), which is marketing a 2,260 square foot main level as well as a 1,674 square foot second floor. The neoclassical arched street-facing stone entrance doorway contrasts with the stark glass facade — the doorway was originally an upper-floor window moulding on an office building that was salvaged from the 1985 Mexico City earthquake, and hopefully the new tenant is able to retain it.

Boboli will continue to operate a women’s-only store at 2776 Granville Street, which offers fashions from some of the world’s most prestigious designers. At one time, Boboli also housed a Max Mara boutique at 2756 Granville Street on the other side of the 2762 Granville men’s store, which closed in 2013 after a dispute between Boboli’s then co-owners who separated their businesses (the other becoming Vestis Fashion Group). Max Mara now has a standalone flagship nearby which is operated by Vestis.

Cedarbrae Walmart. PHOTO: FIRST CAPITAL REALTY

Walmart Closing Store at Toronto’s Cedarbrae Mall

This month, Walmart is closing its store at the Cedarbrae Mall in Toronto. The shopping centre, owned and operated by First Capital Realty, is located in Scarborough and also features anchors Canadian Tire, No Frills, JYSK and Goodlife Fitness, as well as a range of stores catering to the local community.

It’s uncommon for Walmart to close stores in Canada, though it has a history of exiting malls. Walmart entered the Canadian market in 1994 after acquiring department store chain Woolco, which operated stores in many malls. Over time, Walmart left many of those malls to open (oftentimes larger) standalone locations.

PHOTO: BUILD IT BY DESIGN

Hopscotch Chain in Receivership

Toronto-based healthy fast food business Hopscotch, with locations in Toronto, London ON and Edmonton, has been placed into receivership, according to publication Insolvency Insider. Hopscotch, which is owned by 2576230 Ontario, 2511981 Ontario and 9241922 Canada was placed in receivership on December 19 on application by RBC.

By the spring 2018, Hopscotch was regularly in arrears and as a result, in May, RBC contacted Wyatt Booth (an officer and director of the company) to discuss the financial situation. During the call, Mr. Booth advised that Cara Restaurant Group (now ‘Recipe Unlimited’) had expressed an interest in buying the business. Several months later, Mr. Booth further advised that the restaurant had suffered a severe flood in August, which resulted in substantial damage to its food inventory and equipment. He mentioned that two private investors would be acquiring 5-10% of the company, which would give the restaurant the financial relief required after the August incident, according to Insolvency Insider.

RBC told Mr. Booth that there were important items that RBC required information on, including financial reports. When RBC met with Mr. Booth in September of 2018, however, he was unable to provide requested financial information to RBC such as total sales for each Hopscotch location, monthly expenses and confirmation of rent payments, according to Insolvency Insider. In October of 2018, RBC made formal written demand for repayment of all indebtedness, arguing that Hopscotch has been unable to secure alternative financing or otherwise repay RBC despite ample time being given.

Conclusion: We’ll be analyzing the Canadian retail industry in depth this year as the industry continues to transform. We expect that there will be more closures to announce as headwinds hit some business models — high rents are proving to be detrimental to some retailers, which is resulting in strategy shifts that may include more of a focus on e-commerce as well as pop-up retail. At the same time, it’s important to keep in mind that some retailers are doing very well in Canada, including a mix of national and international brands. This year will see many more international brands enter the Canadian market, though not likely as many as 2017, which was a record-breaker with more than 50 international brands entering Canada by opening stores.

After 10 months of 2018, year-to-date total Canadian retail sales are up 3.3%, according to the latest non-adjusted data from Statistics Canada. This is still slowing however, with retail sales gaining just 2.4% year-over-year for the 3 months ending October 2018. At this pace, annual retail sales growth in 2018 is bound to end up as a recent low point, at less than half the 7.1% gain recorded for 2017. There doesn’t appear to be anything on the horizon to indicate that things are going to improve soon, although recently rising gasoline prices may provide some false optimism.

