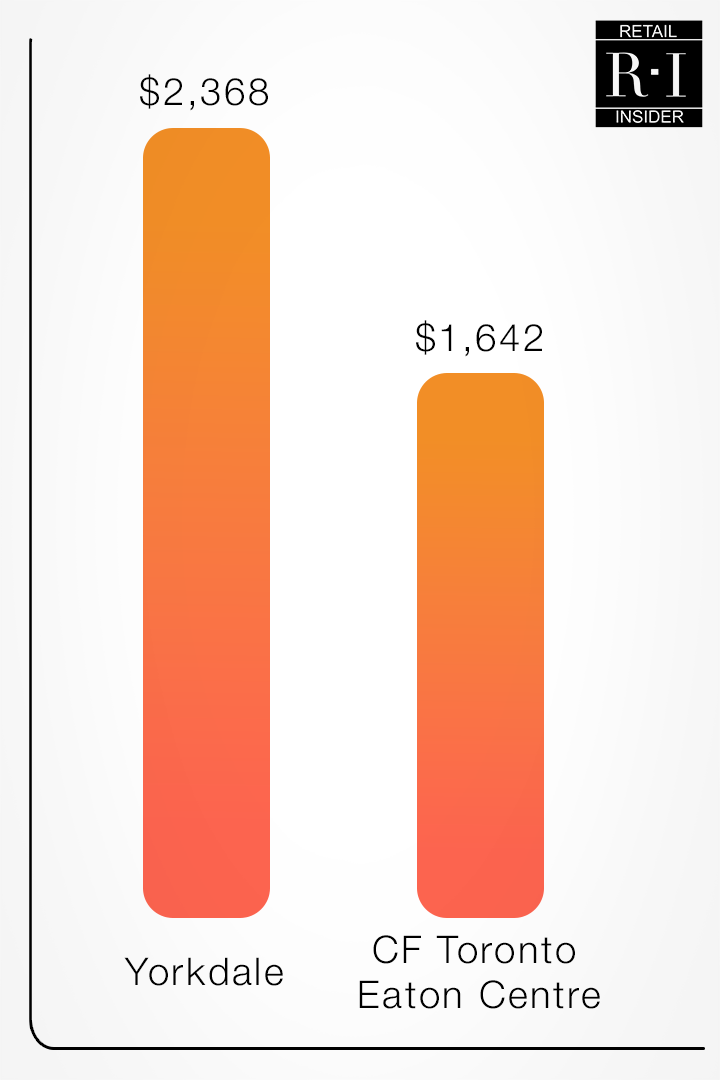

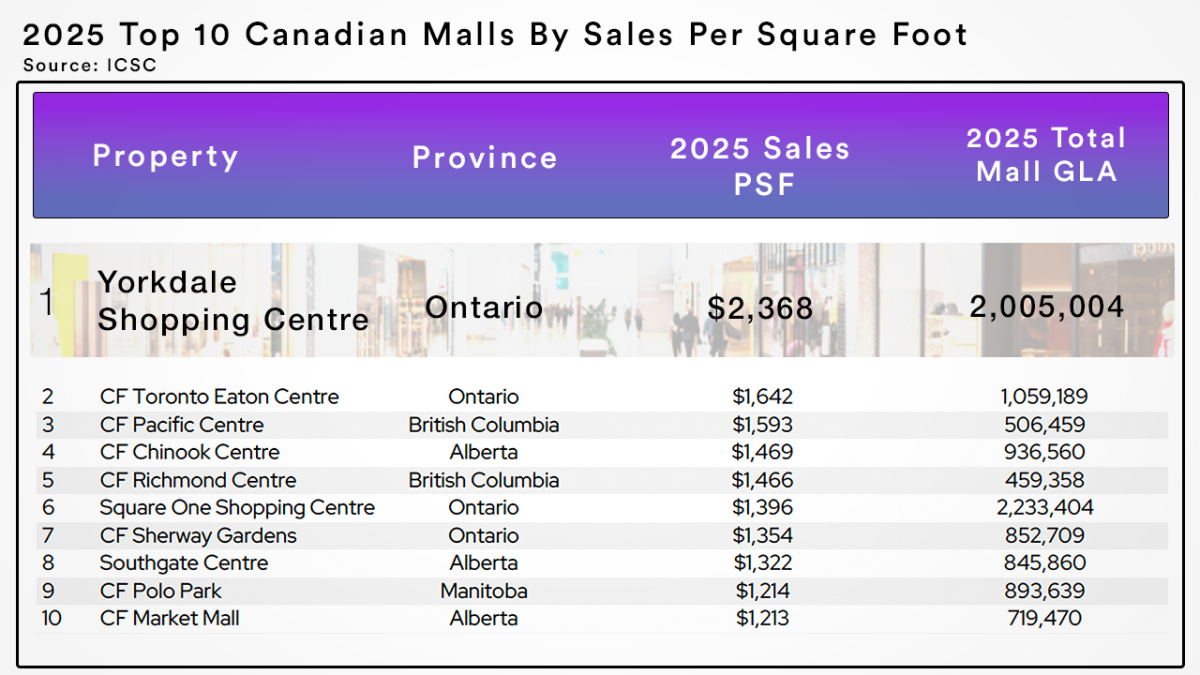

Canada’s highest-performing shopping centres continue to demonstrate strong productivity, with Yorkdale Shopping Centre once again leading the country by a wide margin. According to newly released data from ICSC, Yorkdale recorded sales of $2,368 per square foot in 2025, maintaining its position as Canada’s most productive retail asset.

The gap between first and second place remains significant. CF Toronto Eaton Centre ranked second with $1,642 per square foot, followed by CF Pacific Centre at $1,593. The spread highlights the continued strength of top-tier urban shopping centres, particularly those located in major gateway markets such as Toronto and Vancouver.

