Walmart Canada announced a $53 million investment to increase wages for approximately 40,000 hourly store associates while also making investments in technology. This initiative aims to boost employee compensation, attract talent in competitive markets, and acknowledge the hard work of its associates.

AnnMarie Mercer, Walmart Canada’s Chief People Officer, highlighted the company’s dedication to its employees, stating, “We are committed to investing in our people and making Walmart Canada a great place to work.” This pay raise represents Walmart’s effort to recognize the critical role of store associates in the company’s success and ongoing growth.

In addition to wage increases, Walmart Canada is investing in advanced technology to further modernize its operations. The introduction of new digital handheld devices for employees is expected to improve customer service and operational efficiency. Joe Schrauder, Chief Operating Officer at Walmart Canada, emphasized the importance of this technological upgrade, saying, “Providing our associates with the right tools is essential to meeting the evolving needs of our customers.”

These digital devices will enable employees to access real-time information, manage inventory more effectively, and streamline various in-store processes. By enhancing the technological infrastructure, Walmart Canada aims to create a more seamless and efficient shopping experience for its customers.

Walmart Canada’s comprehensive strategy includes not only competitive wages but also a range of benefits and development opportunities for its employees. The company offers incentive bonuses, health benefits, and career advancement programs, including full tuition coverage through its Live Better U program. These initiatives are designed to support the professional and personal growth of Walmart associates.

Mercer reiterated the company’s focus on employee development, adding, “Our associates are the heart of our business, and we are dedicated to providing them with opportunities to grow and succeed.” This holistic approach to employee welfare underscores Walmart Canada’s commitment to being a top employer in the retail sector.

With over 400 stores nationwide and a robust online presence, Walmart Canada continues to be a dominant player in the Canadian retail market. The company’s efforts to invest in its workforce and embrace new technologies reflect a broader strategy to maintain its leadership position in the industry. The company has announced in recent years billions of dollars of investments in the Canadian market, including updating and expanding physical stores, its online business, as well as its expansive logistical operations.

Anatomy of a Leader: Wendy Derzal Minnett, VP of TacoTime Canada and Extreme Pita Canada

A passion for the hospitality industry has always been an important part of Wendy Derzai Minnett’s life.

The VP of TacoTime Canada and Extreme Pita Canada with the MTY Food Group can trace her career in the hospitality industry back several years ago when she had a burning desire to see Bruce Springsteen in concert in Toronto.

Wendy was born in Montreal but her formative years were spent in Geneva, Switzerland as her father had diplomatic status working with the International Telecommunications Union. The family lived there for most of her younger years.

The family came back to Canada by the time she was in Grade 8 to Manotick, Ontario, just outside of Ottawa.

“I had to learn to read and write in English,” says Wendy.

Earlier years in hospitality – photo supplied

She initially took Arts at Carleton University and then went to the University of Toronto to do a degree in environmental science.

“That’s sort of where my career started. I worked at Skydome actually when I got hired by Manpower when they were just building because I really wanted to see Bruce Springsteen and obviously had no money to do that,” says Wendy.

“A friend of mine was getting a job as an usher and I thought ‘Oh my God that’s a great idea, I’m going to do that too’. So I got a job as an usher and of course I never got to see the show because I was too busy working. So that really didn’t work out very well but it started a great path for me.

“I was an usher. I was there eight years and I got promoted all the way through. I was in guest services, I got promoted to the head of guest services, I was the EA for one of the VP’s at Skydome and then ended up running the corporate suites. And in doing that, I met all the predominant Torontonians who worked in financial and big companies which led me to start my own event marketing company. And it was easy. I was lucky because I made so many great contacts.”

Prior to joining MTY, Wendy was with Gateway Casinos and Entertainment Limited as Director of Brand Marketing and Director of Food and Beverage Marketing.

Her professional career also included positions as Director of Marketing, Sales and Business Development with the Donnelly Group and Director of Marketing and Sales with Points West Hospitality Group.

Wendy also has a Diplome de cuisine from Le Cordon Bleu in Paris, France.

Taco Time trade show event, photo supplied

She spent five years in the casino industry prior to joining MTY.

“It was an exciting five-year venture in the casino business. I was able to build and develop four unique casino brands and four unique food and beverage brands that we sort of replicated in each of the casinos. It was really fun because it was a highly competitive and dynamic environment. It demanded a lot of creativity and innovation and each brand needs to stand alone in a market saturated with entertainment options,” explains Wendy.

“It really actually helped me hone in on my marketing skills, customer service, customer experience, attracting patrons. It really enforced the need for loyalty and that’s a huge thing in casinos but it really translated well into what I do now because it’s all about loyalty. Back then you didn’t have loyalty programs, it was really important to define that brand differentiation, customer loyalty program, high stakes project management. They were all crucial and critical things to learn before I got into QSR (quick service restaurant).”

