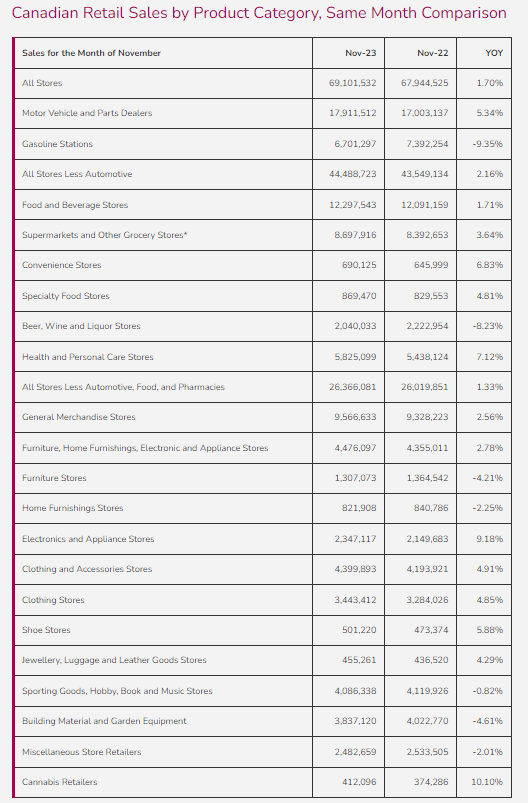

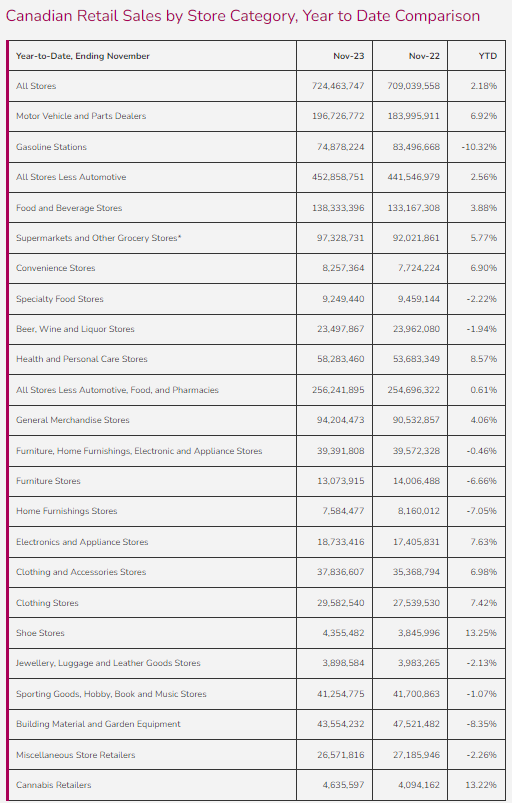

Canadian retail sales grew a mere 1.7% YOY for All Stores in November, with discretionary categories growing even less at 1.3% YOY for All Stores Less Automotive, Food, and Pharmacies.

Black Friday, as with recent years, continued to excel past its prior record-breaking results with sales increasing 24% (reported by Shopify) and 14% (reported by Square) over 2022. Square, who also owns Afterpay, experienced a 29% increase in customers using the “buy now, pay later” payment platform. This is reflective of the trend of consumers delaying larger purchases, or in this case, simply delaying larger purchase payments. The top categories, according to Shopify, were apparel and accessories, health and beauty, and home and garden, which was not necessarily reflected in the Canadian sales numbers. While Clothing and Accessories Stores (up 4.9% YOY) and Health and Personal Care Stores (up 7.1% YOY) performed well, Furniture Stores, Home Furnishings Stores, and Building Material and Garden Equipment Stores were down -4.2%, -2.3%, and -4.6% YOY respectively. This is likely partly a reflection of the delays of larger purchases with Canadians, and the increased housing costs meaning people are spending more on their houses and less on what goes in/around them a trend we had seen at the height of the pandemic.

For the third month in a row, Motor Vehicles and Parts Dealers saw increased revenues, with November sales increasing by 5.3% YOY. There are numerous factors that could be affecting this trend:

- The average price of a new vehicle in Canada continues to rise, with the current average being $67,817,

- Many consumers had moved away from larger cities to work remote but are now required in the office at a hybrid capacity. As such, their gas-guzzling vehicles may not be ideal for a longer trip as costs continue to rise. In addition, couples may only have one car and need a second if they are living in a remote area and need to commute,

- Linking both the average price and the need for vehicles increase, consumers may be opting for more hybrids/EVs to lower the costs in the long term, and

- As mentioned last month, 2022 realizing the worst sales in new vehicles in over a decade.

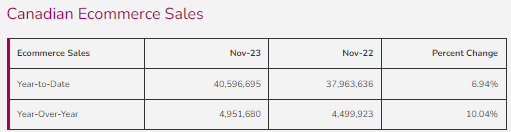

As many Canadians were shopping for holiday in November, JCWG was contemplating how the rapidly changing toy market in Canada would influence retail sales in Canada. Toy stores are represented under the category of Sporting Goods, Hobby, Book, and Music Stores, whose sales were down -0.8% YOY, and -1.0% YTD in November. As Mastermind Toys, Toys R Us, and Melissa & Doug are all under new ownership, these stores are all likely to change (and hopefully for the better). However, it is likely that a large portion of the categories sales are going to Ecommerce (up 10.0% YOY), with some parents are opting for Electronics and Accessories Stores (up 9.2% YOY) for tablets, gaming consoles, and other electronic devices as alternatives to traditional toys. This will be a very interesting category to watch through 2024.

The deadline for partial CEBA forgiveness has arrived. As business groups warn of closures, JCWG is thinking about:

- Are restaurants going to be the hardest hit by this deadline, as more than half are operating at a loss or barely breaking even as they were disproportionately affected by closures?

- Will there be a noticeable decrease in competition for small businesses as closures are imminent?

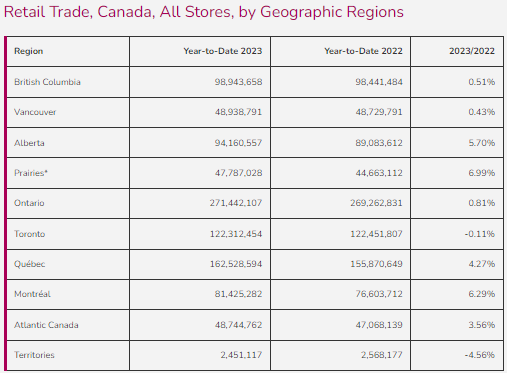

- Where in Canada will the most businesses not have been able to achieve loan forgiveness? While larger cities were closed longer, they were often those who were able to come back the strongest thanks to tourism.

- When will businesses who managed to pay off 1/3 of their loan be able to pay back the rest? Will the next deadline be too soon?

- How have YOU prepared for the repercussions of paying back pandemic supports?

For support with your small/medium business strategy, reach out to the trusted experience at JCWG!

Thank you J.C. Williams Group for this report.