As the above chart shows, the 3 month trend (orange line) is still tracking below the underlying 12 month trend (green line), which itself has been on a downward slide through almost all of 2018. Volatile gas prices have tended to distort the retail sales picture in recent years. If gasoline station sales are excluded, 2018 year-to-date retail sales growth would be just 2.3%, a full percentage point less.

The above chart also illustrates how steep the 2018 downturn has been when gas prices are taken out of the picture.

Food & Drug

Retail sales growth in the Food & Drug sector may be turning a corner, or at least levelling out after almost a year of mediocre performance. For the 3 months ending October 2018, retail sales were up 2.6% year-over-year. On the other hand, year-to-date sales are up only 1.3% after 10 months of 2018, so the sector still has a long way to go and is likely to end the year at a 5 year low.

The underlying 12 month trend (green line in the above chart) has declined for most of the year. The 3 month trend (orange line) however has perked up in recent months, indicating a potential although modest recovery going into 2019.

Supermarkets & other grocery stores drive this sector, accounting for about half of its retail sales. For the 3 months ending October 2018, their sales were up 2.6% versus a year ago, their best such gain so far in 2018.

Health & personal care stores are the second largest retailer type in this sector, but their retail sales were up only 0.4% in the 3 months ending October, and are still down 0.1% year-to-date in 2018.

Convenience stores, specialty food stores, and beer, wine & liquor stores continue to enjoy above average retail sales gains, but not enough to move the needle much in the overall scheme of things.

Store Merchandise

After a remarkable run up in 2017, retail sales growth in the Store Merchandise sector has come down just as quickly in 2018. For the 3 months ending October, retail sales were up 2.5% year-over-year, the lowest such result in a year and a half. The 3 month trend continues to track below the underlying 12 month trend, indicating more of the same ahead and going into 2019.

There were some poor performances in terms of retail sales gains for the 3 months ending October 2018. Furniture stores were down 1.8% year-over-year, building material & garden equipment/supplies dealers declined 1.3%, and home furnishings stores gained only 0.4%.

Electronics & appliance stores did relatively well, with retail sales up 5.8% for the 3 month period, but this was markedly less than their 9.4% year-to-date gain.

The mixed bag of miscellaneous store retailers however are having high sales gains, up 9.2% year-to-date. Starting in October 2018, cannabis stores have been added to this group, and their sales were $43 million for the month. They will make a greater impact in the miscellaneous retailers category as time goes on, but will remain only a small part of the overall retail sales picture.

Note that Statistics Canada is now suppressing the breakdown of general merchandise stores for confidentiality reasons. The figures in the table below are estimates based on previous trends.

Automotive & Related

The Automotive & Related sector is on the down slope of a wild ride, with retail sales growth cut in half over the last 12 months. Current trends indicate things are likely to get worse before they get better.

New car dealers’ retail sales were up a whopping 9.4% in 2017, but have only gained 0.5% after 10 months of 2018. Rising interest rates are making it more difficult for vehicle manufacturers to offer the most attractive financing packages

Gasoline station retail sales have held up for most of 2018, but even this is softening as pump prices moderate. Due to international economic uncertainty, gasoline prices are likely to remain volatile for some time to come.

By The Numbers

Special Note: Statistics Canada has made updates to 2017 numbers, and has also moved retail storefronts of telecom companies out of electronics & appliance stores and into a non-retail category, Telecommunications (NAICS 513). Retail trade statistics have been revised back to January 2012.

StatsCan started providing ecommerce retail sales data in January 2016. While the amount of data is limited, some trends appear to be emerging. Here are some results.

Overall, e-commerce represented about 2.8% of total Canadian retail sales for the 12 months ending October 2018, including both pure play operators as well as the online operations of brick & mortar stores. Canadian consumers however also buy online from foreign websites which is not captured in these numbers.

Canadian e-commerce sales were up 16.9% year-over-year for the 3 months ending October 2018, but this is less than the 26.5% gain recorded in the same period a year ago. E-commerce retail sales gains are still in double digits, and are still much higher than for location based retail, but growth is slowing down.