When she first went to university, Wendy says she wanted to be an environmental lawyer.

“But that didn’t work out very well because the only problem with that is . . . at that time, it was 1992, certainly environmental science and the love of the environment is not where it is today, so back then I would have to be on the side of government and if I was going to be on the side of government versus the people that are polluting I wouldn’t have made any money and I would have starved to death, so that wasn’t going to be a good plan for me,” she laughs.

Working at Skydome led her into another field.

“My mom always said that you’ll fall into something that you love and it just became something that I loved. I loved hospitality. I loved cooking. I have the personality I guess as I’m always good with sales, so sales and marketing kind of came together and the great part of this part of my life is once I left Gateway and Mr. Dave Minnett (CEO of Edo Japan and now her spouse) sort of determined that it was a good idea for me to come to Calgary, doing that here brought the culmination of all that QSR experience,” says Wendy.

“I really love the whole idea of building a brand identity. Customer experience is paramount for me for anything that I’ve ever done. This has all kind of enabled me to innovate continuously, ensuring our QSR brands are not just met but exceeded by customer expectations in today’s competitive market.

“What I love about this job is that it’s sort of a culmination of everything that I’ve ever done and it’s brought into one place. And I feel all the experience I’ve had led me to where I am today. It’s been a 30-year journey.”

Image: Wendy Derzal Minnett

Wendy says she’s worked with great people and some not-so great people in her career.

“I sort of promised myself if I was ever put in a position of having people, leading a team, I would make it inclusive, non-dictatorial. I always say to my team this is not a dictatorship. Your opinion matters. We have to make these decisions together,” she says.

“I’m a very empathetic person. I like people to enjoy what they do. It’s a hard job. We have to do it every day. I want them to come and have a good time, enjoy themselves, and still enjoy their job with support. I believe every person has great abilities to do their job but I think you can do your job a lot better when you’re actually given a pat on the back and told what a great job you’re doing. I really wanted to build loyalty in my team.

“We are a team. I’ve always said the only time that I am the boss is when stuff’s rolling down the hill and then I’m there to protect you from it. That’s my role. Otherwise we do everything together. We collaborate. We do it together. I learned all the things not to do from previous people . . . I really wanted to be a mentor and I’ve had some great people in my career who have actually helped me get to that next level. So I wanted to do that for every member of my team.”

Wendy enjoys golfing in her spare time as well as traveling and culinary experiences.

“Calgary has just been a joy I have to tell you. Going from Vancouver to Calgary I was really concerned. I had a great space in Vancouver. 180 degree view with the mountains and the ocean. But honestly in Calgary the hospitality gene in this city is by far the best I’ve experienced in any city I’ve ever lived in,” she says.

“Our level of culinary expertise and cocktail culture here for a city of its size is staggering to me. There’s always something new and amazing to experience. It’s really been a joy.”

Craig and Dustin Fuhs, Editor-in-Chief at Retail Insider, discuss nearly four years of retail industry evolution during Fuhs’ tenure with the publication. They reflect on the significant impacts of the COVID-19 pandemic, which brought about numerous challenges such as lockdowns, bankruptcies, and rapid adaptations within the retail sector. Fuhs shares insights into how Retail Insider managed to navigate through these turbulent times by staying flexible and responsive to the changing needs of their readership.

Throughout the conversation, Fuhs highlights several memorable stories and milestones, including the closures of major retailers including the Disney Store, Nordstrom, and Target. He recounts the secretive and strategic nature of their work, from holding exclusive news about IKEA’s downtown Toronto store to the expansion of Indochino under Drew Green’s direction. The discussion also covers the rise of experiential retail, with examples like Tesla and Apple stores, and Fuhs’ passion for immersive retail experiences.

As Fuhs prepares to step down from his role, he reveals his future plans, including the launch of his new venture, The Immersive Lab, which focuses on creating unique retail and experiential environments. He expresses his gratitude for the relationships and experiences gained during his time at Retail Insider and looks forward to continuing to contribute to the industry in new ways. Patterson and Fuhs conclude by emphasizing their ongoing commitment to staying connected and discussing the ever-evolving landscape of retail.

Episode Sponsor:

SAJO – Canada’s first specialized retail builder. Visit SAJO to see their holistic approach and transdisciplinary team to explore and understand your needs.

If you prefer to listen to the audio version, it is available below:

The Interview Series audio podcasts by Retail Insider Canada are available on Apple Podcasts, Stitcher, TuneIn, Google Play, or through our dedicated RSS feed for Overcast and other podcast players. Also check out our The Weekly audio podcast where Craig and Lee discuss popular content published on Retail Insider which is part of the The Retail Insider Podcast Network.

Subscribe, Rate, and Review our Retail Insider Podcast!