Top-Tier Centres Continue to Lead

Several of Canada’s most prominent malls rounded out the upper tier of the rankings. CF Chinook Centre in Calgary reported $1,469 per square foot, while CF Richmond Centre and Square One Shopping Centre posted $1,466 and $1,396 respectively.

The presence of multiple Greater Toronto Area properties among the top performers reinforces the region’s role as the country’s most competitive retail market. At the same time, strong results from centres in Vancouver and Calgary point to sustained demand in key Western Canadian markets.

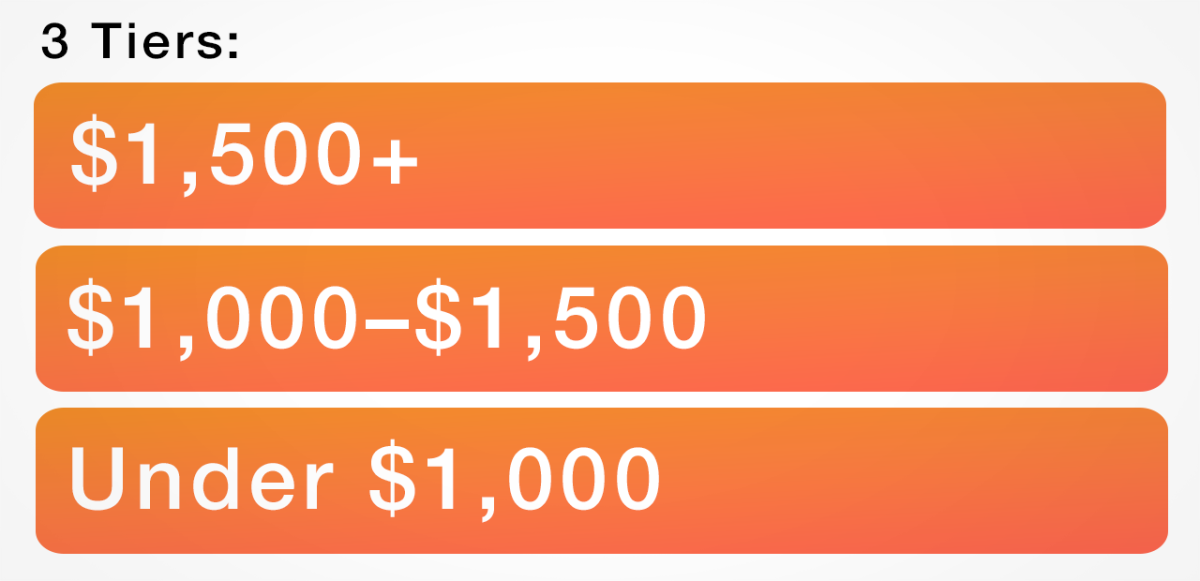

Notably, several properties exceeded $1,300 per square foot, placing them firmly within what industry observers often view as the highest echelon of retail productivity. These centres tend to feature a curated mix of luxury, premium, and high-performing international brands, along with strong food and experiential offerings that drive consistent traffic.

The $1,000 Per Square Foot Benchmark

Beyond the top tier, a substantial number of Canadian shopping centres reported sales above $1,000 per square foot in 2025. This threshold is widely considered a benchmark for strong performance in enclosed malls, reflecting healthy tenant productivity and sustained consumer demand.

Centres such as CF Masonville, CF Carrefour Laval, and Metropolis at Metrotown all fall within this range, demonstrating that high-performing retail is not limited to a single region.

At the same time, the data suggests a widening performance gap across the sector. While top-tier assets continue to achieve strong results, many mid-tier and lower-tier centres report significantly lower sales productivity, often below $700 per square foot. This divergence reflects broader structural shifts within the retail landscape, where tenant demand and consumer traffic are increasingly concentrated in dominant, well-located properties.

Performance Shifts Highlight Changing Dynamics

Year-over-year changes provide additional insight into evolving market conditions. Some centres posted notable gains, including CF Chinook Centre, which saw one of the largest increases in sales per square foot. In contrast, others experienced declines, including CF Sherway Gardens, underscoring the variability in performance even among established assets.

These shifts may reflect a combination of factors, including tenant mix changes, redevelopment activity, evolving consumer preferences, and broader economic conditions. As retailers continue to rationalize store networks and prioritize high-performing locations, top-tier centres are often the primary beneficiaries.

Concentration of Retail Performance Continues

The 2025 data reinforces a broader trend within Canadian retail real estate. Rather than a uniform recovery across all properties, performance is increasingly concentrated among a relatively small group of dominant shopping centres.

These leading assets continue to attract investment, premium tenants, and redevelopment activity, while lower-performing centres face growing pressure to reposition through mixed-use development, experiential offerings, or alternative uses.

As Retail Insider continues to analyze this dataset, upcoming coverage will explore multi-year trends, regional dynamics, and the long-term implications for Canada’s shopping centre landscape.

Notable Shopping Centres Absent from the Dataset

While the 2025 rankings provide a comprehensive snapshot of participating properties, several major Canadian shopping centres are not included in the data submitted to the International Council of Shopping Centers.

Industry sources indicate that these properties rank among the highest-performing shopping centres in Canada by sales productivity. Their absence means that the ICSC list, while highly valuable, does not represent a complete ranking of all top-tier retail assets across the country.

Notably, West Edmonton Mall, owned by Triple Five Group, does not report sales per square foot through ICSC. Similarly, Park Royal, owned by Larco Investments, is absent from the dataset.

In addition, major outlet centres such as Toronto Premium Outlets and McArthurGlen Designer Outlet Vancouver Airport are also not included in the ICSC-reported figures.