The Condo Retail Sales Report: Trends and Insights 2019-2024 by JLL examined the condo retail real estate market trends in Toronto, analyzing transaction data to provide insights into market performance and dynamics.

“The condo retail real estate market has experienced notable shifts during this period, influenced by macroeconomic conditions such as interest rate changes and evolving investor sentiments,” it said.

“The data reveals a market that has navigated fluctuations in pricing and capitalization rates with 2023 and 2024 marking a decline in total transaction volume while maintaining relatively stable PPSF levels.”

The analysis concentrates exclusively on ground level retail space at the base of residential developments (those with condominium and stratified freehold ownership titles – both of which, for the purposes of this report, are referred to as ‘condo retail’’) located from Jane Street to the west, St. Clair Avenue West and Lawrence Avenue West to the north, and the Don Valley Parkway to the east (plus Leslieville) and Lake Ontario to the south.

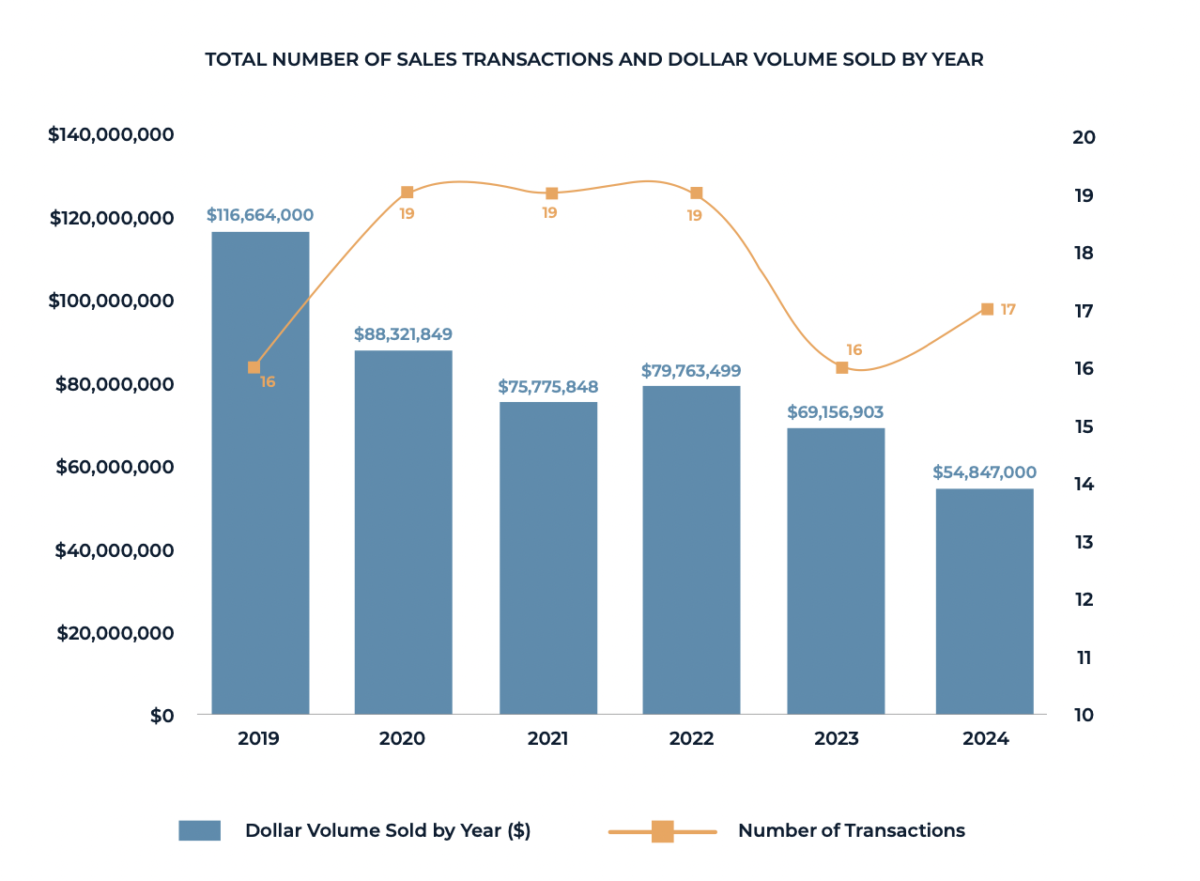

“The total dollar volume of retail transactions over the six-year period was $484.5 million, peaking in 2019 at $116.6 million, followed by a consistent decline through to 2024, where volume dropped to $54.8 million – a 53% decrease over six years. The decrease is likely attributable to a combination of factors, including higher borrowing costs, cautious investor sentiment, and diminished property valuations resulting from increasing capitalization rates,” said the report.