Drop us a line at Craig@Retail-Insider.com. You can also rate us in Apple Podcasts or recommend us in Overcast to help more people discover the show!

Background Music Credit: Hard Boiled Kevin MacLeod (incompetech.com). Licensed under Creative Commons: By Attribution 3.0 License. http://creativecommons.org/licenses/by/3.0/

Retail Insider is streamlining its Canadian retail news from around the web to include a handful of top news stories that can be viewed quickly during the day. Here are the top stories from the past 24 hours.

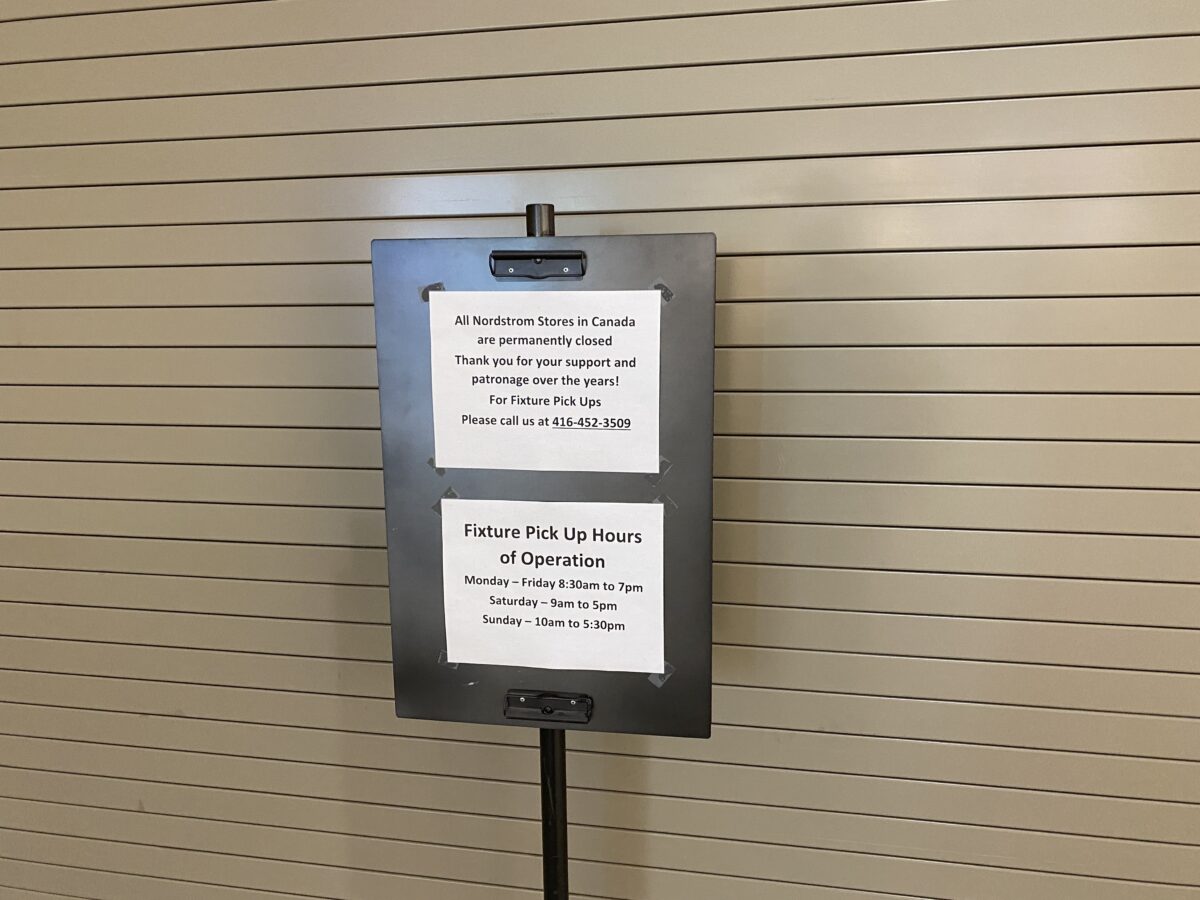

Nordstrom Closing at CF Toronto Eaton Centre (June 2023) Image: Dustin Fuhs

A recent survey reveals that despite moderate brand familiarity, American retail giant Nordstrom struggled with low visit frequency in the Canadian market, ultimately leading to its exit due to insufficient consumer engagement.

“Following the closure, 67 per cent of former customers turned to other retailers like Hudson’s Bay and La Maison Simons (among others), while 53 per cent expressed disappointment as those consumers had valued the retailer’s selection of clothing, quality products, and overall shopping experience,” said Luc Dumont, Senior Vice-President with Leger.

“This significant emotional impact and the diverse preferences for replacement retailers highlight substantial opportunities for other brands to capture the displaced customer base.”