Note that location based retail is the same as that in the preceding large “By The Numbers” table. It’s what’s normally reported as Canadian retail sales. Except that it isn’t. Location based retail excludes another section called Non-Store Retailers (NAICS code 454), which includes electronic shopping and mail-order houses, which in turn is where (mostly) pure play e-commerce businesses are. For the 12 months ending October 2018, electronic shopping and mail-order houses had an estimated $10.12 billion in e-commerce sales.

But that’s not the only source of e-commerce, as (mostly) bricks & mortar location-based retailers also sell online. For the 12 months ending October 2018, this group had an estimated $7.39 billion in e-commerce sales. With electronic shopping and mail-order houses, there’s a grand total of $17.50 billion in e-commerce sales by Canadian operators over the year. Note that this does not include foreign e-commerce purchases made by Canadian consumers, but it does include e-commerce purchases made by foreigners at Canadian businesses.

For electronic shopping and mail-order houses, an estimated 83.4% of their sales are allocated to e-commerce. For (mostly) bricks & mortar retailers, it can be estimated that just 1.2% of their total sales come from e-commerce.

In the final section of the above table, (mostly) pure play operators (namely, under electronic shopping and mail-order houses) generated an estimated 57.8% of all e-commerce sales in Canada, while (mostly) bricks & mortar location-based retailers’ share of e-commerce is 42.2%.

We’re providing some updates to our top 10 most-read articles in Retail Insider in 2018, and what a year it was. Sears Canada closed its remaining Canadian stores, several retail chains exited the market (and in some instance their entire operations), and dozens of new international retailers entered Canada (this month we’ll provide an updated list on brands that entered the country in 2018, as well as a 2019 forecast for the industry).

Given that some of our own exclusive reporting differs from larger mainstream news publications, our most-read articles are rather unique. We endeavour to break stories first where we can, and we sometimes defer major story reporting to other publications through our daily Canadian Retail News from Around the Web where we aggregate articles from other news sources on a summary page.

Below is a list of our top 10 most-read exclusive news stories of 2018, and with that we’re also providing some updates on these as we push forward into 2019. Our story on the possible bankruptcy of Miniso Canada, for example, has some updates after some current and former staff reached out to us with new and in some cases concerning information.

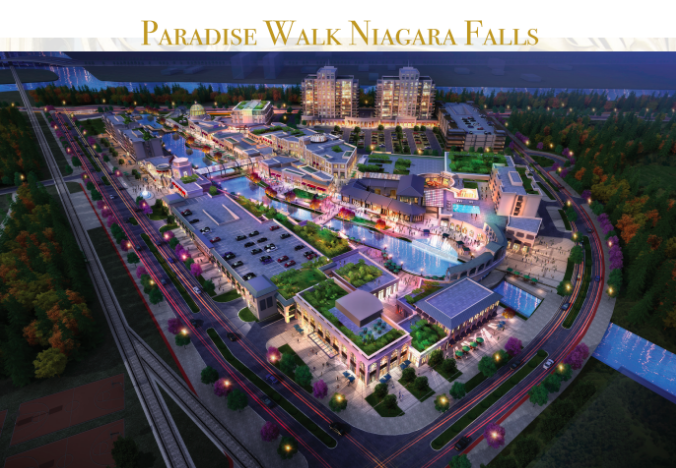

The experience-based commercial area would feature a series of outdoor pedestrian streets with zones dedicated to different tenant types. Included will be several attractive public spaces with central areas that will house attractions such as street performers and a rideable carousel. About 50% of the commercial mix would be for food and beverage offerings, reflecting a similar mix seen in commercial centres in major markets globally.

One of the reasons the article got so many readers is that the proposal is controversial, with some locals standing up against a development that would see significant modifications to a natural habitat. As a result, it’s unclear whether or not the development will ultimately be approved, though in May of 2018 the local government gave it the green light to move forward — we’ll be watching this story and will provide updates.

9:Jollibee Discusses Canadian Expansion Plans: Popular Filipino restaurant chain Jolliebee is expanding its operations in Canada, with plans for about 100 locations. The company entered Canada in November of 2017 via Winnipeg, and it has since expanded into the GTA, where openings saw substantial lineups.

