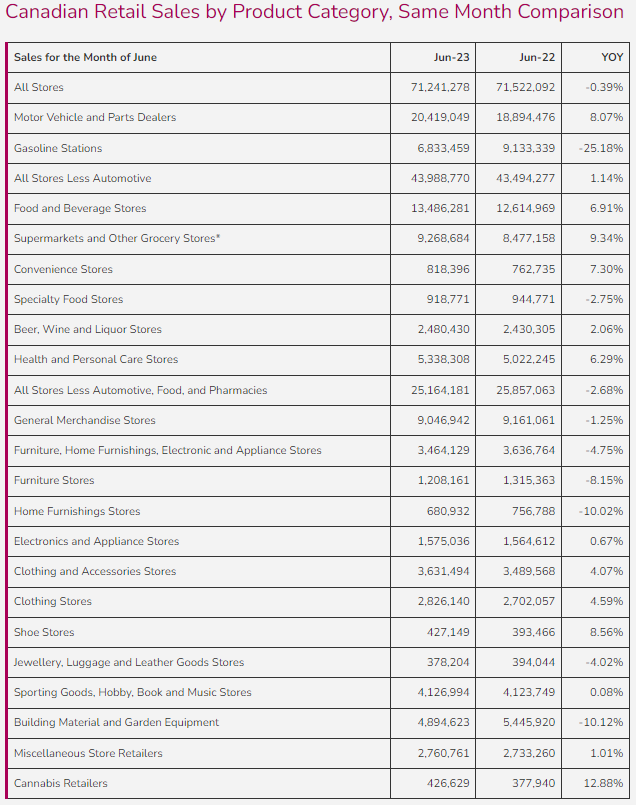

Canadian retail sales began to decrease in June 2023 with All Stores in June decreasing -0.4% YOY and All stores Less Automotive, Food, Pharmacies down -2.7% YOY as inflation continues its stronghold on Canadian consumers.

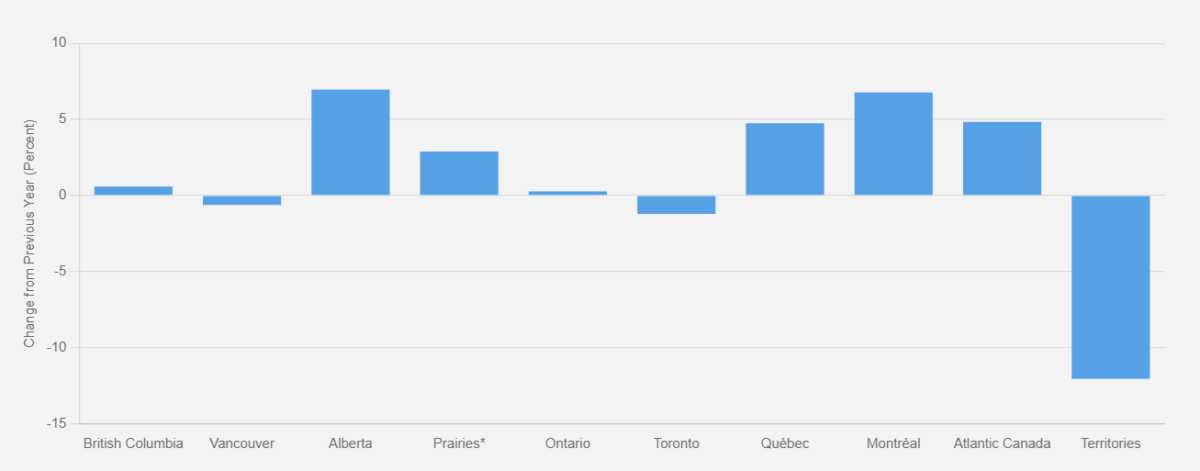

The decreases in sales is in part due to the continued decreases in spending in the two most expensive cities in the country: Toronto and Vancouver, down -1.2% YTD and -0.6 YTD respectively. These two cities account for, on average, approximately a quarter of total Canadian retail sales. As such, with the cost of living being the highest of all cities in Canada, consumers in these regions seen to be cutting back their spending more than others. In addition to the cost of living, June was a period of unprecedented wildfire smoke in Ontario, which likely kept many consumers inside and not spending. There are numerous categories in June that are reflective of the effects of inflation:

- Supermarkets and Other Grocery Stores, though up 9.3% YOY, rising food costs are up 9.1% over 2022, therefore a much less impressive increase,

- Building Material and Garden Equipment, down -10.1% YOY, and

- Furniture, Home Furnishings, Electronics and Appliance Stores are all down in June, reflecting the effects of inflation down -4.8% YOY.

Apart from food, both other categories comprise of big ticket items, products that customers simply cannot afford at the moment. Rona, a significant retailer in the Building Material and Garden Equipment category, reported the elimination of 500 jobs in June as a result of these changing market conditions.

Though June will not yet reflect back-to-school sales, 2023 is expected to shower lower performance compared to previous years. As we are approaching the end of August, this is top of mind at JCWG. The Retail Council of Canada performed a survey of Canadian consumers for back-to-school with some interesting results:

- 81% of Canadians intend to shop at brick-and-mortar retailers in their neighbourhood rather than online,

- 60% of Canadians expect to spend on stationary (the top category), whereas in 2022 stationary didn’t even crack the top ten, and

- Big box stores are expected to take 62.3% of back-to-school sales in 2023.

The expected back-to-school trends from the survey are not surprising with wider inflation trends, such as consumers not looking to purchase electronics (typically big ticket items). As we are in the throws of back-to-school at the writing of this bulletin, and even approaching Halloween, JCWG is thinking about:

- Did Amazon Prime Day have the impact on Canadian sales that it does in the US in July?

- Will Halloween be the latest shopping event to experience the post-pandemic “holiday creep” (moving the shopping season further forward)?

- Which retailers will be the most successful in back-to-school with the changes in consumer preferences?

- Are city sales decreases in part as a result of tourism, or mainly residents?

- How have YOU prepared for the transition from back-to-school to Halloween?

For support with your retail strategy and seasonal merchandise planning, reach out to the trusted experience at JCWG!