Vacated Nordstrom at CF Rideau Centre (Image: Dustin Fuhs)Closed Nordstrom Canada at CF Toronto Eaton Centre (Image: Dustin Fuhs)

Dumont said the survey didn’t reveal anything super surprising.

“We did see that Nordstrom was recognized by many Canadians. Kind of a moderate awareness level. But as we all saw from its performance, they kind of struggled to turn this recognition into actual floor visits,” he said.

“Even before their departure from the Canadian market we could see that. They were struggling to convert that awareness into shop visits and sales.”

Based on his assessment of the brand’s marketing efforts, or lack thereof, Dumont said he felt that Nordstrom never really knew how to connect with the Canadian consumer which is completely different than the American consumer.

“I don’t have any examples of what that means but I think a lot of people were aligned with that thinking when they were here,” he said.

“Canadian consumers are very unique. Following the closures most shoppers say they adapted by turning to or going back to other retailers like The Bay and Simons, which I feel offer similar experiences in terms of their brand mix and their overall in-store experience.

“But it’s also notable to see that quite a few did not have or say they did not find a suitable replacement. That might highlight a bit of an opportunity for other retailers to fill that gap.”

Shuttered Nordstrom at CF Pacific Centre (Image: Lee Rivett)Nordstrom Rack Closing at 1 Bloor (Image: Dustin Fuhs)

Key highlights from the survey report include:

Nordstrom’s aided awareness is at 56 per cent, placing it in the mid-tier among the listed retailers. This indicates that while over 1⁄2 of Canadians were aware of Nordstrom, there is a significant portion that were not. Nordstrom’s awareness is higher than Saks Fifth Avenue (49 per cent) and La Maison Simons (49 per cent), but lower than The Bay (85 per cent) and lululemon (76 per cent);

While Nordstrom had a presence in Canada, it was not as deeply entrenched in consumer consciousness as some other major retailers. Nordstrom has a net familiarity of 35 per cent, which is lower than top retailers like The Bay (79 per cent) and Nike (76 per cent) but higher than Decathlon (22 per cent) and Saks (27 per cent). 66 per cent of respondents either did not know Nordstrom or had only heard of it without knowing any details, indicating a general lack of brand engagement;

Despite being familiar to many Canadians, Nordstrom faced challenges in attracting regular visitors, with 44 per cent of familiar respondents never having visited the store and 38 per cent visiting only rarely. This lack of frequent foot traffic, particularly among older age groups and lower-income households, suggests a disconnect between Nordstrom’s offerings and the needs of these demographics. The limited engagement likely contributed to Nordstrom’s decision to exit the Canadian market, highlighting the importance of converting brand awareness into actual store visits;

Following Nordstrom’s exit from the Canadian market, 67 per cent of its former shoppers have replaced it with other retailers, with The Bay being the top choice at 20 per cent, followed by Simons (11 per cent) and Winners (seven per cent). However, 26 per cent of respondents did not find a replacement. The variety of replacement choices, including specialty and second-hand stores, underscores the diverse preferences of Nordstrom’s former clientele, highlighting both the adaptability of consumers and potential market opportunities for retailers to capture this displaced customer base;

Nordstrom’s departure from Canada deeply affected its customers, with 53 per cent expressing disappointment. Their sentiments were primarily driven by the store’s valued clothing and brand selection, their fondness for shopping there, and its reputation as an excellent department store. The high net disappointment rate underscores the brand’s meaningful presence and the gap it leaves in the Canadian retail landscape. Customers also cited good merchandise, a unique product line, and good prices as key reasons for their disappointment of Nordstrom closing. This indicates opportunities for other retailers to capture this displaced customer base by emulating Nordstrom’s valued attributes and addressing the broader economic and community concerns stemming from its closure.

Updated glass galleria at CF Toronto Eaton Centre. Photo: Dustin Fuhs

Canadians’ spending intentions are improving sequentially and showing signs of life, according to a new survey by Stifel, an investment banking company.

Recently, the company published its quarterly survey assessing spending intentions for Canadians over the coming 12 months.

“Surprisingly, spending intentions are up sequentially in most of the categories we track and near a one-year-high. Categories such as mattresses, powersports, dollar stores, the pet industry, apparel and toys are all at or near a one-year-high,” said the report.

“While our survey suggests improvement in Canadian consumer confidence, spending intentions are still in a pattern of contraction with 52 per cent of respondents being likely or very likely to reduce their discretionary spending over the next 12 months. Despite that, these results piqued our curiosity and suggest investors should start to think about how to position their portfolio under a scenario where Canadian consumer confidence returns to an expansionary mode. Our survey results are positive for Sleep Country, Dollarama, Aritzia, Gildan, Pet Valu, KITS, BRP, and Spin Master.