Jolliebee provides the Filipino community “a chance to experience the Philippines again”, as quoted by journalist Mario Toneguzzi in the article which ran in Retail Insider in January of 2018. In June, Mr. Toneguzzi followed up this story with the revelation that Jolliebee is planning a sweeping expansion of its business. Jose Minana, Jollibee Foods Corporation’s North American Group President, told Retail Insider that the company’s massive expansion plans in Canada are “realistic.”

“It’s a matter of having the ability to ramp this up and as we look at our organization and our capabilities, 100 stores would be something that’s very realistic for us to do,” he said.

The 137,000 square foot Sears box will see some changes, according to Regional Property and Leasing Manager Marcel Elliott. “We’re chopping off about 60,000 square feet on the end and creating more parking and then we will be build out in front of it. We’re subdividing space and adding new space to create smaller units and mid-size to big-box units,” said Elliott.

About 36 new tenants will be added and remarkably, despite challenges to the economy and industry, the centre has had a zero vacancy rate for the last decade. Elliott said, “adding 36 sounds like a lot but we’ve got a waiting list”.

7:Will ALDI and Lidl Enter Canada and Disrupt the Grocery Industry? In January, Grocery Business submitted an article by Michael Marinangeli with a discussion on whether or not German discount grocers Aldi and Lidl would enter the Canadian market. Either of them would disrupt Canadian grocery retailing, which is already hyper-competitive and with relatively low profit margins. Both German retailers are known for their low prices and efficient operations, and both have been expanding into the United States (Aldi also owns US chain Trader Joe’s, which would be a great addition to Canada as well).

The article notes that Lidl has been opening stores rapidly in the United States and Aldi, with 1,600 stores in the US, is spending $1.6-billion to expand/remodel 1,200 of them, while opening an additional 400 stores. Between 2003 and 2013, Lidl and Aldi have grown to 20,000 stores in Europe from 8,000 — in Germany, the two have about 50% market share.

We don’t have any concrete information as to whether or not either will be opening in Canada in the near future, though some in the industry have been predicting it for some time. Loblaw’s Galen Weston told the Globe & Mail in April of 2017, “from a planning perspective, our expectation is that at some stage they will come to Canada. I always say in three years, but I’ve been saying three years for a while.”

If anyone has further information as to if either Aldi or Lidl will enter Canada, please email me: craig@retail-insider.com.

Other luxury brands in the new wing include Montblanc, Saint Laurent, Prada, Max Mara, Jimmy Choo, and Armani, among others. The centre is also home to the first Aritzia outlet, which is said to already be a hit.

Interestingly, Toronto’s luxury gain was Montreal’s loss. Recently, Gucci and Max Mara exited the Premium Outlets Montreal after opening in Toronto Premium Outlets — both malls are owned in partnership by Simon and SmartCentres.

5: 2018 Canadian Retail Forecast: In January of 2018 we put together our annual forecast of what we expected in Canadian retail for the year. We predicted a robust year of store openings, which was certainly the case — this month we’ll reveal a list of international brands that entered Canada by opening stores, as well as our 2019 forecast of what is ahead.

You can read your 2018 forecast here, which provides an overview that discusses international retailers, shopping centres, luxury brand expansion, off-price retail, ‘grocery wars’, cannabis retail, and the rapid growth of e-commerce (which Amazon continues to dominate). We also discussed the possibility of bankruptcies and store closures, some of which unfortunately came to fruition last year.

