Analysis by J.C. Williams Group

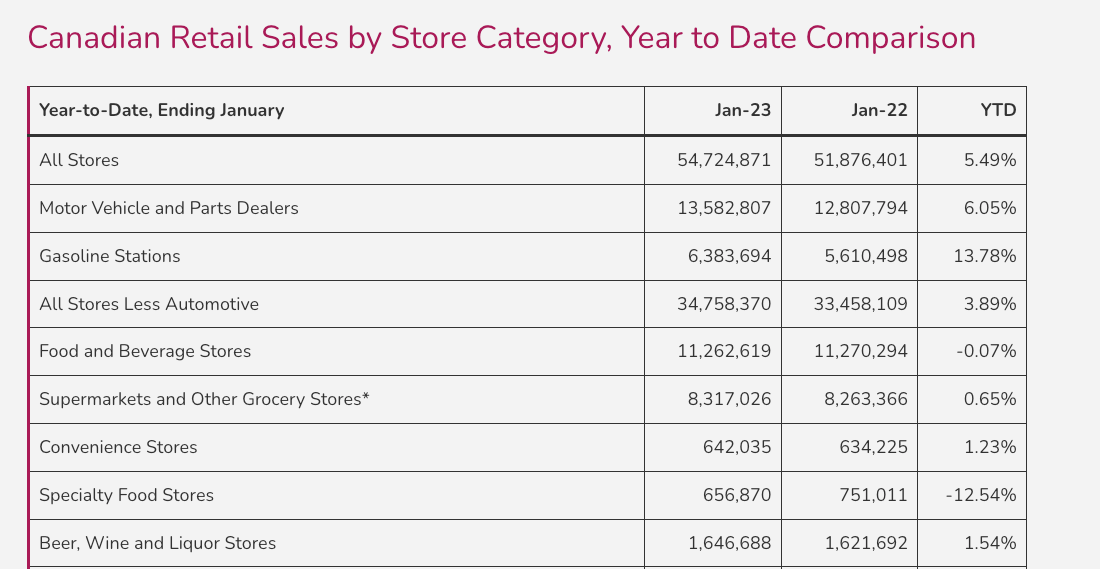

Continuing the trend towards the end of 2022, Canadian retail sales started with minimal growth in 2023 with All Stores in January growing 5.5% YOY and All stores Less Automotive, Food, Pharmacies up 4.5% YOY.

The first element to remember when comparing January 2023 to January 2022 is that there was a lockdown in Ontario last year. With Ontario typically contributing to around one-third or more of total Canadian retail sales, this has a large impact on national retail sales.

