New data on Canadian shopping centre sales per square foot from ICSC provides a clear view of how the retail landscape has evolved since before the COVID-19 pandemic. When compared to Retail Insider’s 2019 study, conducted in partnership with the Retail Council of Canada, the latest figures point to a structural shift rather than a simple recovery.

The data suggests that Canadian retail has not declined in the years since 2019. Instead, it has reorganized, with performance becoming increasingly concentrated among a smaller group of dominant shopping centres.

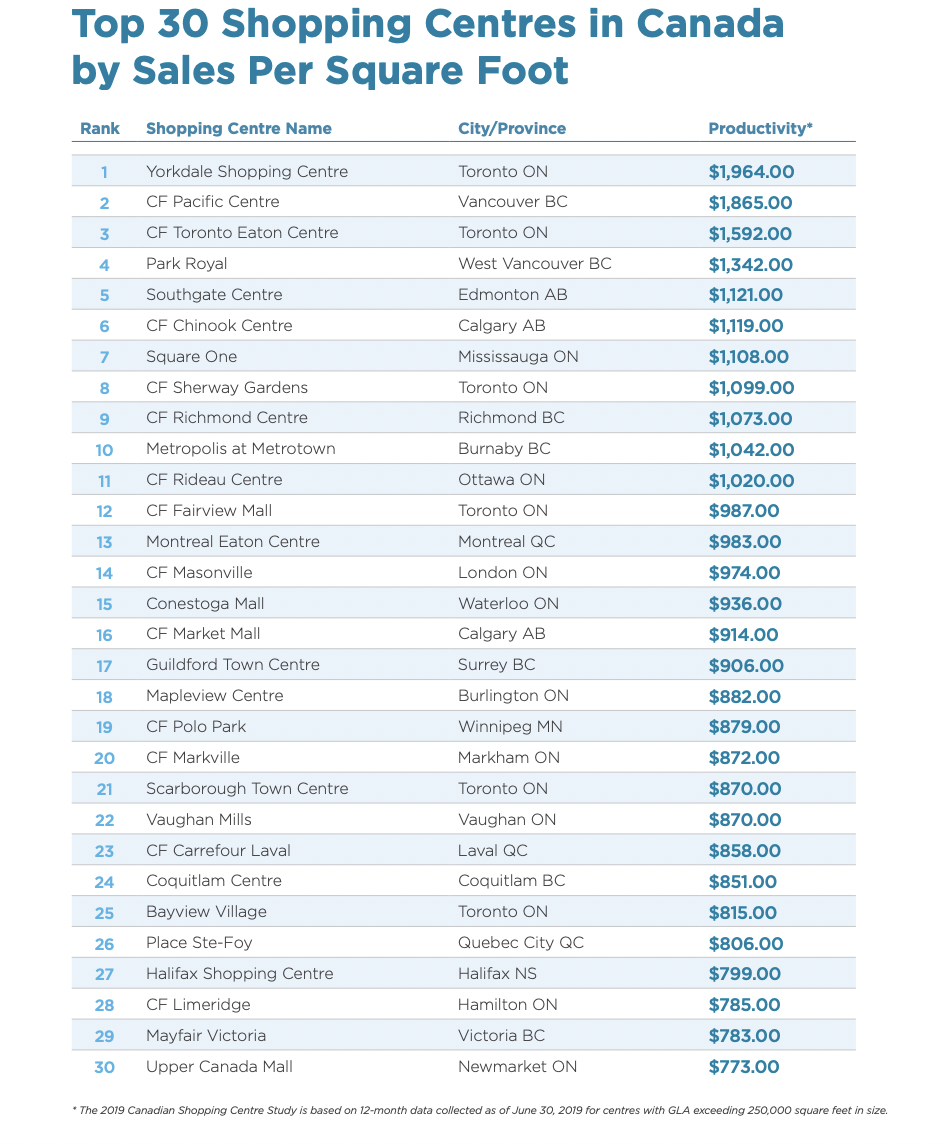

Top-Tier Centres Have Strengthened Their Lead

At the top of the market, leading shopping centres have not only recovered from pandemic disruption but have extended their advantage. Yorkdale Shopping Centre recorded sales of $1,964 per square foot in 2019, rising to $2,368 by 2025.

This increase highlights the growing strength of Canada’s most productive retail assets. Centres such as CF Toronto Eaton Centre have also posted gains over the period, moving from $1,592 per square foot in 2019 to $1,642 in 2025.

While not all top-tier centres have seen uninterrupted growth, their overall position within the market has strengthened. These properties continue to attract premium tenants, international brands, and strong consumer traffic, reinforcing their role as dominant retail destinations.

The Middle of the Market Has Shifted

In 2019, a large number of Canadian shopping centres clustered in the $800 to $1,000 per square foot range. At the time, this was widely considered a solid level of performance for enclosed malls.

By 2025, that same range represents a different position within the market. While many centres still operate within this band, it now sits further from the top tier, which has moved significantly higher.

This shift reflects a broader change in how retail performance is distributed. What was once considered strong performance is now more reflective of mid-tier positioning, particularly in major urban markets.

The $1,000 Benchmark Has Been Redefined

The evolving role of the $1,000 per square foot threshold illustrates the extent of this transformation. In 2019, exceeding $1,000 per square foot placed a shopping centre firmly among the country’s stronger performers.

Today, that threshold has become closer to a baseline for relevance in competitive markets. A growing number of top-tier centres now operate well above $1,300 per square foot, with the highest-performing assets significantly exceeding that level.

This change underscores how retail productivity has become more concentrated in fewer, higher-performing locations.

Urban Dominance Has Intensified

The data also reinforces the continued strength of major urban markets, particularly Toronto and Vancouver. Centres in these regions dominated the rankings in 2019 and continue to do so today, often with even stronger relative performance.

At the same time, certain high-performing centres that were included in the 2019 study are not captured in more recent datasets. Properties such as Park Royal ranked among the country’s top-performing shopping centres in 2019 and are widely understood to remain highly productive.

This suggests that the true upper tier of Canadian retail may be even stronger than current rankings alone indicate.

COVID-19 Accelerated Structural Change

The gap between 2019 and 2023 reflects a period of unprecedented disruption. Retail Insider’s historical study was paused in 2020 as lockdowns forced widespread shopping centre closures. These closures varied significantly by region, making direct comparisons during that period unreliable.

As a result, the post-2023 data provides a clearer view of stabilized performance. When viewed alongside 2019 figures, it becomes evident that the pandemic did not fundamentally weaken Canadian shopping centres. Instead, it accelerated existing trends.

Retailers have become more selective in their physical store strategies, focusing on fewer, higher-performing locations. Consumers, in turn, are increasingly gravitating toward dominant shopping destinations that offer a stronger mix of retail, dining, and experiences.

A More Concentrated and Competitive Future

Taken together, the comparison between 2019 and 2025 highlights a retail landscape that is more concentrated and more competitive than it was before the pandemic.

Top-tier shopping centres have strengthened their positions and continue to attract investment and premium tenants. Meanwhile, mid-tier and lower-performing assets face increasing pressure to adapt through redevelopment, repositioning, or diversification.

The data suggests that Canadian retail has not declined. Instead, it has reorganized around performance, with a growing emphasis on productivity, tenant quality, and overall experience.

As this evolution continues, the gap between leading and mid-tier shopping centres is likely to widen further, reshaping the structure of the country’s retail real estate sector in the years ahead.