Photo: Endy

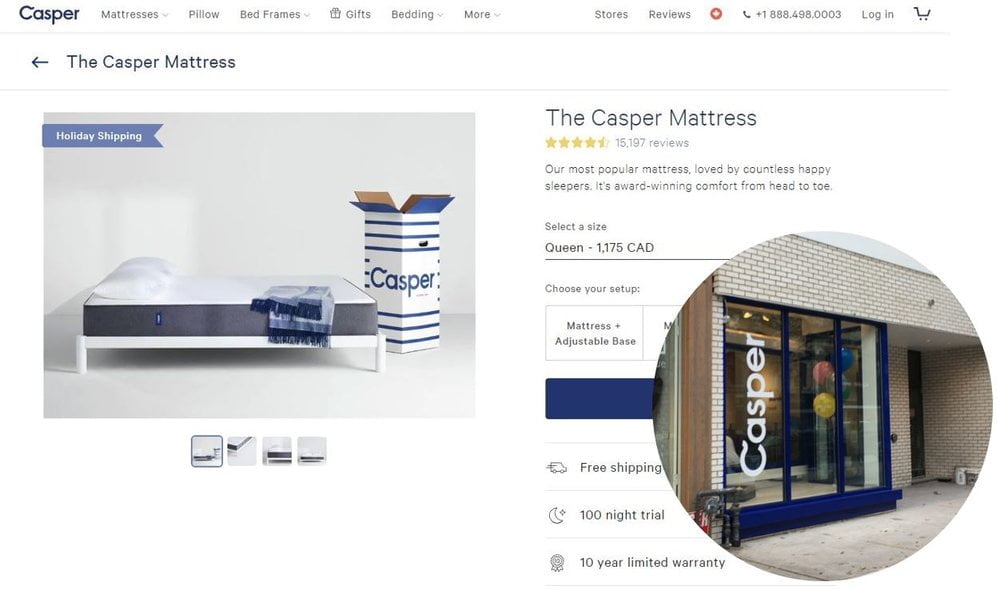

4: Canadian Mattress-in-a-Box Brand ‘Endy’ Announces Expansion Amid Explosive Success: Competition has never been fiercer for ‘mattress-in-a-box’ retailers — the concept has been around for only a few years and it is already disrupting the bedding industry globally. Endy says that it is the top-selling mattress of its kind in Canada, surpassing competitors such as Casper. Endy’s growth is rapid, boasting 300% year-over-year gains, not to mention a lot of five-star ratings from purchasers.

Endy recently opened a Western Canadian distribution centre near Vancouver to keep up with the demand. When we reported on Endy in June, CEO Mike Gettis said that a standalone store expansion could be in the works — that follows on the heels of Casper, which last month opened its second standalone Canadian store.

Canada’s biggest bedding retailer, Sleep Country Canada, acquired Endy for about $89-million in November. While both will operate independently, it’s likely at some point that we’ll be seeing some sort of brand partnerships, given the success and growth plans for both retailers.

PHoto: Craig Patterson

3: Nordstrom Announces First 3 Canadian Nordstrom Rack Opening Dates: In September of 2017 we announced the opening dates of Canada’s first three Nordstrom Rack stores, and it appears that thousands were interested in reading about the news. Although the story wasn’t published in 2018, search engine optimization led to the massively high readership last year.

Nordstrom Rack currently operates six stores in Canada, and more are said to be on the way. While not confirmed by Nordstrom, marketing materials for the Lougheed Town Centre in suburban Vancouver indicate that Nordstrom Rack could be a future tenant at the overhauled mixed-use centre.

Miniso Canada issued a statement on social media claiming that it had reached a ‘preliminary agreement’ and that things would be ok. We followed up repeatedly with the company and never got a response.

Several former (and current) employees have since reached out to us with their stories about Miniso, which are concerning. One individual, who recently left the company, explained how stress in the workplace had caused them to start taking sleeping pills and anti-depressants. Some are said to have sleeping bags in a warehouse because of long hours, and the rapid pace of store openings has been taxing on everyone involved.

Another concern is the lack of proper French-language labelling and signage in Quebec. Miniso Canada has been put on notice by the Office québécois de la langue française, or the ‘Language Police’ as some call them. If the issue isn’t properly addressed, Miniso Canada could be required to forfeit its revenue in the province from the time that the first store opened there. Quebec became one of the fastest-growing markets for Miniso globally, which means it could be fined millions of dollars. That’s especially concerning, considering that there are also multiple lawsuits from contractors who claim that they are owed money for building Miniso’s stores.