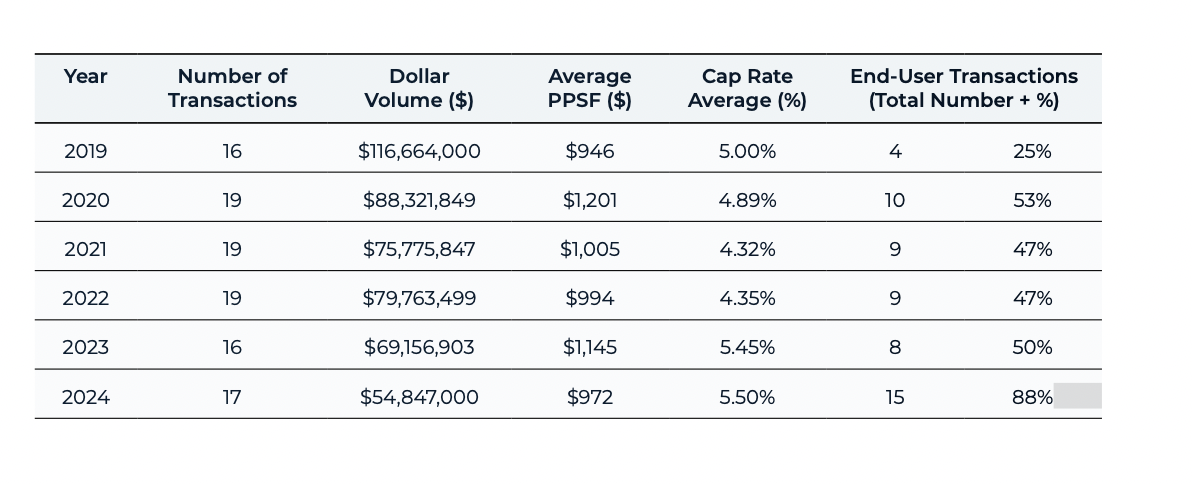

“The total number of condo retail sales completed from 2019 through to the end of 2024 is 106. Transaction volume remained relatively stable in terms of deal count, with the number of transactions per annum ranging from 16 to 19. The years 2020, 2021, and 2022 saw the highest number of transactions at 19 each, while 2019 and 2023 had the lowest at 16. This stability in transaction count suggests a consistent level of market activity despite fluctuations in total dollar volume.