“In our view, the results paint an accurate picture of the state of the Canadian consumer and historically the results have been generally a good indication of upcoming financial performance of our companies under coverage.”

Martin Landry, Managing Director, Equity Research for Stifel Canada, said the company was surprised by the increase in spending intentions that the survey suggests.

Martin Landry

“We’ve been carrying this survey for three years now. We’re doing it on a quarterly basis . . . Historically it’s been somewhat a good predictor of operational performance of our companies. So the recent results were quite upbeat,” he said.

“We saw a nice increase in spending intentions on discretionary items.”

Here’s Stifel’s take on the report:

Discretionary spending intentions rebound in July. After nine months of depressed spending intentions, the outlook appears to improve. According to our survey results, 48 per cent of respondents expect their spending on discretionary items to increase in the coming 12 months, up 400bps sequentially from April 2024. Interestingly, 14 per cent of respondents indicated they were “very likely” to increase their discretionary spending over the next 12 months, the highest proportion of the last five surveys we conducted. However, our survey would suggest we are still in a pattern of contraction as 52 per cent of respondents are likely to reduce their spending on discretionary items;

Stronger spending intentions for clothing and apparel vs. July 2023. 54 per cent of respondents to our survey expect to increase their spending on clothing and apparel in the next 12 months. While spending intentions for clothing and apparel appear stable sequentially, when compared to our July 2023 survey results, they came-in 400bps higher, which is surprising given the current economic slowdown. After nine months of spending intentions below 50 per cent, this is the second survey suggesting we are in an expansionary period for clothing and apparel. We view these demand trends as positive for Aritzia and Gildan;

Signs of demand recovery within the mattress industry continues. The demand environment for mattresses in Canada has been challenging for the past two-plus years. However, our survey results suggest that the outlook is improving with spending intentions up for two consecutive quarters, and with July 2024 showing the strongest spending intentions since March 2022. Hence, we could see a scenario for a rapid pickup in demand as the economic environment improves;

Demand trends for powersports vehicles appear resilient in Canada. Our survey results show that spending intentions for powersports vehicles appear to have rebounded sequentially and have reached their highest level since July 2022. These results align with BRP’s comments that demand weakness has been more pronounced in Asia Pacific, Europe and to some extent in the U.S., while Canada has been a bright spot. However, Canada represents roughly 15 per cent of BRP’s revenues. Hence, the impact on BRP’s overall results remains limited vs. the U.S. where BRP generates ~60 per cent of its revenues. We have seen no change in the demand environment in the U.S. as suggested by CDK Global data, which shows that recent demand trends at U.S. dealerships remain soft;

Demand intentions for the pet industry reach the highest level in a year. Following an unexpected drop in demand intentions within the pet industry in April 2024, demand trends appear to have improved sequentially with July 2024 spending intentions coming in at the highest level of the last 12 months. Compared to July 2023, demand intentions are flat, which we view as positive for Pet Valu. These trends paint a more bullish outlook for the pet industry than expected and may indicate that demand trends are better than feared;

Demand for “value” alternatives within eyewear products appear strong. On June 19th, KITS announced the official launch of its private label daily silicone hydrogel contact lenses. According to our analysis, KITS contact lenses are priced at a discount of roughly 40 per cent to national brands. According to our survey results, this should appeal to consumers as 74 per cent of respondents who buy contact lenses would consider switching to a private label brand if the price was at least 30% cheaper. While KITS’ private label contact lens business is small, we see a potential for the company to grow this segment, which should boost profitability given margins on KITS’ private label products tend to be much higher vs. margins on national brands products;

Spending intentions for the toy industry remain in positive territory. 54 per cent of respondents to our survey expect their spending on toys to increase in the next 12 months. This is a decline of 200bps sequentially from our April 2024 survey. However, 15 per cent of respondents said they are “very likely” to increase their spending on toys in the coming 12 months, the highest level in the last year. Overall, spending intentions within the toy industry have shown limited volatility over the past four surveys and have remained positive (i.e. a majority of respondents expect their spending to increase), which is a positive for Spin Master.

Landry said the results could be the start of the return of consumer confidence of Canadians which may seem a little bit counter intuitive to what we’ve been hearing lately.

“I could explain this by two things,” he added. “There’s been some healthy salary and wage increases over the last two years. Sometimes even higher than inflation and we’ve also got our first interest rate cut by the Bank of Canada. Although that’s not going to have a meaningful impact on mortgage payments yet, it’s the start of a trend towards interest rate reduction and maybe that plays out in consumer confidence and maybe that’s why we’re seeing that reflected in our survey.”

Retail Insider is streamlining its Canadian retail news from around the web to include a handful of top news stories that can be viewed quickly during the day. Here are the top stories from the past 24 hours.

According to the 2024 Deloitte Back-to-School Survey, spending for K-12 students will likely remain flat, estimated to reach a collective $31.3 billion in the United States, or approximately $586 per student this year.