The centre was first announced in December of 2013, followed by an announcement that the centre would be larger than anticipated at about 428,000 square feet. The centre cost about $215-million to build and is unique in that it is an enclosed outlet centre — In Canada, most are open to the elements.

We speculate that one of the reasons the article was so widely read was, due in part, to some disappointment over the tenant mix, which was initially rather unremarkable. New tenants have since been added, though the Edmonton centre lacks the brand offering of centres such as Toronto Premium Outlets.

Conclusion: This month we’ll be revealing a list of brands that entered Canada by opening stores, as well as our 2019 industry outlook. We’ll also be diving deeper into editorial topics in 2019 as we grow in strategy as a publication. Happy New Year.

Craig Patterson, now based in Toronto, is the founder and Editor-in-Chief Retail Insider. He’s also a retail and real estate consultant, retail tour guide and public speaker.

A cannabis retailer has leased space on Canada’s most prestigious street-front retail strip, Bloor Street West in Toronto, and another is set to open nearby in Yorkville. Neither is open yet and it’s not yet clear how they will operate, given that only 25 cannabis licenses will be granted by the Ontario government in April of this year.

Signage for Fire & Flower went up at 95 Bloor Street West at the end of December in a retail space flanked by MCM to the east and Victorianox to the west. Several prominent luxury retailers are located nearby. The 3,600 square foot retail space (2,100 sq ft ground floor, 1,600 sq ft upstairs), which now features a video wall on its second level facing towards Bloor Street, was most recently occupied by menswear retailer Strellson and prior to that, Town Shoes. The building was listed for lease by CBRE Toronto’s Urban Retail Team.

In many respects, cannabis retail in Yorkville makes sense. The affluent high-density area is growing quickly, including a mix of new younger residents as well as seniors downsizing from larger homes in areas such as Rosedale and Forest Hill. Cannabis use is proving to be more common than many expected, and an informal poll amongst residents in the neighbourhood last week indicated that some will be shopping locally, be it for recreation or for medicinal uses.

SLIDESHOW (swipe for more)

Photo: Fire & Flower Facebook

Photo: Fire & Flower Facebook

Photo: Fire & Flower Facebook

Photo: Fire & Flower Facebook

Photo: Fire & Flower Facebook

SLIDESHOW (swipe for more)

Photo: Fire & Flower Facebook

Photo: Fire & Flower Facebook

The Ontario government announced last month that only 25 legal cannabis dispensaries would be opening in Ontario in April via a lottery system, with lack of supply being the main reason for the limited rollout. More licenses will be granted as the cannabis supply chain sorts itself out — pot has been selling out in retailers nationally after legalization in October of 2018. There’s no word yet if either Yorkville retailer will be able to distribute cannabis products in April, though some brands are also securing spaces for educational purposes.

Many landlords we’ve recently spoken with have said that lately, cannabis-related retailers have been the most aggressive in bidding for street-front locations in cities such as Toronto. That’s good news at a time when in some areas, leasing space has proven to be a challenge as some retailers re-evaluate their brick-and-mortar strategy in Canada. Some streets have seen a downward trend in foot traffic — and if Ste-Catherine Street in Montreal is any indication, cannabis retailers could help add foot traffic to neighbourhoods as consumers line up to make purchases. Hopefully the same shoppers will have enough money left over for Louis Vuitton, Prada and Dior, the latter of which will open its largest store in North America at 131 Bloor Street West later this year.

Craig Patterson, now based in Toronto, is the founder and Editor-in-Chief Retail Insider. He’s also a retail and real estate consultant, retail tour guide and public speaker.