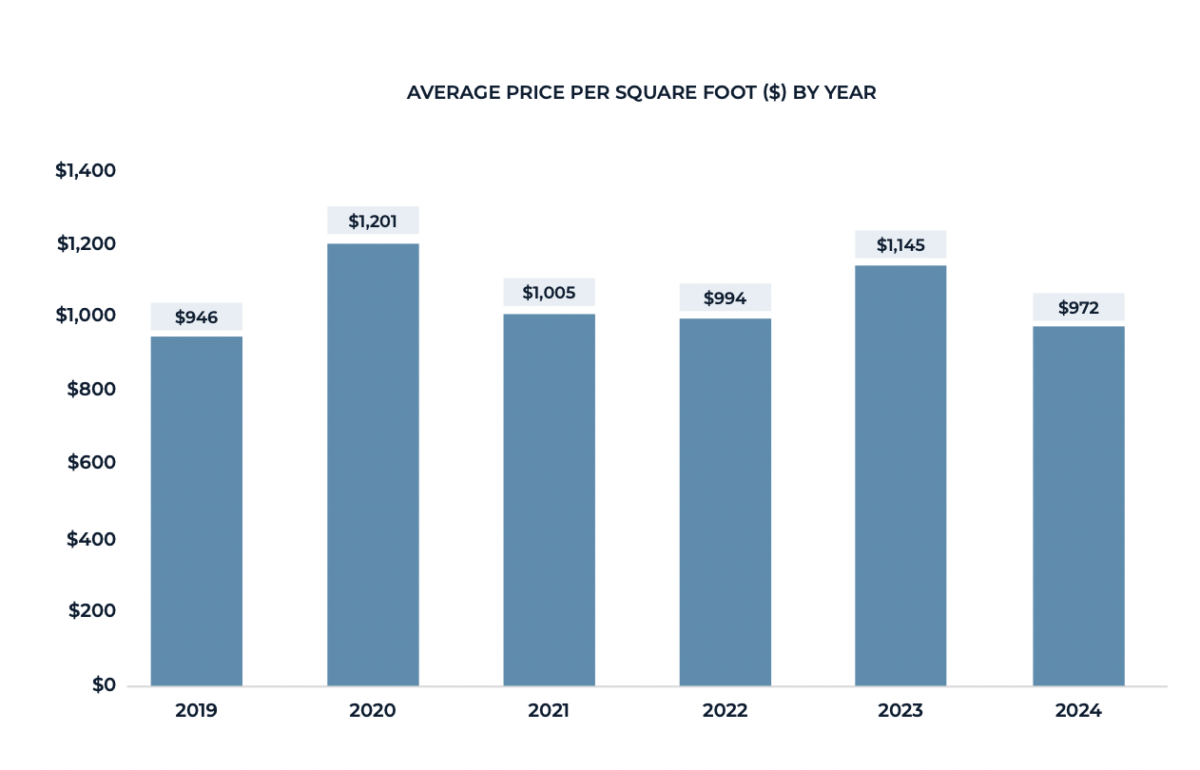

The report said the average price per square foot (PPSF) has fluctuated significantly over the six-year period, with no clear upward or downward trend. It reached its peak of $1,201 in 2020, following a rise from its lowest point of $946 in 2019, representing a 27% increase. These fluctuations might reflect changes in the mix of property types being sold, location variations within the study area, and overall market volatility influenced by broader economic factors. Subsequent years have seen various shifts in PPSF, indicating a dynamic and unpredictable market environment.