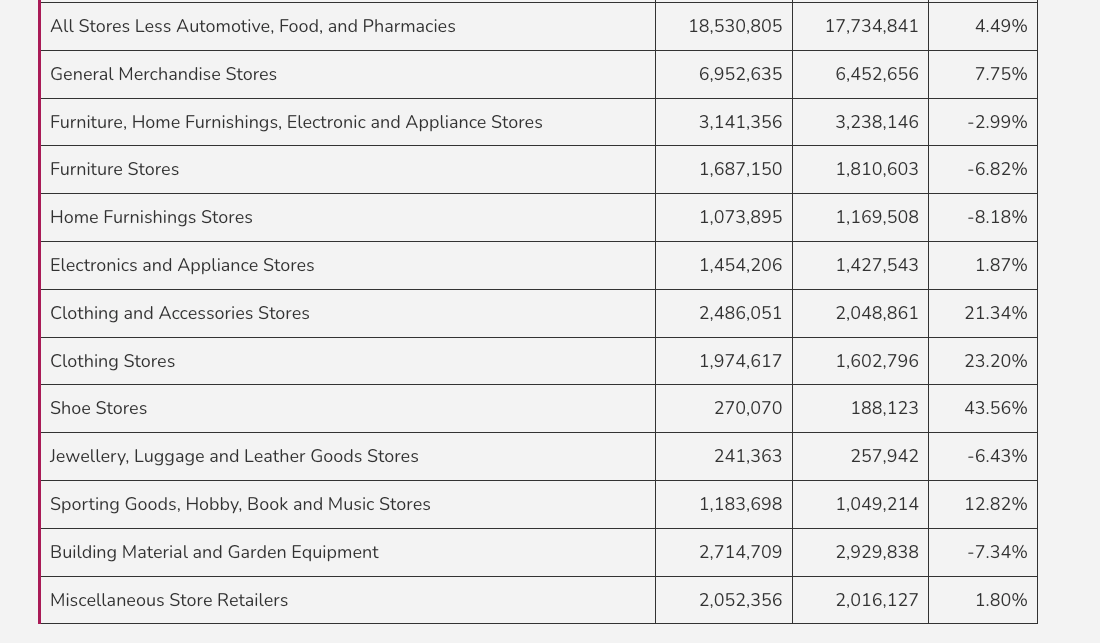

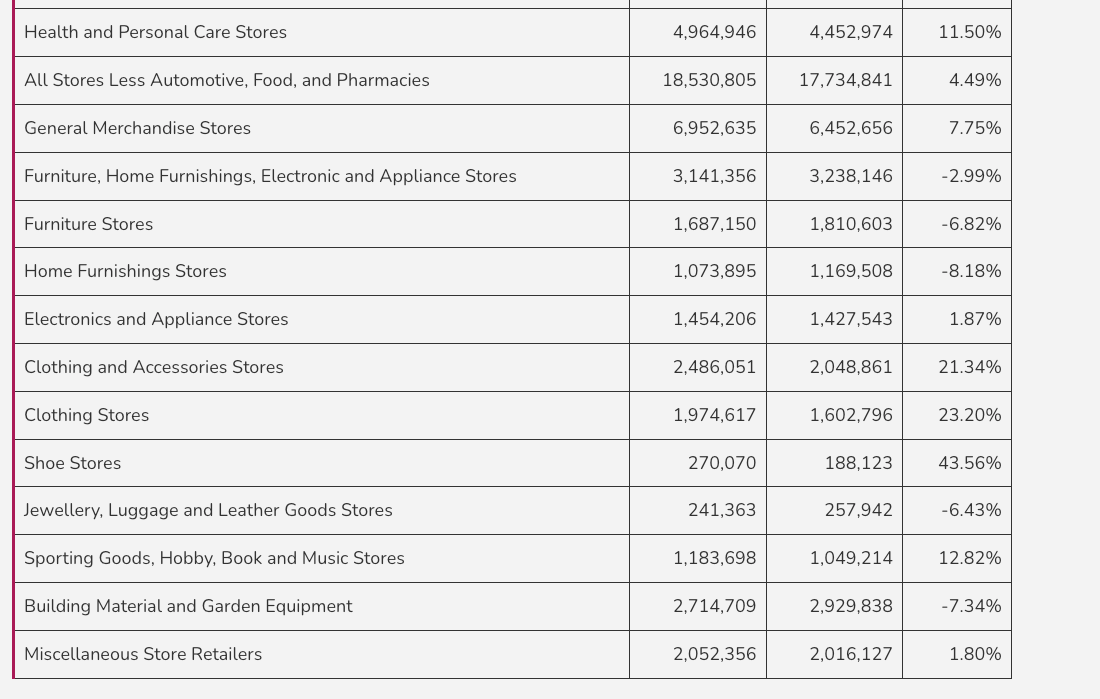

Even when considering the lockdown, it is still surprising to see that Clothing and Accessories Stores increased by 21.3% YOY in January. The subcategories grew impressively, at rates of:

- Clothing Stores: Up 23.2%,

- Shoe Stores: Up 43.6%, and

- Jewellery, Luggage and Leather Good Stores: Down -6.4% YOY.

These abnormalities are likely directly related to the fact that Ontario was in lockdown in January, 2022. When comparing sales to 2019, the numbers are much more normalized:

- Clothing Stores: Up 11.3%,

- Shoe Stores: Up 11.4%, and

- Jewellery, Luggage and Leather Good Stores: Up 20.6% YOY.

The other standout category in January is Food and Beverage Stores, down -0.7% YOY. The largest drop off in this category is Specialty Food Stores, down -12.5%, but all categories grew at a rate below inflation, which is 10.4% in January for food prices. When the JCWG team discussed these changes, we landed on the fact that people are still only spending what they have. There are few people whose income has increased by 10% over the past year, so the distribution of where they are spending their food budget has changed. Consumers are looking for better pricing, moving towards Walmart, Costco, etc. for grocery, which was shown through the 7.8% YOY increase in General Merchandise Stores. Specialty Food Stores include butcher shops, cheese shops, etc. which have been some of the most impacted products from inflation.

2023 promises to be a tumultuous year for Canadian retail sales. Inflation is very relevant, customers have resumed most of their previous shopping habits (hopefully for good), and we are still in the throws of a recession. With that being said, major disruptions with chain retailers in Canada, namely the exit of Nordstrom and the re-entrance of Zellers will impact the coming months. This has the team thinking about:

- Where will current Nordstrom customers shop for their mid-luxury/luxury products?

- How long will it take for shopping centres to fill the Nordstrom vacancies and how will the vacancy impact traffic flow and footfall?

- How many, if any, current discount department store customers will change their habits to Zellers, and away from Walmart, Costco, Dollarama, etc.?

- What international retailers are currently eyeing Canada for expansion opportunities?

- How are YOU prepared for the changed Canadian retail landscape?

This analysis by J.C. Williams Group is updated monthly as new numbers are published by Statistics Canada.

J.C. Williams Group focuses solely on Retail sector strategy and consulting. The breadth and depth of our functional areas of retail specialization enable us to bring to each engagement a holistic perspective and expertise that provides both insightful and actionable recommendations.