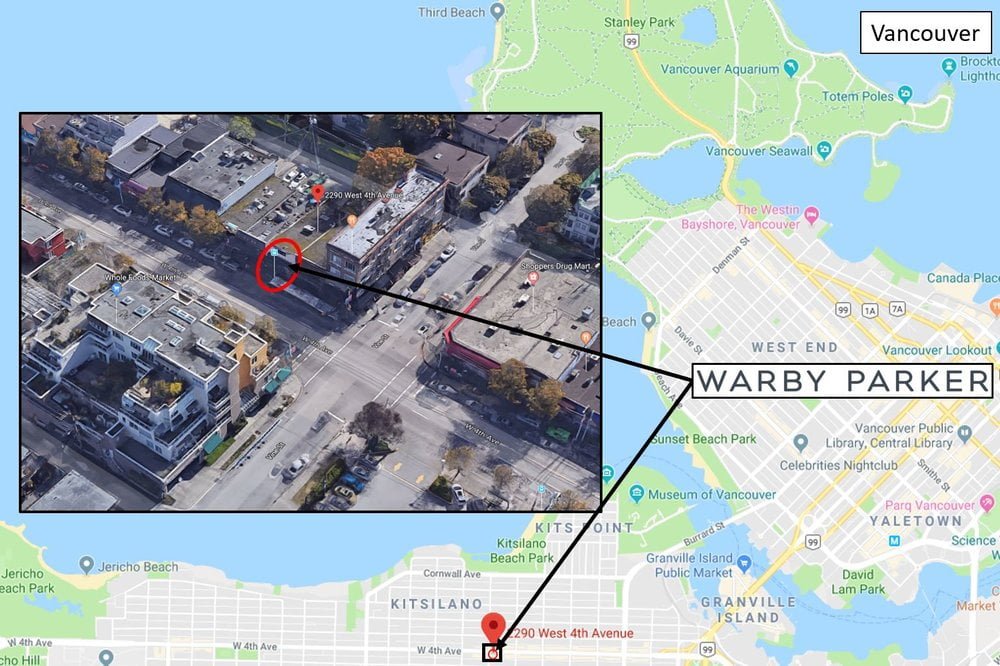

Innovative New York City-based, value-priced prescription eyewear retailer Warby Parker has secured a location for its first location in Vancouver, which it intends to open in early 2019 in the city’s trendy Kitsilano area. More locations will follow as the retailer ramps up its Canadian store expansion.

The Kitsilano Warby Parker will be located at 2290 West 4th Avenue in a space that is nearly 1,800 square feet on one level. The trendy area is home to some unique independent and chain retailers, and Warby Parker will be directly across the street from a Whole Foods grocery store.

The store’s design, according to Warby Parker co-founder and co-CEO Dave Gilboa, will be reminiscent of a library. Mr. Gilboa said that the reason West 4th Avenue was chosen is because Warby Parker “loved the feel of Kits, and the building could lend itself to a unique design”.

As with other Warby Parker store openings, the Vancouver location will feature a unique art and design component, as well as an exclusive product offer for the city. The company will reveal further details in January.

In some ways, the Kitsilano location is similar to where Warby Parker opened its first Canadian store in Toronto in August of 2016. Located at 684 Queen Street West, the 1084 square foot Warby Parker store is at the centre of a trendy area which Vogue Magazine named as being the ‘second-coolest’ in the world in 2014.

Warby Parker opened its second Canadian store at Toronto’s Yorkdale Shopping Centre in December of 2016. That store, as well as the Queen Street store, feature something of a ‘library theme’ with books on display, some of which are also for sale.

Warby Parker has been growing rapidly in the United States. When Warby Parker opened its Toronto store in the summer of 2016, we reported that the brand had 30 stores in the United States. As of now, Warby Parker operates 86 stores in the United States as well as the two Toronto locations.

Mr. Gilboa said that Warby Parker is looking to operate about 100 locations in the United States, as well as several in Canada. He said specifically that the Vancouver market will see more than one location, though no other leases have been signed in Canada.

Warby Parker was founded in 2010 as a pure play online retailer with a $2,500 seed investment by students in the Venture Initiation Program of the Wharton School of the University of Pennsylvania in Philadelphia. Shortly after its launch, the company was featured on Vogue.com, and GQ, referred to as ‘the Netflix of eyewear’. The company has grown substantially and now boasts 30 brick-and-mortar stores in the United States. Last year, the company was reportedly valued at US $1.2 billion. Warby Parker designs its glasses in-house and sells directly to customers — prices are therefore generally lower than regular optical stores, which may mark up product substantially.