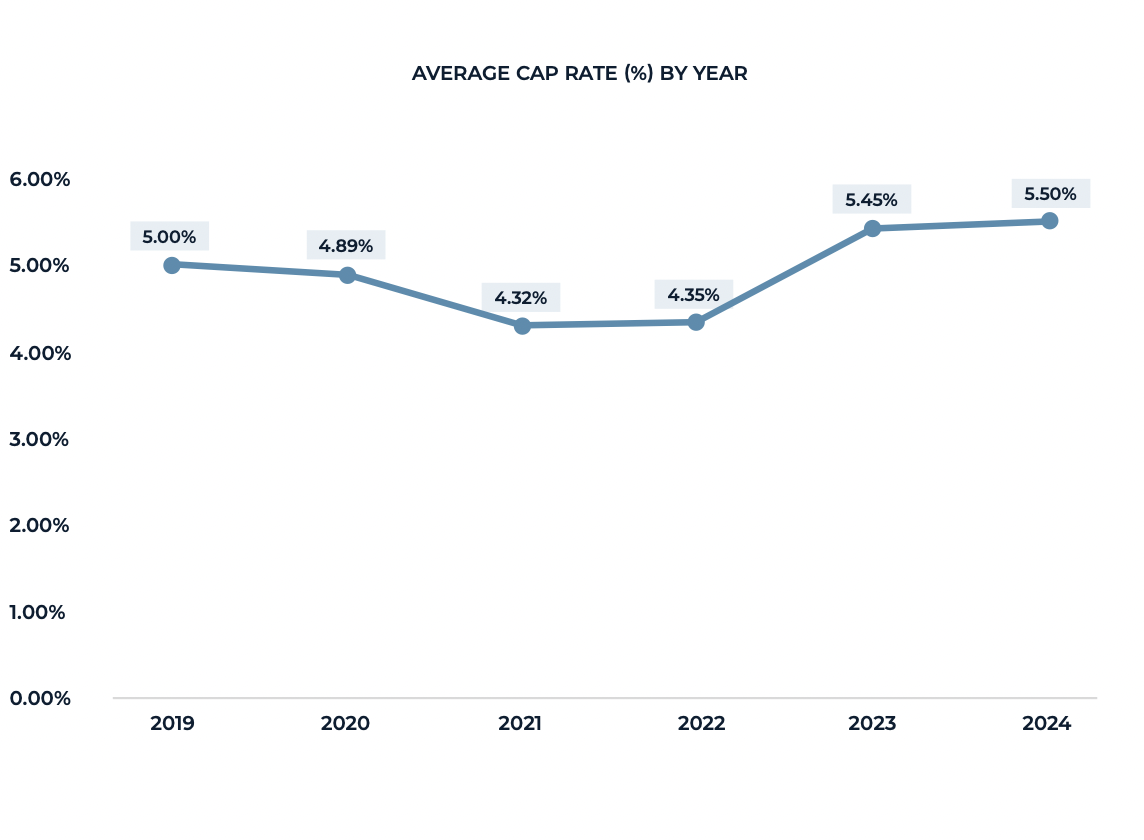

“Cap rates have shown notable variation over the study period, ranging from a low of 4.32% in 2021 to a high of 5.50% in 2024. There is an upward trend in recent years, with 2023 hitting a 5-year high of 5.45% before reaching 5.50% in 2024. The lowest average cap rate was recorded in 2021 at 4.32%, indicating peak investor confidence during a period of historically low interest rates. Conversely, the highest average cap rates were observed in 2024 (5.50%) and 2023 (5.45%), reflecting softening market conditions and a shift towards buyer-favourable pricing. This upward trend in cap rates aligns with the broader economic context of rising interest rates and increased market uncertainty,” explained JLL.

A significant shift towards end-user transactions has been observed from 2019 to 2024. In 2019, only 25% of sales were to end-users, but by 2024, this proportion had risen dramatically to 88.2%. This trend clearly demonstrates a growing preference for owner-occupied properties, particularly among professional services such as dentists, who are increasingly focused on purchasing their own real estate, noted the report.

Several factors have prompted this shift towards owner-occupier purchases:

1. Lower sales velocity for income-producing assets

2. Rising interest rates, making ownership potentially more attractive than leasing

3. The desire for greater control over property use and potential for long-term appreciation

“This trend has implications for both the market dynamics and the future composition of condo retail space ownership, potentially leading to a more diverse and stable tenant mix in these properties,” it said.

The report said the average size of transactions has fluctuated significantly over the study period. 2019 stands out with the largest average transaction size of 7,780 square feet. Subsequent years saw a shift towards smaller average transaction sizes, ranging from 3,514 to 4,953 square feet. This trend aligns with the increasing proportion of end-user transactions, which historically have resulted in smaller unit sizes. This is exemplified in 2024, where 15 end-user transactions averaged just 2,902 square feet, significantly below the overall average for the period. This shift in transaction size reflects the changing nature of demand in the condo retail market, with smaller, owner-occupied units becoming increasingly prevalent.

“The retail real estate market from 2019 to 2024 reflects a period of significant transition. While total transaction dollar volume has declined substantially, pricing metrics such as price per square foot (PPSF) have shown resilience. Simultaneously, cap rates suggest a recalibration of investor expectations in response to changing market conditions,” said the report.

Looking ahead, investors should closely monitor several key factors, it added:

1. Interest rate movements and their impact on financing costs

2. Consumer spending patterns and their effect on retail performance

3. Evolving retail fundamentals, including the shift towards end-user ownership

“These factors will be crucial in identifying opportunities in a market that is adjusting to new economic realities. The increasing trend of end-user purchases, particularly among professional services, may continue to shape the landscape of condo retail real estate in the coming years,” said JLL.

The condo retail sales market for 2025 is expected to stabilize, with several key trends emerging, added the report:

- End-user interest is projected to remain strong, driven by consistent lending environments and more affordable debt. However, we anticipate user transactions as a percentage of the overall market to decrease from the record high of 88.2% seen in 2024;

- Economic uncertainties in the United States are fostering caution among Toronto investors. Nevertheless, the cap rate precedents set in 2024, averaging 5.50%, may provide sellers with confidence in asset values;

- We expect more high-profile assets to trade in 2025, potentially leading to an increase in both overall dollar volume and number of transactions from the $54.8 million and 17 transactions recorded in 2024;

- Price per square foot figures are expected to remain stable, continuing the trend observed in recent years. Vacant condo retail assets are expected to trade within a consistent value band, similar to the $972 per square foot average seen in 2024.

“The stabilization of the market may attract a more diverse range of investors, balancing the recent dominance of end-users. This could lead to a more dynamic and competitive market environment.”

Related Retail Insider stories:

")