The survey found that parents plan to make the most of early discounts, with 66 per cent of spending expected to occur by the end of July.

The results likely mirror the trend that will take place in Canada this year as well.

Key results of the survey include:

Surveyed parents plan to decrease their spending on technology products by 11 per cent year-over-year while increasing spend on other categories like personal hygiene and educational furniture by 22 per cent. Spending on clothing and school supplies remains unchanged.

Shoppers surveyed prioritize retailers offering value and convenience as mass merchants (77 per cent) and online retailers (65 per cent) are top destinations. In search of deals, parents plan to shop across 4.7 retail formats on average, up from 3.9 in 2023, and may sacrifice loyalty to stay within budget.

Despite financial concerns, 85 per cent of surveyed parents would splurge on their child’s must-have back-to-school products, and 50 per cent would shop for themselves.

In addition to spending on back-to-school products, 86 per cent of surveyed parents enrolled their children in extracurricular activities and plan to spend $582, including fees and equipment.

While more parents say their children use Generative Artificial Intelligence (GenAI) for their schoolwork than last year (23 per cent versus 15 per cent in 2023), they are divided on its benefits.

“We expect back-to-school spending to be flat to down modestly when adjusted for inflation, mainly driven by middle-income families juggling financial priorities and ongoing inflation perceptions. Retailers can expect headwinds to volume and loyalty as consumers seek to save money. However, wanting to please their kids, retailers will likely have opportunities to harness the indulgences parents are willing to make,” said Stephen Rogers, managing director, Deloitte Insights Consumer Industry Center, Deloitte Services LP.

Back to School at Hudson’s Bay Queen Street (Image: Dustin Fuhs)

The survey also found:

More surveyed parents plan to make the most of early discounts, with 66 per cent of spending expected to occur by the end of July, up from 59 per cent in 2023. 59 per cent believe the best deals occur earlier in the season, compared to 41 per cent who think they appear later.

On the hunt for deals, parents plan to shop across 4.7 retail formats on average, up from 3.9 in 2023.

While 62 per cent of parents surveyed respondents plan to shop within a fixed budget, they may sacrifice loyalty to do so: 67 per cent will shift brands if the preferred brand is too expensive, 62 per cent will shop at a more affordable retailer, and 50 per cent will shop for private labels over name brands, underscoring the need for retailers to offer incentives to keep shoppers engaged.

Back-to-school shoppers overwhelmingly cite mass merchants (77 per cent) as their most preferred retail format, followed by online retailers (65 per cent) and off-price retailers (tied with department stores at 39 per cent). Overall, seven in 10 surveyed seek convenience (convenient locations, delivery options, and easy returns) — making it the number one driver for where they plan to spend the most.

Multi-channel retailers account for 80 per cent of the total back-to-school intended spend, up from 73 per cent last year, and 70 per cent of families plan to shop in-store and online, up from 66 per cent.

Circularity comes to the forefront as more families plan to purchase used items to maximize value further: four in 10 (across income groups) surveyed expect to buy a used or refurbished item this season, up five percentage points among both middle- and high-income families. Technology and apparel lead the charge among pre-owned products (both at 28 per cent).

Social commerce is on the rise among K-12 parents, with one in three surveyed planning to use social media sites to assist in their back-to-school shopping, up eight percentage points year-over-year. In addition, one in eight plan to make a purchase on social media, up six percentage points from last year.

GenAI is nascent for back-to-school shopping, with 18 per cent of parents planning to use the technology when purchasing.

Nearly one-quarter of parents (23 per cent) say their children use GenAI for schoolwork, up from 15 per cent in 2023. However, parents are divided on its benefits: 35 per cent agree that GenAI is a positive tool for academic performance and overall learning experiences, compared to 33 per cent who disagree.

“Families are searching for deals and prioritizing value and convenience to save wherever possible. This dynamic creates an opportunity for retailers to take some of the anxiety out of the season by extending loyalty programs and incentives. In addition, building a seamless omnichannel approach could better position retailers to see consumers coming back throughout the season,” said Brian McCarthy, principal, Retail Strategy, Deloitte Consulting LLP

Nikki Baird, formerly at Forrester and RSR which she co-founded, now VP of strategy and product at Aptos, said the holiday season is always make-or-break for retail. Back to school gets attention as another major spending period, but it doesn’t always get due recognition for the unique role it plays in nurturing consumer trust and delivering on store expectations.

“Shopper emotions run high during the back-to-school season, driven by the nerves kids feel when entering a new school year and the stress parents feel over making that transition as smooth as possible,” said Baird.

“There’s an unmatched opportunity for retailers to play a special role in elevating the sentimental moment that takes place between child and parent in preparation for a strong school year.

“If retailers deliver a subpar experience during the back-to-school season, it will negatively impact their standing when consumers consider their holiday shopping plans.”

Back to School at Walmart (Image: Dustin Fuhs)

Matt Pavich, formerly at Target in merchandise buying, now senior director of strategy and innovation at Revionics, said regardless of how it is defined, consumers are looking for value even if the impacts of inflation are less pronounced than the previous two Back to School seasons. As consumers look for value, they are increasingly less loyal to individual retailers and open to finding value anywhere.

“BTS is a uniquely challenging event for retailers to plan for because it’s highly localized, as the school start dates differ . . . Having an analytics-informed localized pricing strategy is critical to succeeding during BTS. The decision to grow sales during BTS via lower pricing or extra promotions differs by retailer and by products. The best approach for most retailers is to stay true to their brand while leveraging analytics to find opportunities to drive optimal results,” he said.

“Clearance is an often-overlooked element of BTS pricing strategy, but it can be the difference for retailers between a highly successful and a poor-performing BTS period. In many ways, BTS remains a highly tactile in-store holiday due to the tradition of parents and children spending time together trying on clothes, debating what’s cool, and ultimately deciding on items to buy. This offers a great opportunity for retailers to drive traffic and adopt strategies to increase basket sizes during those shopping trips.”

By Derek Corrick, General Manager of Data Management, Pivotree

While Canadian businesses should be focused on shifting from survival mode to growth mode, many still find themselves working against tough economic times, and, largely due to their inability to adapt to modern ways of shopping, are faced with a wave of increased insolvencies. Regardless of the industry, modern solutions like artificial intelligence and automation have become increasingly important in an organization’s operations. To maintain a healthy and successful business, leaders must adapt their business to the latest landscape and ultimately, provide consumers with the seamless shopping experience they seek.

Coming out of the pandemic and faced with inflation, consumers changed their shopping habits and their expectations. While there were shifts in buying behavior as a result, expectations have remained high for a frictionless experience. Historically, customers prioritized quality service and fair pricing above all. Now, they expect more out of their shopping experience – personalized interactions, seamless shopping, proactive service and consistency across digital channels have become the norm for the modern consumer, with many considering the experience just as important as the product or service they’re paying for.

In a survey conducted by Pivotree and Canam Research, only 39% of commerce business leaders said that their commerce strategy and tactics were “definitely keeping pace” with changes in customer behaviour. How can the remaining 61% increase their chances of surviving and thriving, both now and in the future?

Start with clarity on value to customers.

Now more than ever, retailers and businesses need to be incredibly clear on the value they provide customers and to ensure they are delivering that value quickly, at scale, and with minimal costs. This is where technology can be leveraged most effectively to serve both the customer and the retailer’s bottom line.

The Find Buy GetTrust model remains king with Keep as the new heir.

To create a frictionless experience that addresses customers’ current and shifting needs, organizations must first look at how data, supply chain, commerce technology, and digital solutions work together holistically. Let’s look through the lens of the Find Buy Get Trust model.

For “Find” to be frictionless it goes beyond the basics of search and discover – it involves a relationship with your customer and an understanding and anticipation of customer needs. Canyour customers find the items they’re looking for? Do their search parameters match up to the attributes on your site?

The “Buy” aspect of the value chain is vital. Whether your customers buy online, in-store, or through a distributor, the right commerce platform enabled with the right product data will ensure a smooth purchase experience. With data, supply chain data, and commerce technology seamlessly integrated the buyer experience is enhanced. That’s where “Get” comes into play. Whether a customer wants to try a product before they purchase, buy online and pick up in store, or ship to a locker, customers want to receive their products in a variety of ways. And they want to understand when they can expect to get the product.

Lastly, being able to fulfill a customer’s desire builds “Trust” in your brand and ultimately, will enhance lifetime value. Trust is built through engagement. Leveraging data to drive trust both in-store and online will help your customers find, buy, and get the products they want, as well as ensure their financial and personal data are safe and secure.

While this model has remained essential in the retail space for decades, “Keep” is a newer part of the model that has become increasingly important for a retailer’s bottom line. Returns cost businesses a lot of money. Even if the item is returned in good condition, the entire process is costly because of the required labour, transport, and inspection; and that’s not even considering the environmental impact. While streamlining returns and making it easier for customers is important, returns have become a big challenge for retailers. Many consumers now tend to over-purchase and return products that they don’t want or need, creating a surplus of products that can become hard to resell. Navigating how to get customers to keep what they buy must also be considered when assessing the health and future of a retail business.

Technology is only a part of the system, and data is at the heart of it.

When talking about ‘future-proofing’ a business, many immediately think of technology. However, technology is only part of the problem. Oftentimes, when a business is struggling, retailers look to new technology solutions to resolve their issues, when really (in a lot of cases), the problems they’re experiencing are symptoms from a lack of data quality, consistency, and completeness. Before any organization can implement meaningful technology, they must invest in optimizing their data first. From helping retailers find efficiencies that reduce costs, to facilitating smoother returns operations, data is at heart of a retailer’s ability to deliver a frictionless experience to customers.

To succeed, now and in the future, invest in AI and automation.

Automation and generative AI offer the potential to transform retail operations, driving efficiency, innovation, and profitability in an increasingly competitive landscape. Generative AI can analyze vast amounts of data to make accurate predictions about customer preferences, demand forecasting, and inventory optimization as well as reduce errors in ordering and stocking.

AI-powered recommendation engines can also analyze customer behavior and preferences to provide personalized product recommendations, enhancing the shopping experience and driving sales.

On the dynamic pricing front algorithms can analyze market conditions, competitor pricing, and customer behavior to optimize pricing strategies in real-time to stay highly competitive. Automation tools can monitor inventory levels in real-time and automatically reorder products when stock runs low. This minimizes the risk of stockouts and ensures that popular items are always available to customers.

By leveraging automation and generative AI, retailers can differentiate themselves from competitors by offering superior customer experiences, optimizing operations, and staying ahead of market trends.

Derek Corrick

Derek Corrick is an experienced Information Management practitioner with an abiding commitment to the success of his customers. As Pivotree’s General Manager for data management (DM), he leads a team dedicated to helping companies leverage their information assets to deliver clear and measurable business results, increase sales, drive enterprise efficiency, and enhance customer experience/engagement – all while reducing business risk. Prior to joining Pivotree, Derek founded and managed successful DM and Information Management practices at two leading consultancy firms, and served as Executive Vice President for a major DM solution provider. His passion spans DM implementation excellence, change management, business development, and digital transformation.

About Pivotree: Pivotree, a leader in frictionless commerce, strategizes, designs, builds, and manages digital Commerce, Data Management, and Supply Chain solutions for over 200 major retailers and branded manufacturers globally. With a portfolio of digital products as well as managed and professional services, Pivotree provides businesses of all sizes with true end-to-end solutions. Headquartered in Toronto, Canada, with offices and customers in the Americas, EMEA, and APAC, Pivotree is widely recognized as a high-growth company and industry leader. For more information, visit www.pivotree.com or follow the company on LinkedIn.

*Partner content. To work with Retail Insider, email Craig Patterson at craig@retail-insider.com

Barcodes, those ubiquitous stripes we encounter daily at checkout counters, are far more than mere patterns; they are pillars of modern food distribution and traceability. Celebrating its 50th anniversary, the Universal Product Code (UPC) barcode first made its mark on June 26, 1974, in a supermarket in Troy, Ohio. Interestingly, Canada quickly followed, becoming the second country to adopt this system in July 1974, with its first scan at a Steinberg grocery store in Dorval, Quebec.

Despite their everyday presence, UPC barcodes remain underappreciated. These codes have revolutionized retail and supply chain sectors by enabling efficient product identification and inventory management, thereby enhancing our food industry’s efficiency. At retail checkouts, these barcodes encode a unique 12-digit number for each product, facilitating quick, accurate transactions without the need for manual data entry. This not only speeds up the checkout process but also reduces errors, akin to how fingerprints uniquely identify humans.

Barcodes are invaluable for tracking sales trends, managing promotions, and making informed inventory decisions, thus enriching the overall shopping experience for consumers. Beyond the point of sale, UPC barcodes optimize inventory and supply chain operations by allowing precise monitoring of stock levels, facilitating timely reorders, and preventing stockouts and overstock situations. Essentially, barcodes are indispensable tools that support both the logistical and commercial aspects of modern retailing.

The success of the UPC barcode owes much to the GS1 standards, set by a relatively unknown non-profit organization, which have been instrumental in enhancing the reliability of supply chains worldwide. In Canada, GS1 ensures that businesses benefit from standardized barcodes, improving supply chain efficiency and product traceability. It provides essential tools and guidance for adopting these global standards, helping businesses streamline operations, reduce errors, and maintain accurate product information from production to retail.

However, the system is not flawless and is susceptible to human error, highlighting the need for a neutral, non-profit arbitrator to ensure compliance.

Barcodes are here to stay, but as the need for greater traceability grows, the traditional 12-digit single-layered code is no longer sufficient. The introduction of data matrices and QR codes—types of two-dimensional barcodes—marks the next step in barcode evolution. These advanced codes could manage real-time food recalls or provide consumers with detailed product information, potentially obviating the need for “Best Before” dates. Opportunities are endless.

Thus, each time we scan a barcode, we engage with a marvel of logistics that connects us transparently to an industry that often seems opaque. This is just the beginning; as we delve deeper into barcode technology, its potential to transform our food system becomes even more apparent.